Water crises are the top societal global risk in terms of impact, according to The World Economic Forum’s Global Risk Report 2016.

There is of course no lack of water; the risk is around availability of fresh water which constitutes just 2.5% of the world’s water. This has broadly been the case for millennia – what’s new is the enormous growth in demand for fresh water.

Rising water demand is largely influenced by population growth and its food and energy needs. The world population of 7 billion today is projected to grow to over 10 billion by 2050 and the United Nations predicts an associated 55% rise in global water demand.

Companies need to answer three questions to ensure they have resilient business models:

- How dependent is my business on water throughout the value chain?

- Are any of these dependencies in water stressed areas?

- Do I make sufficient profit from my local use of water to compete with other users?

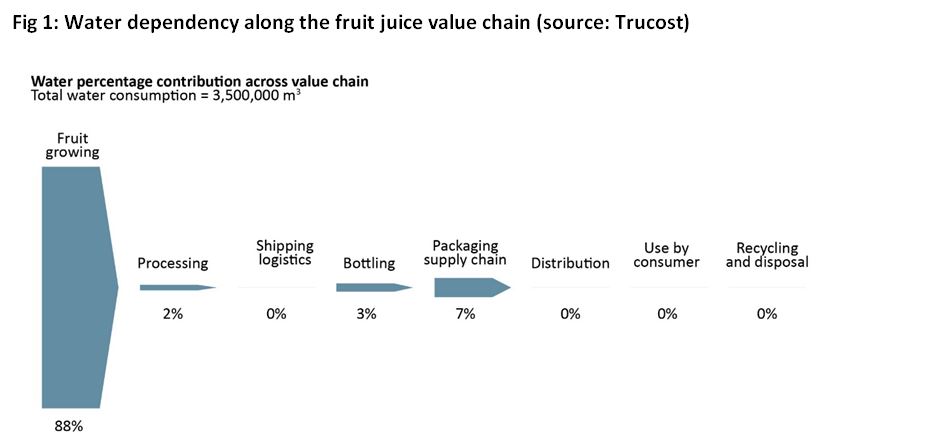

Water Dependency

Companies need to understand their dependency on water throughout the value chain. Many companies – not unnaturally – focus on their own direct use of water. Fig 1 represents the water footprint of a fruit juice company along the value chain. Previously, the majority of their water initiatives were in the bottling process, which accounted for just 3% of water use. Once this was understood, a number of different mitigation strategies were deployed to improve resilience where it most mattered in the fruit growing stage, including long term contracts with farmers in areas of more robust water supply and joint investment in water irrigation efficiency.

Water Stress

Water stress is not simply a consideration for companies operating in the world’s hotter countries. The UK is not often thought of as an area for concern but a 2013 government study classified 9 out of the 24 water company areas as having “serious” water stress.

This stress can translate into business risks in two main ways. Firstly, there is simply insufficient water for the business to operate, or to operate at its optimum capacity. The mining industry is one that frequently has this issue. But it is the second that will increasingly become a standard business concern – that of cost.

Water /Profit

While water has historically been plentiful and inexpensive, this is not the future outlook. Increasing competition for a scarce resource will require companies to make sufficiently good economic use of water to enable them to secure supplies as costs rise.

In Australia’s Murray River basin, where water trading has taken place for a number of years, we have seen water rights sold off by agriculture concerns to other sectors such as mining who use the water more profitably.

To understand and mitigate future risk for both themselves and investors, companies need to understand where in their value chains water presents the biggest risk, alongside competition for water in the river basins in which they operate.

The posts on this blog are opinions, not advice. Please read our Disclaimers.