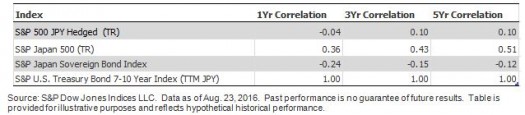

Japanese market participants looking to access U.S. Treasury bonds or any other international bond market may need to be aware of fixed income risk and currency volatility. Depending on their investment view, Japanese market participants may choose to hedge currency risk or remain unhedged. Either way, market participants may be exposed to additional returns or a reduction in returns that can result from the hedging or the performance of the foreign currency.

To illustrate this, let’s look at the S&P U.S. Treasury Bond 7-10 Year Index (TTM JPY) and the S&P U.S. Treasury Bond 7-10 Year Index (TTM JPY Hedged). The S&P U.S. Treasury Bond 7-10 Year Index (TTM JPY) measures the performance of U.S. Treasury bonds maturing in 7 to 10 years and is calculated in Japanese yen, while the S&P U.S. Treasury Bond 7-10 Year Index (TTM JPY Hedged) measures the performance of U.S. Treasury bonds hedged in Japanese yen.

As observed in Exhibit 1, the historical total return of the S&P U.S. Treasury Bond 7-10 Year Index (TTM JPY Hedged) closely tracked the S&P U.S. Treasury Bond 7-10 Year Index, which is calculated in USD. The total return of the hedged index is composed of the local total return and the hedging return, which is derived from the forward return and depends on the interest rate differential between the countries. Since the S&P U.S. Treasury Bond 7-10 Year Index (TTM JPY) has exposure to currency fluctuation, it resulted in higher volatility, and it outperformed or underperformed the hedged index depending on the time horizon.

Exhibit 1: Comparison of S&P U.S. Treasury Bond 7-10 Year Indices’ Returns

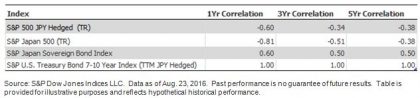

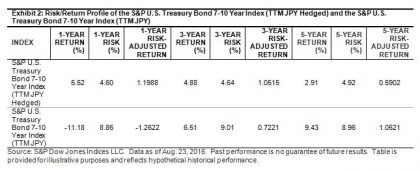

The reduced volatility of the S&P U.S. Treasury Bond 7-10 Year Index (TTM JPY Hedged) is further demonstrated in Exhibit 2; the volatility of the hedged index was approximately half that of the unhedged version over the one-, three-, and five-year periods. In other words, historical data suggests that the S&P U.S. Treasury Bond 7-10 Year Index (TTM JPY Hedged) has a better risk-adjusted return profile.

Conclusion

The S&P U.S. Treasury Bond 7-10 Year Index (TTM JPY Hedged) and the S&P U.S. Treasury Bond 7-10 Year Index (TTM JPY) seek to track intermediate-term U.S. Treasury bonds while giving market participants the option to have currency exposure or manage their currency risk. Japanese market participants seeking the benefits of diversification can access U.S. Treasury bonds. The portfolio volatility could be further reduced by currency hedging, which historically has resulted in a better risk-adjusted return profile.

The posts on this blog are opinions, not advice. Please read our Disclaimers.