In spite of the complex and volatile global markets, the Mexican government issued bonds in the international market for the second time this year. In January 2016, it issued USD 2.25 billion in bonds with a coupon of 4.125%, and on Feb. 16, 2016, it issued two other types of bonds denominated in euros, totaling € 2.5 billion, or approximately USD 2.8 billion. All of this adds up to a total of USD 5 billion, which represents 80% of the foreign debt financial needs for 2016.

The new bonds issued in euros were issued with a yield close to historic minimums in the euro market. The first was for € 1.5 billion, with a maturity in 2022, which was offered at a yield of 1.98% and a coupon of 1.875%. The second was for € 1 billion, maturing in 2031 at a yield of 3.424%, with a coupon of 3.375%. The demand had a ratio of 1.76, with more than 280 international investors. According to the Ministry of Finance (Secretaría de Hacienda y Crédito Público), the level of participation showed the trust in public finances and the good management of public debt. Also, it established new references to provide liquidity to the yield curve in euros.

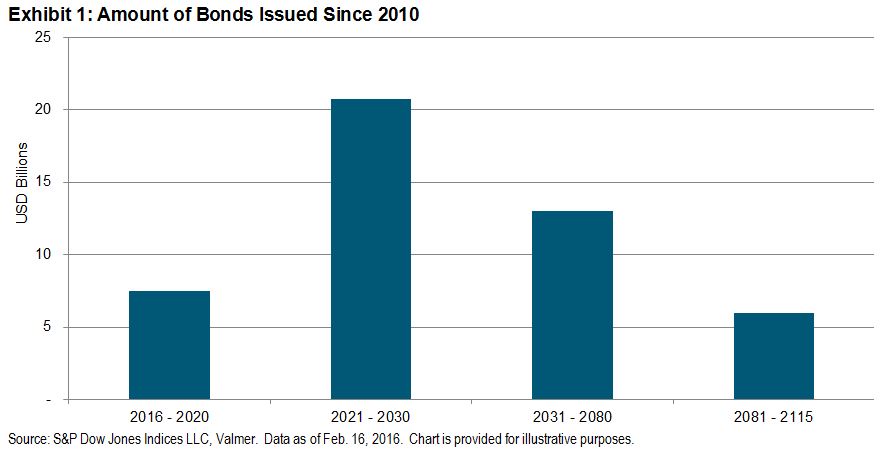

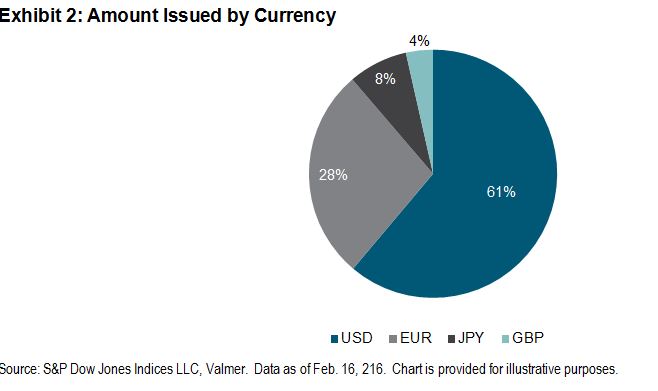

Considering the bond issuances since 2010, Exhibit 1 illustrates the amount issued in U.S. dollars (taking into account bonds in U.S. dollars, euros, British pounds, and Japanese yen), divided by maturity. We can see that 44% of the total (USD 20.75 billion) will mature between 2021 and 2030. Exhibit 2 shows the amount issued by currency and that 61% of the total amount is issued in U.S. dollars.

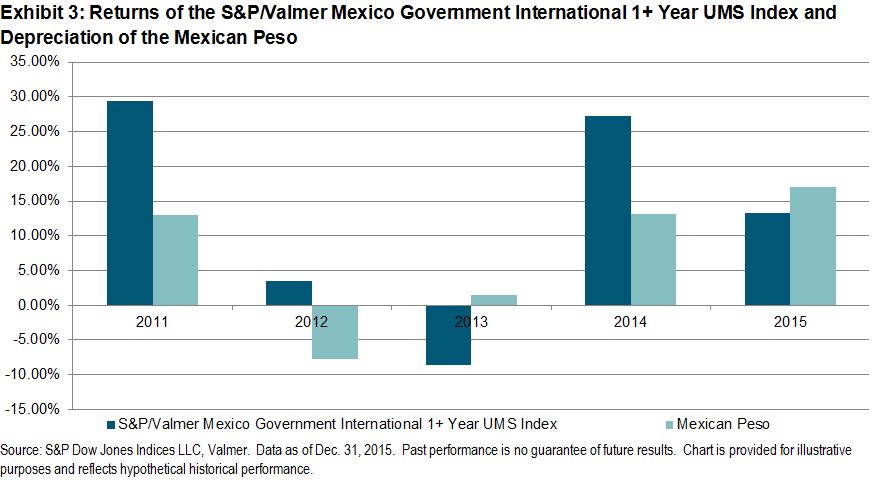

S&P Dow Jones Indices seeks to track the bond issuances in U.S. dollars with a maturity of over one year with the S&P/Valmer Mexico Government International 1+ Year UMS Index. Exhibit 3 shows the annual returns of the index for the past five years and the depreciation of the Mexican peso against the U.S. dollar. We can see that annual high returns are correlated with a depreciation of the currency.