Lyrics to the Canadian national anthem, “O Canada,” state “The true north strong and free!” Like in the U.S and many other countries, government and corporate debt has become a big issue in Canada.

The Canadian overnight rate stands at 0.5% and will most likely remain unchanged or decrease even more. Central Bank Governor Stephen Poloz’s decision on Jan. 20, 2016, to keep the benchmark rate at 0.5% halted a slide in the currency.

With rates so low, governments have been looking to more than just monetary policy to stimulate their economies. The newly elected Canadian government has looked to infrastructure spending as a way to grease the economic skids. Prime Minister Justin Trudeau said the federal government would fast-track infrastructure spending.

The newly elected liberal government said the deficit could swell to CAD 30 billion in the 2016-2017 fiscal year amid a starkly weaker outlook for the economy. Such a large deficit would be 1.5% of GDP. Compared to the amount of debt the U.S. carries, with obligations to other countries such as China, Canada’s AAA rating and debt amount look pretty good, but investors should be aware that the situation is and will be changing. Larger amounts of longer-term debt may make the Canadian indices more sensitive to interest rate movements.

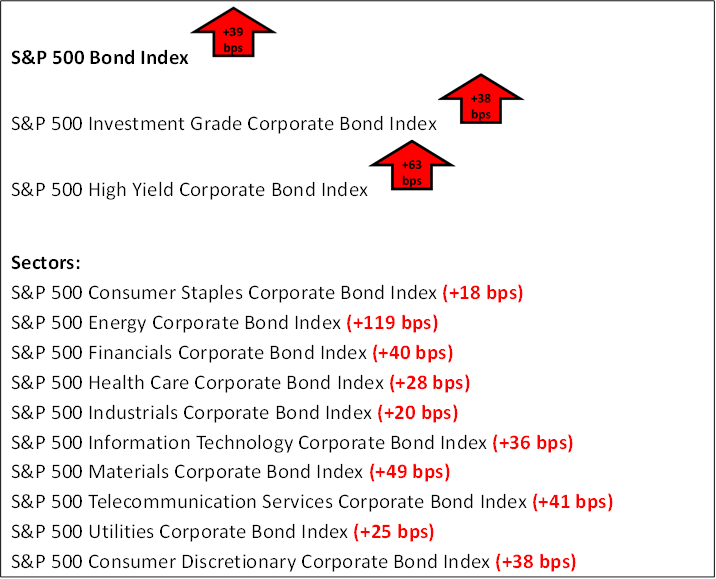

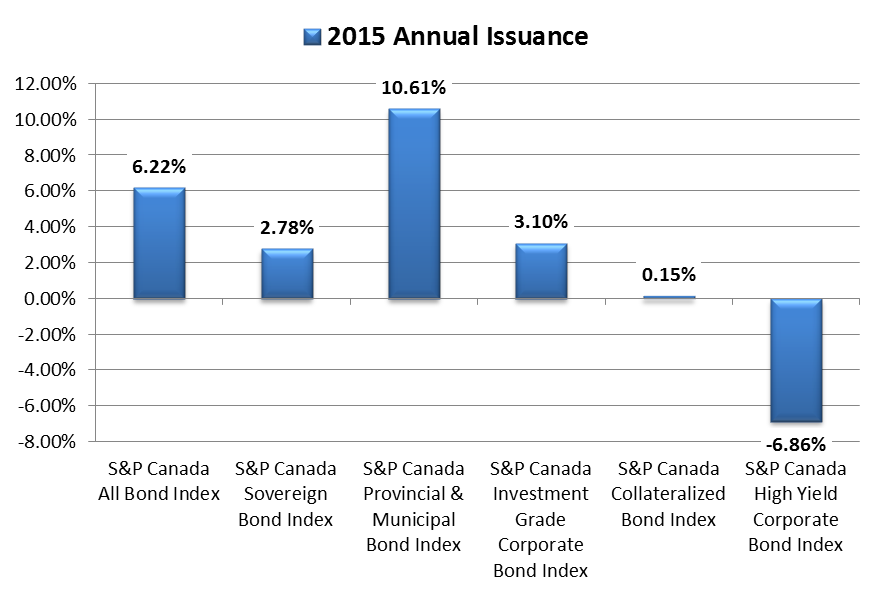

Exhibit 1 shows the percentage changes in the Canadian dollar amount of debt for each fixed income asset class for 2015. The amount of debt outstanding for 2016 is expected to grow as the new government’s policies are put into place.

Exhibit 1: Index Increases of Market Value

Source: S&P Dow Jones Indices LLC. Data as of Dec. 31, 2015. Past performance is no guarantee of future results. Chart is provided for illustrative purposes. *Globe and Mail, BoC holds rates; bets stimulus, global gains will ease economic pain, Barrie McKenna, January 20, 2016.

The posts on this blog are opinions, not advice. Please read our Disclaimers.