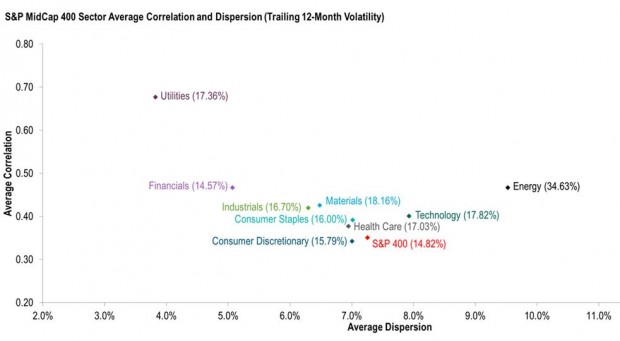

Stock market turmoil is generating fears and predictions of a 2016 recession. The S&P 500 and the Dow dropped more than 10% from recent record highs to correction levels, but none of this guarantees a recession. In fact, the stock market is notorious for predicting recessions –and many other things – that never happened. The chart shows the S&P 500 since 1948 with vertical areas marking recessions. The market does drop before each recession, but it also drops several times where there is no recession. In fact the biggest drop of all – October 19, 1987 – didn’t point to a recession.

A better place to look for recession warnings is in the broader economy – and the news there is better than in the market. A reliable short term indicator is the weekly unemployment insurance claims report – the number of people recently laid off filing their first claim. Anything under 300 thousand is considered good news, anything over 400,000 spells recession. The numbers have been under the 300 thousand mark for a some time.

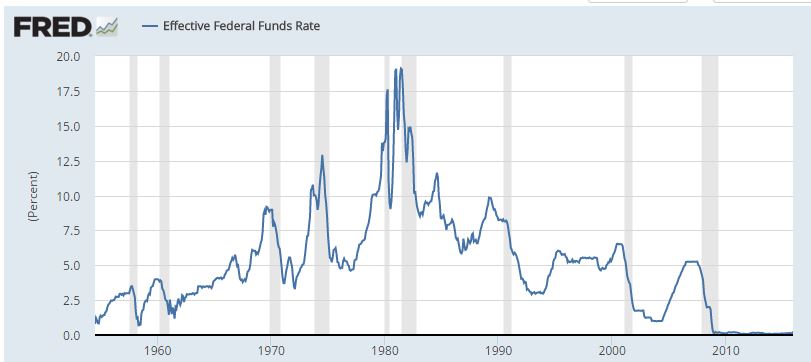

Some analysts are arguing that the Fed erred in raising the Fed funds rate last month and has set the stage for a recession. For politicians, if the market didn’t signal recession than the Fed is causing one. However, the chart shows the Fed funds rate since the mid-1950s and recessions. Interest rates do rise before recessions, but there are a lot of false signals and long lead times.

There will be another recession, and no one knows when it will begin or how nasty it will be. Despite 2016’s poor start on Wall Street, most of the economic indicators are positive. If everyone expects a recession, stops spending, starts hoarding their money we will get a recession.

Data for the S&P 500 chart from S&P Dow Jones Indices, Recession dates from the National Bureau of Economic Research. Charts marked FRED are from the Federal Reserve Bank fo St. Louis economic data.

The posts on this blog are opinions, not advice. Please read our Disclaimers.