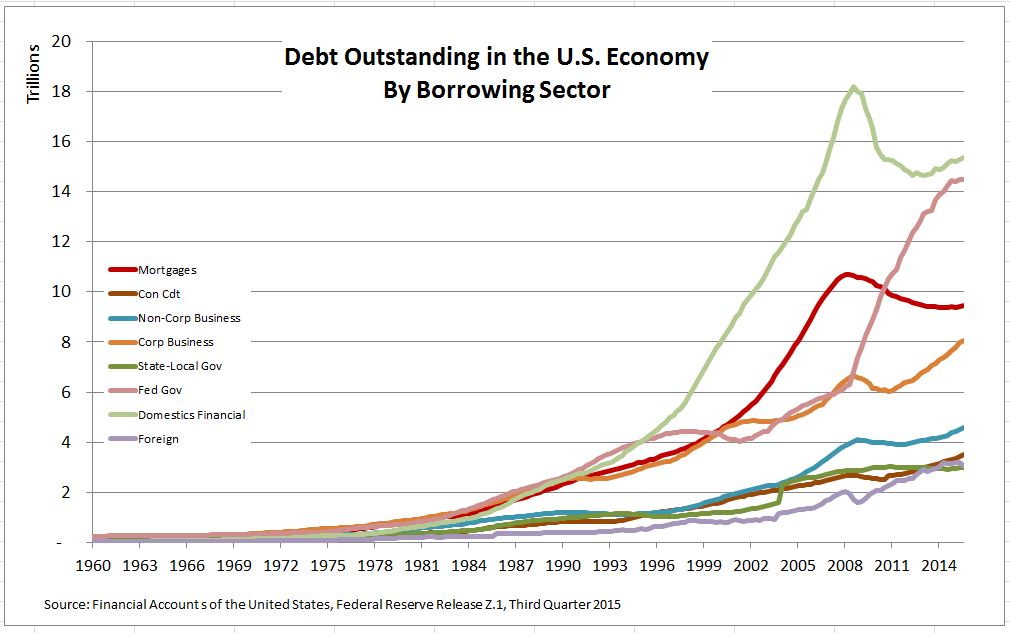

As the Fed prepares to raise interest rates on Wednesday – or surprise virtually everyone – it is worth looking at the debt in the economy. Interest expenses for most of it won’t move very much or very soon, but some believe the Fed is embarking on a two to three year process of pushing interest rates every upward.

The chart tells the story. The pale green line with the peak at about 2008 is the domestic financial sector – banks, brokerages, insurance companies and so forth. Like most sectors, this one peaked as the financial crisis hit; unlike some sectors it has paid down a lot of debt and then resumed its climb. Since the mid 1990s the growth of financial sector debt outpaced everything else, it may be poised to outpace most other sectors going forward. The red line – home mortgages — has the second largest dip after financials and it too is recovering. Neither of these suggests a major change or retrenchment following the financial crisis. Another sector that gets a lot of attention is the pink line trying to flatten out in the latest couple of quarters – federal government borrowings. Corporate business, the gold colored line, staged a sharp rise in the last few years.

The bottom four sectors are a bit more stable and represent foreign borrowing in the U.S., state and local government debts, consumer credit and non-corporate borrowing.

The message here is two parts: one reason the last recession was called the Great Recession is the large and rapidly growing debt throughout the economy in 2007-2008; second is the hope that a small rise in interest rates and borrowing costs will moderate the current growth rates well before the next recession.

The posts on this blog are opinions, not advice. Please read our Disclaimers.