Since 1938, the state has been doing all the work. PEMEX was the only company managing the exploration, exploitation, and commercialization of oil but with the energy reform, things will change. PEMEX is the biggest company in Mexico, with sales over USD 123 billion and total assets over USD 156 billion as of 2013. Mexico recently opened the market for more participants through the tenders that started with “Ronda Uno” (Round One) in July 2015. In this first phase, only two blocks out of 14 were awarded, which was not what the Ministry of Energy was expecting (between 30%-50%). The next phase of Ronda Uno will be on Sept. 30, 2015, with five different contracts to be awarded in nine different blocks for drilling.

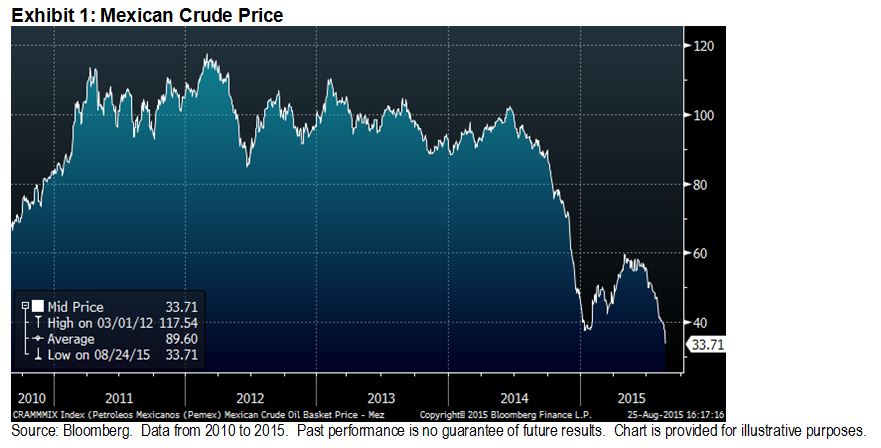

The global economy, especially China, has not helped with this. Year-over-year, Mexican crude fell 63.05%, from USD 91.22 to USD 33.71 (as of Aug. 24, 2015). Exhibit 1 shows the price of Mexican crude over the past five years.

But, What About the Debt of PEMEX?

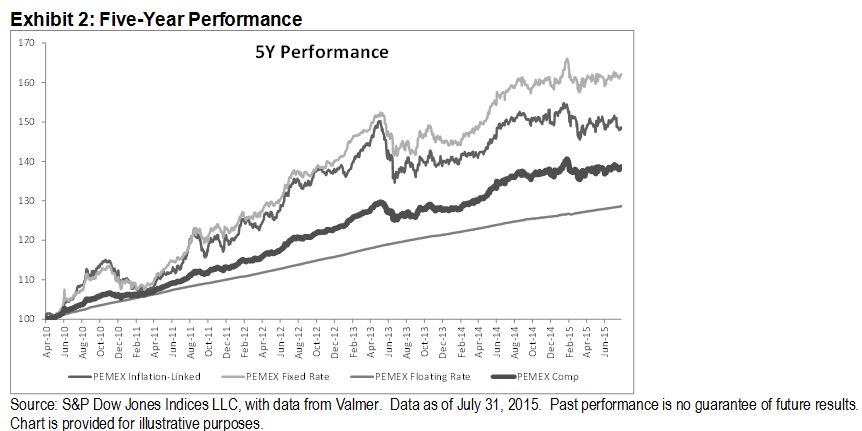

Nowadays, PEMEX issues debt in pesos, dollars, and euros. By the end of 2013, the debt in U.S. dollars represented 79% of the company’s total debt. Focusing on the local debt and using local information, we created four indices classified by: fixed-rate debt, inflation-linked debt, floating-rate debt, and a separate index comprising the other three. For the inflation-linked index, the cumulative returns were -2.50% YTD, and -1.04% for the one-year period. During the same time period, the fixed-rate debt returned only 1.52% YTD and 2.05% year-over-year, as shown in Exhibits 2 and 3.

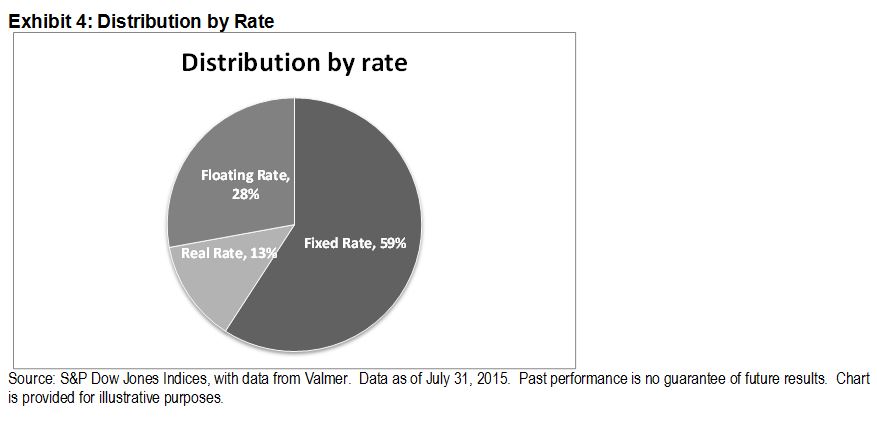

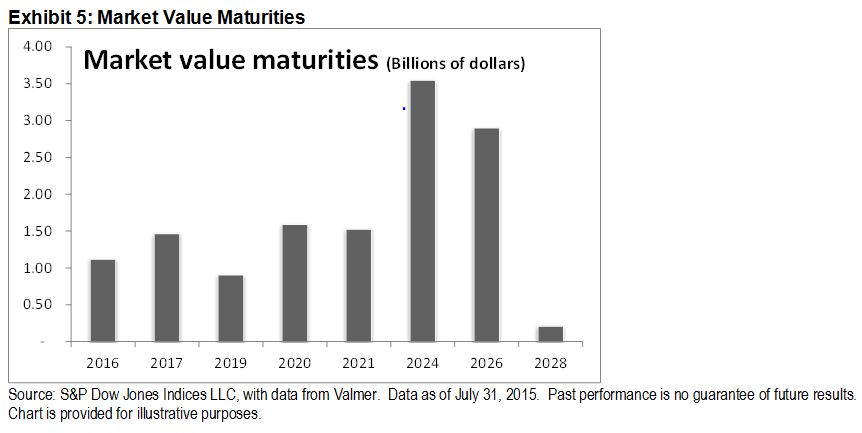

The total local debt was distributed into 14 issues (not including the PEMEX 09U series or ABS), with a total market value of USD 13.25 billion (as of July 31, 2015, using a spot price of MXN 16.1088), where 59% of the total is represented by fixed-rate bonds and 26.74% matures in 2024. Exhibit 4 shows the distribution of the different rates and Exhibit 5 the maturity in billions of U.S. dollars in market value.

Finally, if we think about a peer for PEMEX —not from an oil perspective but from the perspective of a quasi-sovereign company in Mexico—the Federal Electrical Commission (CFE) is the first name that comes to mind. With six different types of bonds (excluding ABS) and USD 4.06 billion of market value, PEMEX represents 56% of the S&P/Valmer Quasi-Sovereign Bond Index, while CFE represents 28%. Comparing the fixed-rate bonds of these two, Exhibit 6 shows how PEMEX has underperformed CFE. Moreover, we can compare them with some of the indices of the S&P/Valmer Indices, and we can see also how PEMEX has underperformed year-to-date and over the one- and three-year periods.