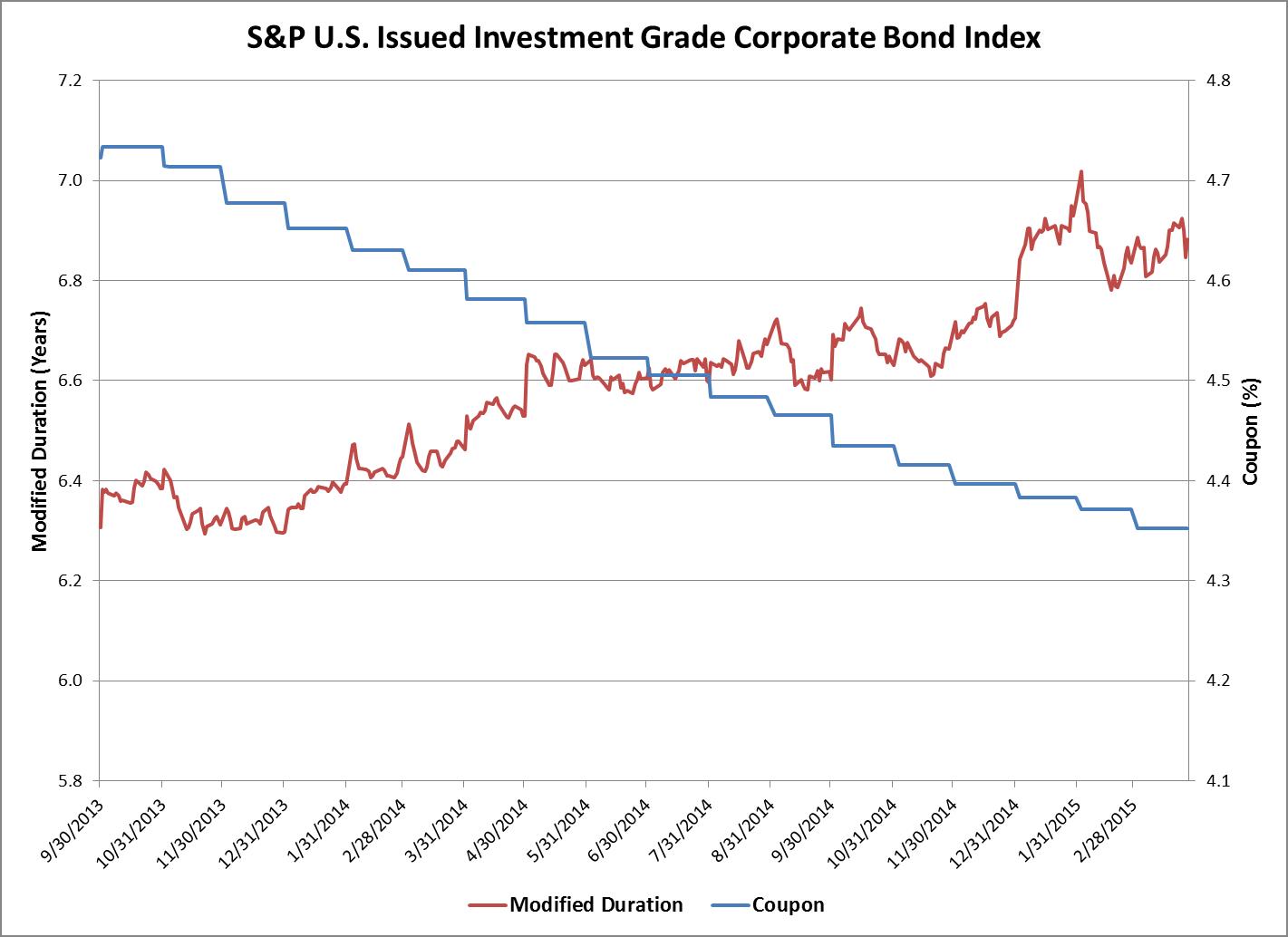

Lower yields and newly issued coupons have added an element of danger to fixed income investing.

The following chart shows that since September 2013, the weighted average coupon of the S&P U.S. Issued Investment Grade Corporate Bond Index has trended down, as higher-coupon bonds are called away and lower coupon new issuance is added to the index at the monthly rebalancing. The result of a lower coupon for the index is that the modified duration has been moving up, or longer out on the curve. The modified duration of the index is currently at 6.9 years, and the coupon is 4.35%. The index has returned 0.41% MTD and 2.11% YTD as of March 31, 2015.

As issuance in the primary markets hits record levels, lower coupons, yields, and longer bonds could change the characteristics of an index.

- The lower the bond’s coupon or yield, the higher the duration and volatility of price. Bonds with low coupon rates and lower yields will have a higher duration than bonds that pay high coupon rates or offer higher yields. Because the bond pays a low coupon rate, the holder of the bond receives repayment of the bond at a slower rate.

- Longer-maturity bonds also have higher durations and are exposed to more risk.

Source: S&P Dow Jones Indices LLC. Data as of March 31, 2015. Charts and tables are provided for illustrative purposes only. Past performance is no guarantee of future results.