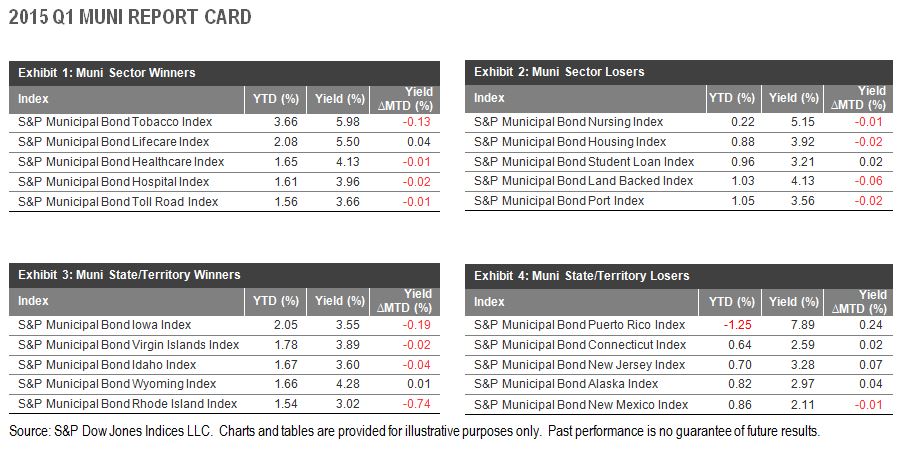

The S&P Municipal Bond Puerto Rico Index was the only state or territory index to finish the quarter in the red, down 1.25% with its yield to worst at 7.89%. Yields continue to rise as investors become more skeptical about Puerto Rico’s ability to fulfill obligations to their creditors.

The S&P Municipal Bond Puerto Rico General Obligation Index saw yields climb to 8.36% to finish the quarter. Yields on the index have not been this high since January 2014. The S&P Municipal Bond Puerto Rico General Obligation Index includes bonds from the Puerto Rico Electric Power Authority (PREPRA) that have received a 15-day extension on their debt. Investors have been concerned, as it appears the leveraged utility may have to borrow upward of USD 600 million in additional funds just to keep the lights on, with a looming USD 400 million debt payment scheduled for July 2015.

The S&P Municipal Bond Tobacco Index has outperformed all other muni sectors thus far in 2015, returning 3.66% YTD. In contrast, the S&P Municipal Bond Nursing Index was the sector loser, finishing the quarter up just 0.22% YTD. The yields are comparable; however, it is important to remember that the Tobacco Master Settlement Agreement of 1998 is a 25-year settlement. All things equal, longer duration reduces yield. Tobacco munis have a modified duration of 10.1, compared with the nursing sector’s modified duration of 3.2. Comparable yields and contrasting durations indicate that, while tobacco may be the flavor of the month, the market (and hopefully the end user) associates much more risk with tobacco than with nurses.

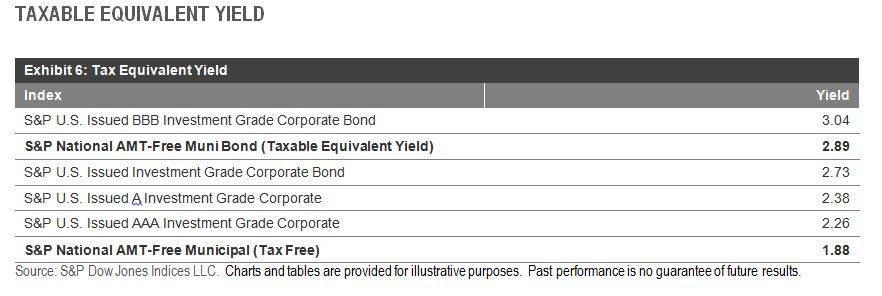

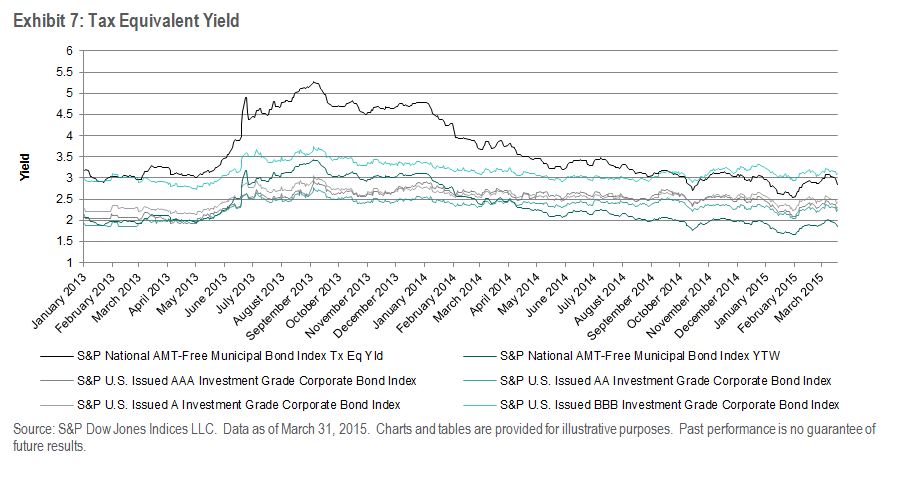

CORPORATE COMPARISON

When examining yields and returns on tax-free munis, it is imperative to consider the potential tax benefit. The investment-grade issues in the S&P National AMT-Free Municipal Bond Index have a tax equivalent yield of 2.89%, which is superior to the yield of 2.73% posted by the S&P U.S. Issued Investment Grade Corporate Bond Index.