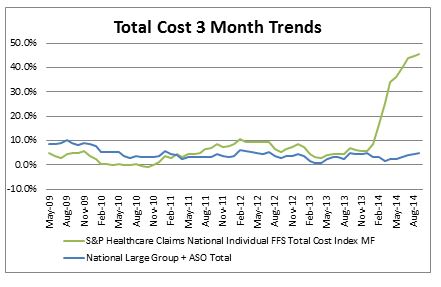

The overall medical trend rates covering all services have continued to be modest in the S&P data through the 3rd quarter of 2014—increasing up to 3.5% on a 12-month moving average basis as of September[1].

But in 2014 the Individual trends reported by S&P are now over 45% based on 3-month moving average trends as of September. These can reflect the impact of adverse selection, higher demographics and higher minimum (essential) benefits required under the ACA. To one degree or another, the industry tried to anticipate these effects in the initial rating for 2014. It remains to be seen if we see a similar effect on Small Group in 2015. We would not expect the impact to be as dramatic on Small Group as it was for Individual in 2014, however the results remain uncertain at this time. The Small Group ACA coverage requirement and electronic enrollment had been deferred until 2015 and insureds in this category were only allowed to enroll electronically staring in late 2014 so no experience due to Small Group ACA enrollment is yet apparent, but there could be an increase in these measured trends, although probably not as dramatic as the Individual trends.