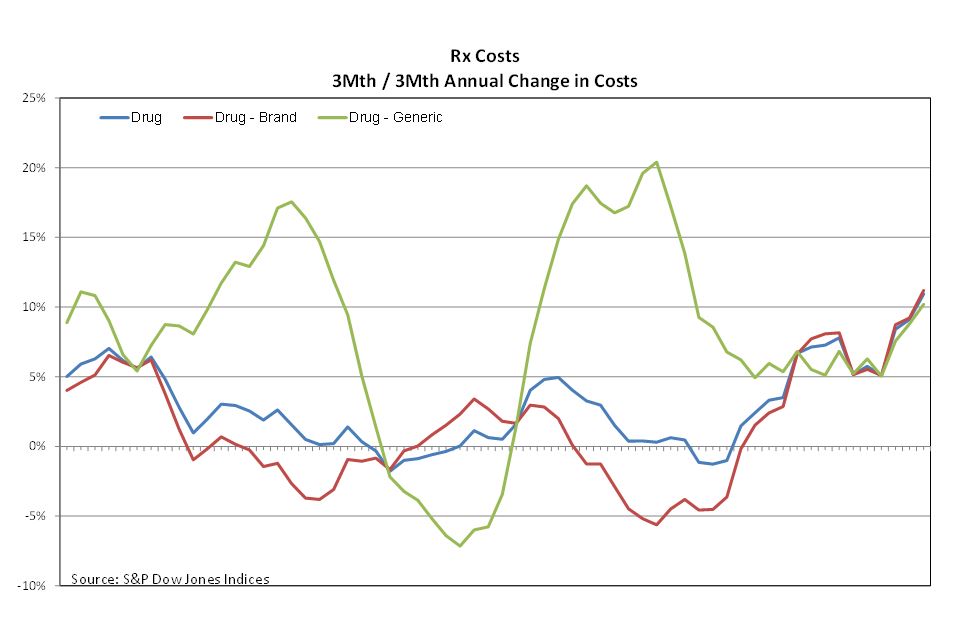

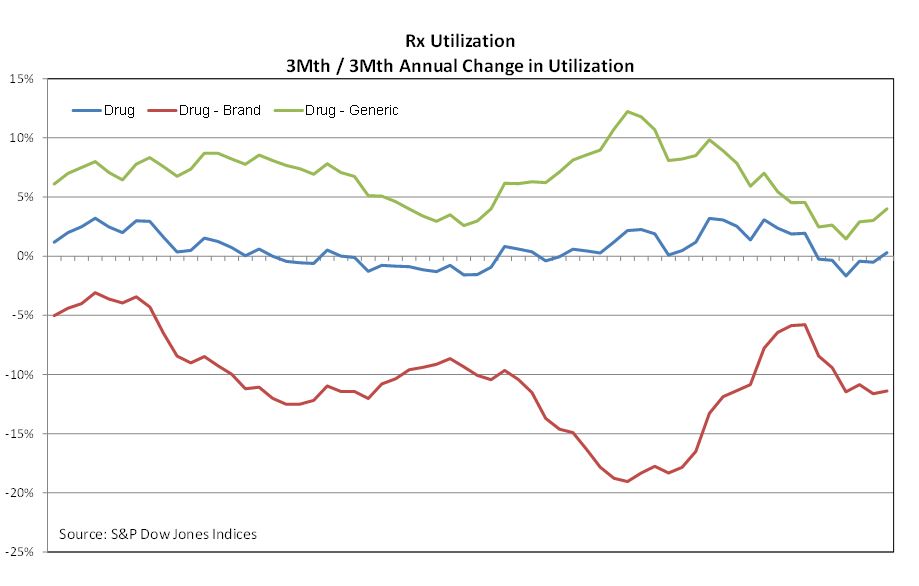

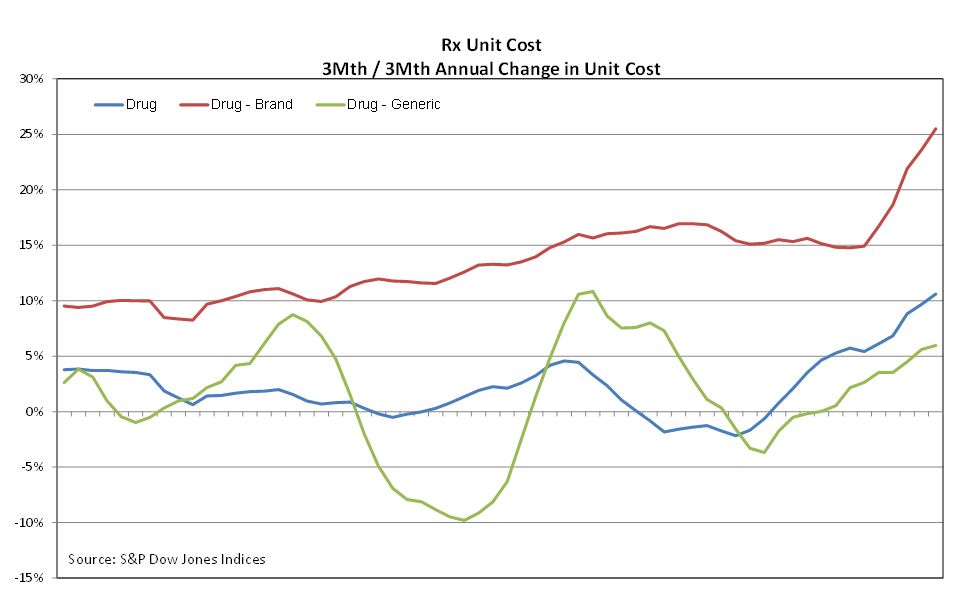

In late August, as reported by the Wall Street Journal, Walgreens announced the departure of their CFO at the end of the current year. This news came after a significant cut in forecasts by $1.1 billion from the original $8.5 billion forecast in fiscal 2016 pharmacy-unit earnings. According to the Wall Street Journal, “Walgreens hadn’t factored in, among other things, a spike in the price of some generic drugs that it sells as part of annual contracts.” This illustrates an opportunity where the S&P Healthcare Claims Indices may have been utilized as a tool to monitor the changing costs of both medical and drugs. As evident in the cost chart below, generic drug costs tend to be quite volatile, with overall costs growing at times in excess of 20%. However, looking at utilization, we can see that growth peaked in January of 2013, and has been declining ever since.

To gain insight on generic drugs, one may look at Unit Cost Indices, which show that while brand name drugs continue to escalate in price steadily over time, the cost of generic drugs on a Unit Cost basis tends to be more volatile, even declining in price at times. Because both the utilization and average cost of generic drugs are driven by factors such as the end of the patent protection period on brand drugs, high volatility is likely to be an inherent characteristic of generic drugs. By utilizing the S&P Healthcare Claims Indices, one may be able to better manage expectations for future changes in healthcare costs by studying recent trends.

The posts on this blog are opinions, not advice. Please read our Disclaimers.