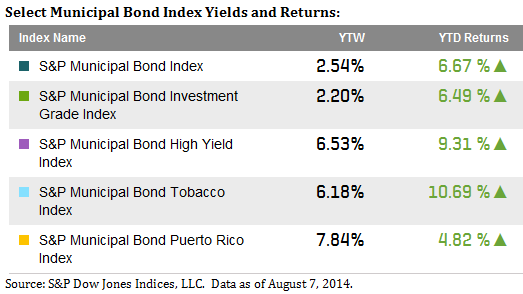

As the young gas station attendant says at the end of the movie Terminator “there is a storm coming”. While Detroit and Puerto Rico’s financial struggles continue to rattle the municipal bond market, the over $87billion state issued tobacco settlement bond market is another potential dark cloud worthy of watching.

A recent article in the Huffington Post ‘How Wall Street Tobacco Deals Left States With Billions of Toxic Debt‘ initiates an important discussion on the future of the future of this large sector of bonds.The S&P Municipal Bond Tobacco Index has returned over10.6% year to date as it leads all other municipal bond sectors in performance. These impressive short term gains mask the risk associated with these bonds. Two of the largest risks are that the average credit quality of bonds in this sector is well below investment grade and the heavy issuance of zero coupon bonds creates a sector that has one of the longest durations in the municipal bond market.

Why worry now? The hazardous combination of credit and interest rate risk. Repayment of these bonds is heavily dependent upon sales of tobacco products in the U.S. at a time when U.S. tobacco consumption is declining. The long duration of bonds in this sector make it highly vulnerable to when interest rates begin to rise – the prices of these bonds will fall more quickly and by a larger amount when interest rates begin to rise.

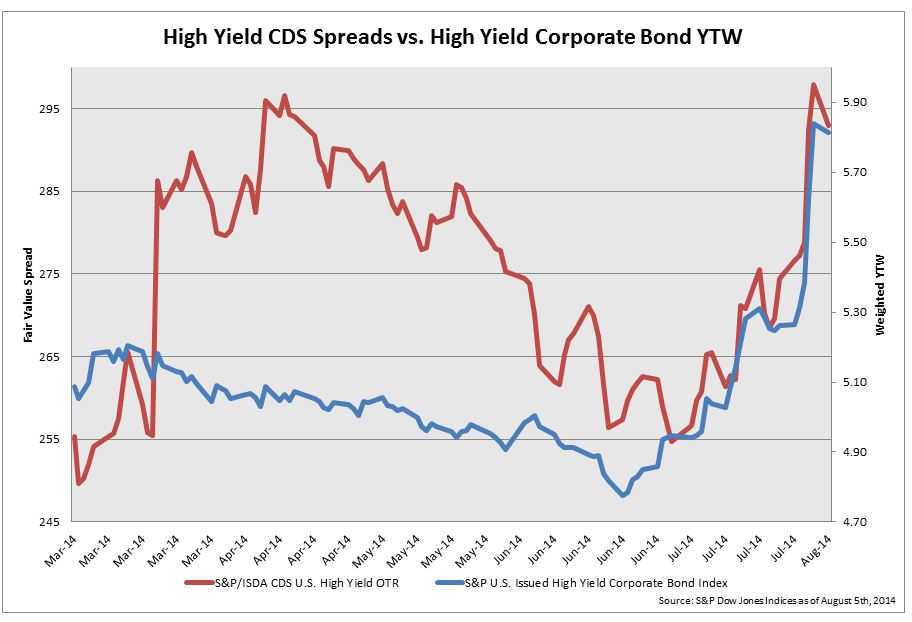

The divergence between CDS spreads and actual high yield bond yields show that the bond market has not followed CDS spreads movements due to the appetite for yield supporting the high yield market and pushing bond yields down. Argentina’s default caused bond yields to move more in line with the direction of CDS.

The divergence between CDS spreads and actual high yield bond yields show that the bond market has not followed CDS spreads movements due to the appetite for yield supporting the high yield market and pushing bond yields down. Argentina’s default caused bond yields to move more in line with the direction of CDS.