On my daily commute to New York City via New Jersey Transit today I overheard a conversation on the train that started with “Back when I was a kid”. Though the start of the conversation had grabbed my attention, the rest became a blur as the statement had triggered memories that related to the current article I was reading on my IPad. The combination of a fellow commuter’s overheard statement and E.S. Browning’s article Inflation Is Back on Wall Street Agenda got me thinking about being a kid in the 1970’s.

Back then news was not a major focus of mine as I had more important things like Little League Baseball and CYO basketball to occupy my time. Though there are memories of newscasts on our black and white television or overheard radio reports from the back seat of my dad’s Ford Fairlane. Even as a kid I knew the economy was a mess. Oil prices never went down, gold was a hot commodity and Inflation sounded more like a monster than an economic concept. Now I’m not saying we are due for a 1970’s economy, just that the idea of inflation has had a long lasting impact on me and others of the time.

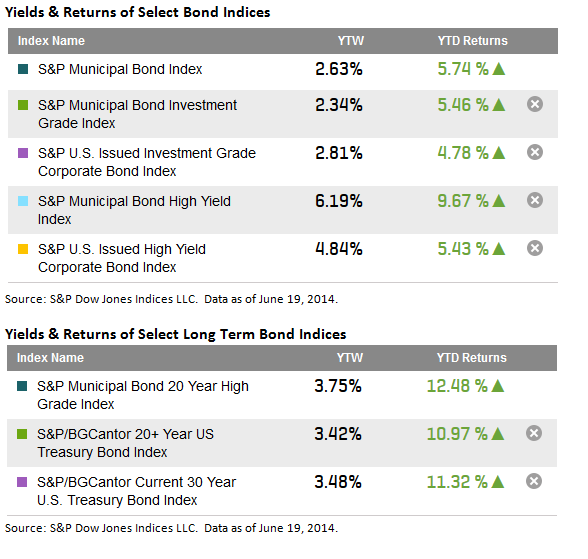

In addition to my memories of the past, Mr. Browning’s article made for an interesting read to fill the time of my commute. Lightly touched upon in the article was the financial product of TIPS (Treasury Inflation Protection Securities). These securities did not exist “back then” but were issued by the U.S. Treasury in 1997, specifically to protect against the eroding effects of inflation upon the principal of fixed income securities. The S&P U.S. TIPS Index has returned 4.88% year-to-date, though longer indices such as the S&P 10+ Year US Treasury TIPS Index are returning 10.10% year-to-date.

Another addition to the U.S. Treasury’s portfolio of products, which would be beneficial to investors in a rising rate environment, is the recently issued floating rate product. On July 31, 2013, the U.S. Treasury published amendments to its marketable securities auction rules to accommodate the auction and issuance of a Floating Rate Note (FRN). Treasury FRNs are indexed to the most recent 13-week Treasury bill auction. $15 billion of 2-year FRN was first issued on January 23rd, 2014. The S&P U.S. Floating Rate Treasury Index is returning 0.04% month-to-date and is made up of the originally issued January 2016 maturity along with a more recent April 2016 issue.

Source: S&P Dow Jones Indices, Data as of 6/20/2014

The posts on this blog are opinions, not advice. Please read our Disclaimers.