The S&P Municipal Bond Tobacco Index has returned 12.79% year to date as the tobacco settlement bond market has recovered from a dismal 2013 return of -8.77%. Yields of these bonds have fallen 99bps during the year to an average of 5.92%. These long duration higher yielding bonds represent just under 15% of the total market value of the S&P Municipal Bond High Yield Index which has returned 9.86% year to date.

Yield investors seem to be willing to accept significant incremental risk over the near term as the prospects for repayment of tobacco settlement bonds is dependent upon tobacco sales in the U.S. which has been declining over time and may be a critical factor that may drive defaults of these bonds in the future.

The ten year range of the municipal bond market remains relatively cheap given the S&P AMT-Free Municipal Series 2023 Index has an average tax free yield of 2.53% which is just 5bps below the 10 year U.S. Treasury Bond.

Longer, high quality municipal bonds tracked in the S&P Municipal Bond 20 Year High Grade Index have returned over 12.2% year to date as yields have dropped by 79bps during the year so far.

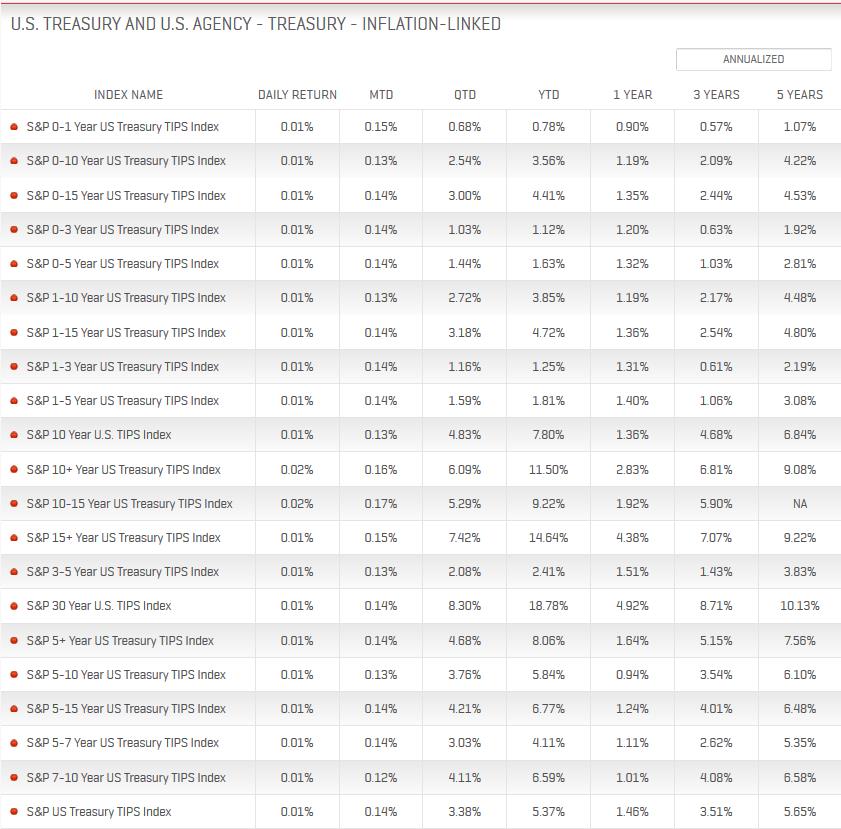

Returns of Select Municipal Bond Indices as of June 12, 2014:

Source: S&P Dow Jones Indices. Data as of June 12, 2014.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

Source: S&P Dow Jones Indices, June 11, 2014

Source: S&P Dow Jones Indices, June 11, 2014