Bonds May Puzzle But Stocks Could be Worrisome

Bonds: Just when people thought we were safe from creative financing applied to bonds backed by homes, a new improved approach is about to surface. The past year has seen an increase in buying homes for rent by private equity funds and others. The private equity buyers are funded by their fund investors, much the same way private equity investments in corporate businesses are funded. As noted in the New York Times yesterday, American Homes 4 Rent, a publicly traded real estate investment trust is planning a bond issue to raise funds to purchase homes for rent. The company went public last summer and has a market value of about $3 billion. If this bond issue proves successful, and is followed by further issues from other companies looking to enter the home purchase-to-rent business, this could accelerate a shift towards renting from buying.

The growth in buy-to-rent may raise some risks to the economy. If a large buy-to-rent firm fell on hard times or if housing prices in an area with significant rental activity were to drop, the owner of rental homes might be tempted to dump the houses on the market putting huge downward pressure on prices, and the local economy. Such a move might mean falling prices and the specter of default for rent-to-buy bonds. At present the extent of rent-to-buy is modest and the risk of a major economic reversal from a collapse in the rental housing market is limited. Separately the Census Bureau reported today that the home ownership rate for the fourth quarter of 2013 was 65.2%, a bit below the figure of 65.4% at the end of 2012.

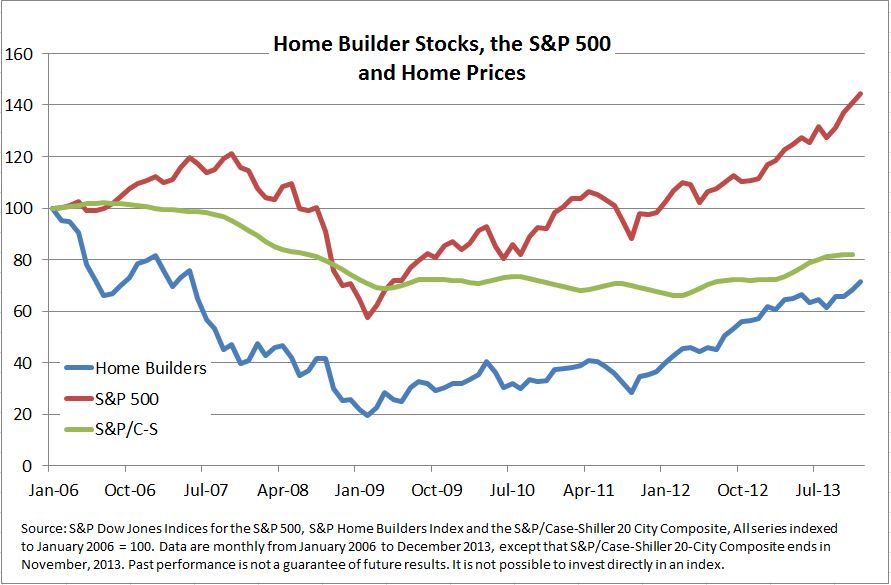

Stocks: While housing starts and new home sales lagged in this long drawn out recovery, home building stocks did well. Home builders, as shown by the S&P Home Builders Index, dropped farther and faster than either home prices or the S&P 500. (see chart). The exciting part started at the bottom in February 2009 – well before home prices turned up in the second quarter of 2012. From the bottom, the home builders are up about 2.6 times, much better than the 1.5 times gain in the S&P 500. Home prices are above their level of February 2009, but not by much.

The recent activity is not as nice. From December 31st 2013 to the end of January 2014, home builders are down 5.1% compared to a drop of 3.5% for the S&P 500.

The posts on this blog are opinions, not advice. Please read our Disclaimers.