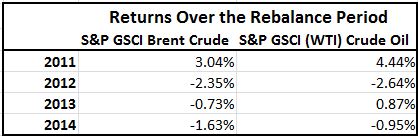

Maybe the verdict is still undecided for some, but it is hard to look at the evidence and still be questioning the idea that index investing drives underlying commodity prices. Now that the commodity index rebalance is over and the shift between WTI and Brent is behind, we can examine the impact. As I mentioned in a prior blog post, Not ALL Weights are EQUAL: Why Brent isn’t Heavier than WTI, there has been a dramatic move out of WTI and into Brent since 2011. Below is the table:

If one follows the logic that prices increase based on index investing, then one would have witnessed falling WTI prices and rising Brent prices. However, that is not what happened.

Notice 3 out of 4 years when the index weights were increasing in Brent, the return over the rebalance period was negative. Also notice that in 2 of 4 years when the index weights were decreasing in WTI, the return over the rebalance period was positive.

Supply and demand should be unaffected by commodity futures investing since there is no physical delivery from commodity futures investing. Along with the simple example over the rebalance, there are fundamental stories that demonstrate a disconnect between money flow and price. For example, Brent recently fell pressured by incremental increases in Libyan oil supply and expectations that Iranian crude will return to market.

Another simple argument is as follows: trading, production and open interest stats are similar for crude oil and natural gas where futures trading volume is several times larger than production or consumption. Sometimes oil prices are up while natural gas is down, so how can futures trading be driving price of oil up while gas, with same trading stats, is down? (Nat gas may be down from fracking technology increasing supply. A supporting comment is at http://www.econbrowser.com/archives/2012/04/a_ban_on_oil_sp.html with a follow up at http://www.econbrowser.com/)

There is a helpful summary of research studies on the topic of futures trading versus spot prices, which states that currently, there is no clear evidence of futures trading driving spot prices. An article on Vox by Lutz Kilian was based on his paper, “The Role of Speculation in Oil Markets: What Have We Learned So Far?” He co-authored the paper with Bassam Fattouh and Lavan Mahadeva. The article neatly summarized the results of a number of studies on the topic and concluded that the literature has shown that the presence of index funds has, if anything, been associated with reduced price volatility. (This is since long-only investors provide insurance to producers, hence reducing price volatility from the supply side) They found that the existing evidence is not supportive of an important role of speculation in driving the spot price of oil after 2003. Instead, there is strong evidence that the co-movement between spot and futures prices reflects common economic fundamentals, rather than the financialization of the oil futures markets.

Another research piece on the link between commodity futures investing and spot price can be found at http://docs.edhec-risk.com/ERI-Days-Asia-2012/documents/Long-Short_Commodity_Investing.pdf. The 2009 Staff Report by the U.S. Senate Permanent Subcommittee on Investigation argues that commodity index traders were disruptive forces, driving prices away from fundamentals. If established, this would support calls for an increase in transparency, position limits and margins to curb excessive speculation, and it is hoped – volatility. Since then, the claim that the financialization of commodity markets is responsible for the observed volatility in commodity prices has been the subject of an intense academic debate – the overwhelming conclusion of which has been that it is not possible to empirically link investments in commodity futures and commodity futures prices. (See for Irwin and Sanders (2011) for a recent review of the evidence at Irwin, S., and D., Sanders, 2011, Index funds, financialization, and commodity futures markets, Applied Economic Perspectives and Policy, 1-31.)

The Edhec paper also studies whether the observed financialization of commodity futures markets (as evidenced by the increase in the long, as well as short, positions of speculators over time) has led to change in the conditional volatility of commodity markets or to changes in their conditional correlations with traditional assets. Their results find no support for the hypothesis that speculators have destabilised commodity prices by increasing volatility or co-movements between commodity prices and those of traditional assets. Interestingly, this conclusion holds irrespective of whether speculators are labelled as “non-commercial” in the CFTC Commitment of Traders report or “professional money managers” (i.e., CTAs, CPOs and hedge funds) in the CFTC Disaggregated Commitment of Traders report. Thus their analysis does not call for a change in the regulation relating to the participation of professional money managers in commodity futures markets.

One last simple example, beyond oil, that commodity futures investing is not driving prices is from the summer of 2012. According to Barclays Capital, commodity index flows were negative approximately $5-6 billion in 2012, but S&P GSCI Grains was up between 30-50%. Why? There was a major drought that destroyed the crop yield. The yield was worst for soybeans from the crop rotation out of the soil, which had the highest return not only from the low supply but from the relatively inelastic demand due to lack of substitutes for soy products.

The posts on this blog are opinions, not advice. Please read our Disclaimers.