My colleagues, Daniel Ung and Xiaowei Kang, recently published an article on alternative commodity strategies. Below is an intro and some highlights:

“Ever since the publication of Professor Harry Markowitz’s work in 1952, modern portfolio theory has been one of the cornerstones of asset allocation and portfolio construction. Until recently, the principal building blocks used to construct investment portfolios have always been individual assets or asset classes. However, recent crises have brought into sharp relief the lack of diversification of many investment portfolios, despite appearances to the contrary. In reality, the correlation between traditional asset classes has increased steadily over the past decade, surging to alarmingly elevated levels during the 2008-09 financial crisis. Indeed, seemingly unrelated assets moved in lockstep, and portfolios once thought to be diversified did not weather the storm. This has led to some investors exploring risk-factor-based asset allocation as a potential new framework for portfolio construction, and looking at alternative beta strategies in an effort to rectify the “defects” of conventional market portfolios.”

Risk Weighting is SUPERIOR to Minimum-Variance

“In addition, it is also apparent from the results that the Risk-Weight strategy was far superior to the Minimum-Variance when seen through the prism of risk and return trade-off. Indeed, commodity prices and volatility often go hand in hand with each other, particularly during periods of supply shortage, when both will spike upwards; this is why the distribution of commodity returns tends to be positively skewed. For this reason, merely targeting the lowest level of volatility appears counterintuitive, and a more satisfactory approach would be to target risk reduction by assigning a risk budget across different commodities and sectors.”

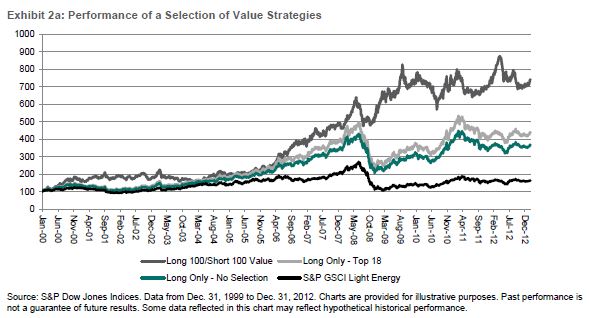

Value Strategies Perform when Fundamentals Diverge

“Despite the attractiveness of value strategies, they can experience periods of underperformance too, especially in periods where commodity fundamentals play a secondary role to the general macroeconomic environment in influencing prices. … It follows from this that such strategies are the most effective when the fundamentals of different commodities are divergent, enabling value to be extracted via active selection.”

Flexible Curve Strategies Perform in Demand Growth Expansion

“Even more dynamic strategies—such as the S&P GSCI Dynamic Roll and the Dow Jones-UBS Roll Select indices—have also garnered much interest in recent years. Unlike their static counterparts, their objective is not only to minimize the effect of contango, but also to maximize the effect of backwardation by adopting a different roll strategy with respect to the term structure of the commodity concerned. In practice, they roll into the futures contract with the lowest implied roll cost when a commodity trades in contango, and roll into the futures contract with the highest implied roll benefit when a commodity trades in backwardation.”

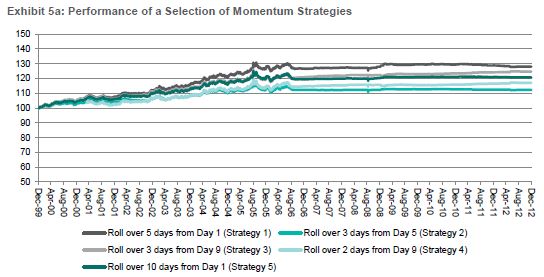

Momentum Is Worth the Risk in Trending Markets

“An important advantage of momentum strategies is that they may provide downside protection during sharp market corrections, while maintaining upside participation during bull markets… Undoubtedly, these strategies also experience periods of subpar performance. In range-bound markets where there is no clear trend, they are unlikely to generate returns. For instance, in the oscillating markets over the last two years or so, momentum strategies—irrespective of their construction—posted disappointing results, as compared with their benchmarks.”

Liquidity / Transparency Tradeoff

“In light of the changing liquidity conditions, a possible improvement to the static [rolling] approach explored above would be to adopt a dynamic rolling schedule in which the roll would occur over a rolling window that is determined on an ongoing basis, rather than defined in advance… adopting different roll schedules can produce very different returns, depending on the time period in question. Obviously, this would come at the expense of transparency. Finally, the analysis finds no evidence to show that lengthening or shortening the rolling window enhances or reduces return on a consistent basis.”

CONCLUSION

“Alternative beta strategies can serve a variety of different investment objectives, which may include reducing volatility or achieving tilts to systematic risk exposures… Two main approaches to alternative beta are reviewed in this paper: the “risk-based approach,” which entails reducing portfolio risk; and the “factor-based approach,” which involves enhancing return through earning systematic risk premia, with a focus on the latter. While alternative beta is fairly well established in equity strategy investing, it is still a nascent concept in commodities. However, as a result of investors’ pursuit of better-diversified portfolios and a recognition that systematic risk factors explain the majority of returns, the development of commodity alternative beta products is gathering pace… From our investigation in this study, there appears to be potential benefit in allocating into alternative beta strategies as part of a portfolio’s commodity allocation, and we find that combining risk-based and factor-based commodity strategies has historically delivered higher return and lower risk than passive long-only strategies on their own.”

Please contact us for more information about these ideas. We’d love to hear from you!

The posts on this blog are opinions, not advice. Please read our Disclaimers.