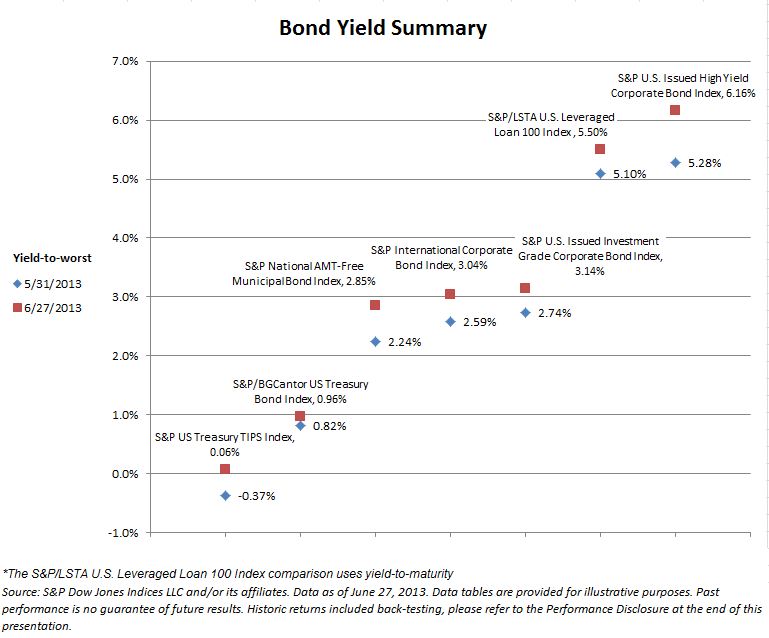

Beginning in May and then aggressively following Fed Chairman Ben Bernanke’s June 19th press conference interest rates rose. The yield on the 10 year treasury both led the way and spooked the markets world-wide. Analysts raised the specter of an early end to QE3, cited Bernanke’s comments and hinted that the central bank was about to abandon the markets. Stocks responded with a sharp slide. Just as it seemed that all were united in castigating the Fed for bringing on the inevitable end to bond bull market, a counter attack was launched.

In the week and a half since the press conference, the Fed has put on a full court press with speeches from two Fed Governors and timely news stories pitching the idea that the rate rise was a case of premature market jitters. Why did rates rise? Some of the comments in Bernanke’s press conference reminded everyone that sooner or later QE3 would end and that, if the Fed’s economic forecast proved reasonably correct there would be no QE4. While no one wanted to be reminded that QE3 would end; there were other factors in the press conference and the market. Bernanke talked about beginning to taper off QE3 if the unemployment rate slipped into the neighborhood of 7%. Some may have confused this with comments from a few months ago that the Fed Funds target would remain zero to 25 bp until the unemployment rate reached 6.5% . (It is 7.6%, at least until the next report on Friday morning). The Fed has two unemployment rate targets – one for QE3 and another for the Fed Funds rate.

More important than the double unemployment rate targets, the Fed confirmed both in the press conference and in those recent speeches that monetary policy will respond to the economy and that it believes the economy is beginning to improve. The Fed’s own forecast for 2014 looks almost rosy at 3% to 3.5% real growth, at or above trend. That growth, rather than monetary policy, will boost interest rates.

Who dun it? The number one suspect is the economy. As to the central bank, one might consider it an accessory before the fact – and offer a compliment for their success.

The posts on this blog are opinions, not advice. Please read our Disclaimers.