U.S. Treasury Bonds:

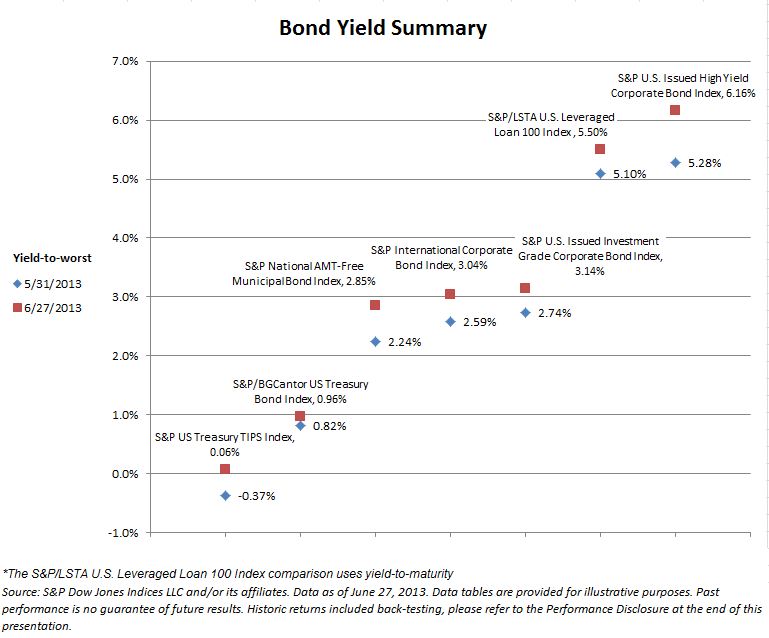

There are just a few hours of trading left to the month of June, but on the whole the month took its toll on fixed income products. Treasuries, as measured by the S&P/BGCantor U.S. Treasury Bond Index, are down -0.91% for the month. Year-to-date this index is returning -1.55%. Yields are up across fixed income products as seen by the Bond Yield Summary Chart.

U.S. Corporate Bonds & Senior Loans:

Only giving up -0.83% for the month, the S&P/LSTA U.S. Leveraged Loan 100 Index stayed out of the fixed income fray and has returned a positive 1.99%, year-to-date.

After reaching a year-to-date low Option Adjusted Spread (OAS) of 378 bps on May 8, the spread for the S&P U.S. Issued High Yield Corporate Bond Index reversed direction. Throughout June the spread rose and peaked on June 24 at 483 bps. Since then it has come down to 464 bps. On the month, the index is returning -2.79%. For the year it is at +0.92%.

The FOMC meeting took its toll on investment grade credit as well. June 19 and 20 showed the two worst daily returns of -0.72% and -0.93%, respectively for the S&P U.S. Issued Investment Grade Corporate Bond Index. The current month-to-date return of -2.71% will be the largest monthly loss since October of 2008’s -5.38%.

The posts on this blog are opinions, not advice. Please read our Disclaimers.