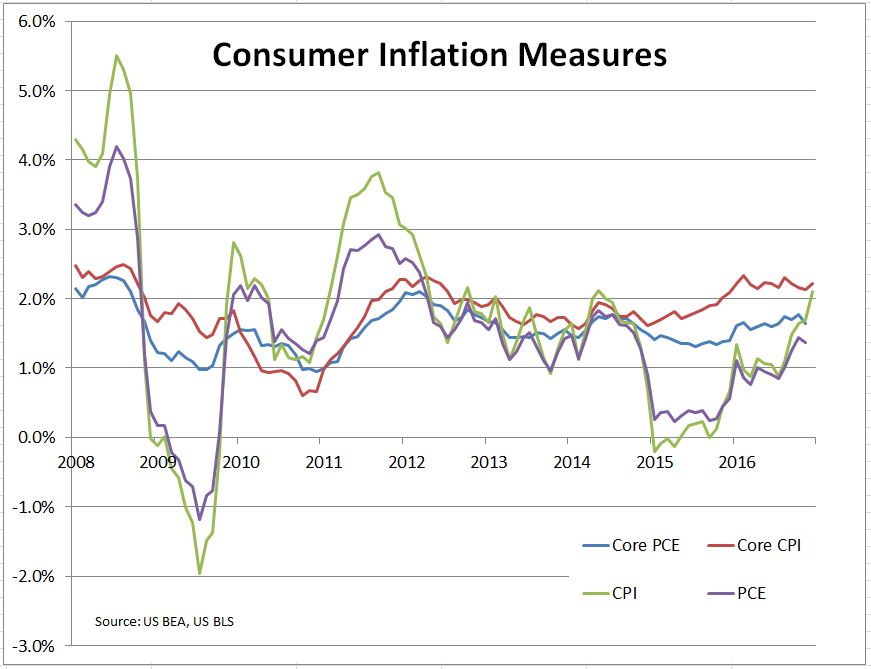

Supported by a stronger economy and higher oil prices, recent readings of inflation are rising. The Fed’s principal gauge, the personal consumption expenditures deflator excluding food and energy (Core PCE) is approaching but still below its 2% target. The more widely recognized CPI and CPI excluding food and energy are both rising and a bit over 2%. (See chart).

While nothing on the horizon suggests a sudden surge in prices, the forces affecting inflation point to a risk that inflation moves higher over the next couple of years. The unemployment rate is under 5% and trending downward and wages are (finally) showing some sign of advancing. Falling unemployment means that the economy is growing more than fast enough to absorb new entrants to the labor force. If this continues and unless labor force participation climbs, the unemployment rate will continue dropping and wages are likely to see more gains. Low and falling unemployment is not the only economic factor behind inflation.

With a growing economy aggregate supply must expand in tandem with aggregate demand if price pressures are to be avoided. The initial impact of the stimulus packages being discussed by the President and Congress will be on demand. Lower taxes mean more spending by consumers and business. Government or private sector spending on infrastructure will add to demand now and to effective supply later. The impact of any stimulus program on inflation or growth depends on how the economy condition at the start of the program. Since the economy is in reasonable shape now, some of that impact will be felt as inflation rather than real GDP growth.

Expectations of future inflation are an important determinant of inflation. Were business to anticipate rising inflation it would be a reason to raise prices. Expectations depend on recent experience of inflation. Since the last time the core CPI inflation rate was over 2.5% was in 2007, inflation expectations are fairly neutral now. The risk is that a gradual increase from the Fed’s 2% target towards 2.5% or 3% will cause people to re-evaluate their expectations of future inflation.

The prospects for inflation also depend on numerous wild cards. If oil prices spike, or collapse, inflation will do the same. If the economy slips into recession, we will return to worrying about deflation; if GDP growth surges inflation will advance. But none of these is predictable.

The posts on this blog are opinions, not advice. Please read our Disclaimers.