The impact of the ECB announcement on March 10, 2016, continues to play out in the bond markets. The governing council decided to establish a new program (the Corporate Sector Purchase Program, or CSPP), which will purchase investment-grade, euro-denominated bonds issued by non-bank corporations established in the eurozone. The goal of the action is to further stimulate the economy. The CSPP will be added to the existing Asset Purchase Program and will be included in the combined monthly purchases, which are to start toward the end of the second quarter of 2016.

Needless to say, this additional program has made an impact: eurozone corporate bonds, as measured by the S&P Eurozone Investment Grade Corporate Bond Index, have returned 0.39% for the month and 2.84% YTD as of May 12, 2016. The S&P Eurozone Quasi & Foreign Government Bond Index has returned 0.59% for the month and 2.26% YTD, while the S&P Eurozone Sovereign Bond Index has returned 0.71% for the month and 2.73% YTD as of the same date.

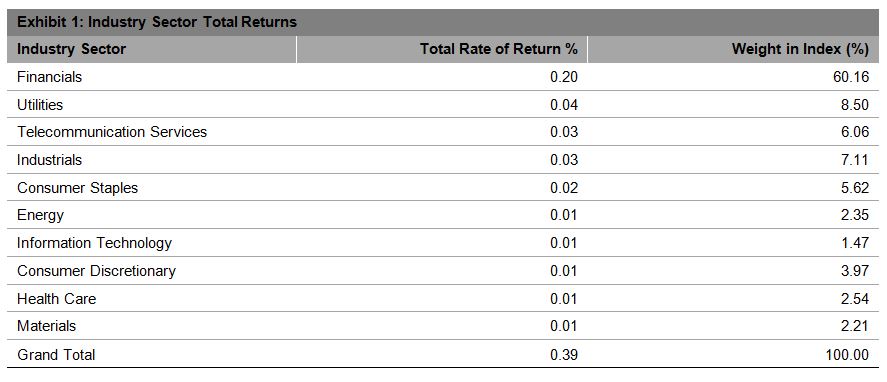

The best-performing sector by far for the month has been financials, which makes up 60% of the index and has returned 0.20% as of the same date, though 31% are banks that do not participate in the CSPP.

Spreads of the S&P Eurozone Investment Grade Corporate Bond Index by rating category show that since mid-February 2016, the Option Adjusted Spreads (OAS) are significantly tighter for the AA, A, and BBB categories. The BBB category has seen the most movement, tightening by 48 bps between Feb. 15, 2016, and May 11, 2016.

Exhibit-2: Eurozone Investment-Grade Corporate Bond OAS by Rating Category

The posts on this blog are opinions, not advice. Please read our Disclaimers.