English speakers have grown to love the German word schadenfreude. But what’s the single word for indifference to the suffering of others? We need to figure this out to describe what’s happening in the US options markets.

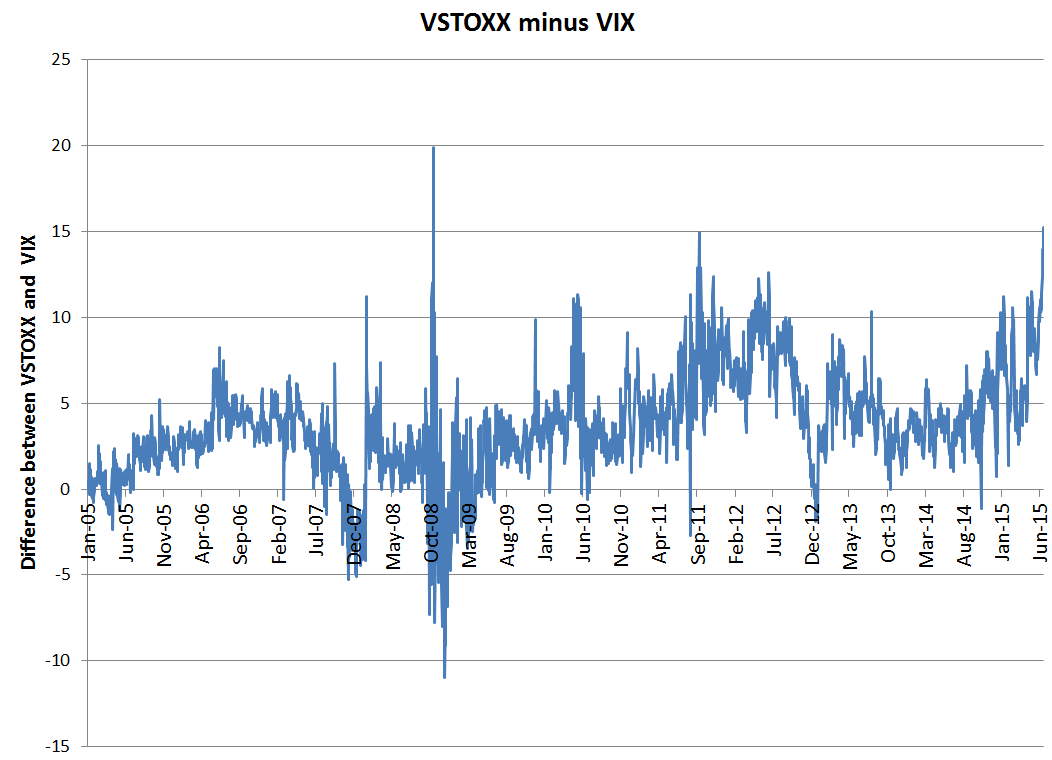

For the past decade, European and US options investors have been sympathetic to each other’s pains. When we chart the EURO STOXX 50 Volatility Index (VSTOXX) against the CBOE Volatility Index (VIX), we can see that the VSTOXX has typically been a little higher than VIX, but that these two indices have moved largely in sync.

Something strange has happened, though, in the past year. VSTOXX and VIX have diverged. As VSTOXX has gone up, VIX has stayed near its floor in the low teens.

This is easier to see when we subtract the daily values of VIX from the daily values of VSTOXX and chart the difference. For only the third time in the past decade, the gap between these two measures has hit 15 volatility points.

The chart below shows the same measure, but just over the past 18 months. The trend is unmistakable.

Why this decoupling? One explanation I have heard is that investors see the troubles in Greece more as a political crisis than a financial one. Financial crises, such as the one that rocked the world in 2008, tend to more directly affect financial institutions that span multiple regions. Political crises, on the other hand, are less likely to spill over borders. Or so the theory says. Personally, I have difficulty seeing the difference between the two types of crises in this case.

The posts on this blog are opinions, not advice. Please read our Disclaimers.