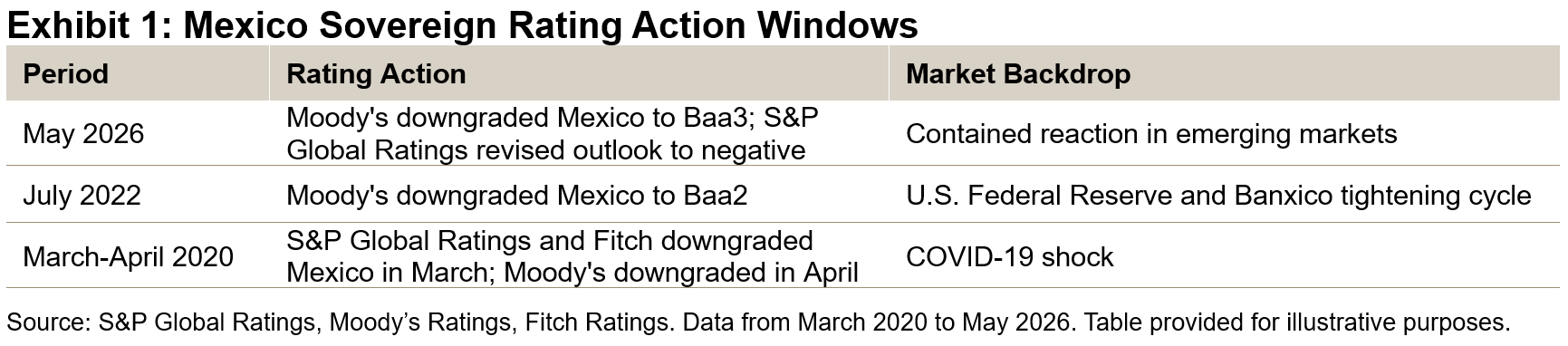

Mexico’s recent rating actions have brought renewed attention to the country’s sovereign credit profile. Moody’s downgraded Mexico in May 2026, while S&P Global Ratings revised its outlook to negative. For fixed income investors, the key question is not only what changed from a ratings perspective, but also how those events translated into market performance.

Bond indices provide a useful lens through which to assess these effects. Comparing Mexico’s rating actions in 2020, 2022 and 2026, the data suggest a nuanced conclusion: Mexican risk repriced following these events, but the market reaction has generally appeared contained rather than disruptive.

Sovereign Bonds: Repricing, but Context Matters

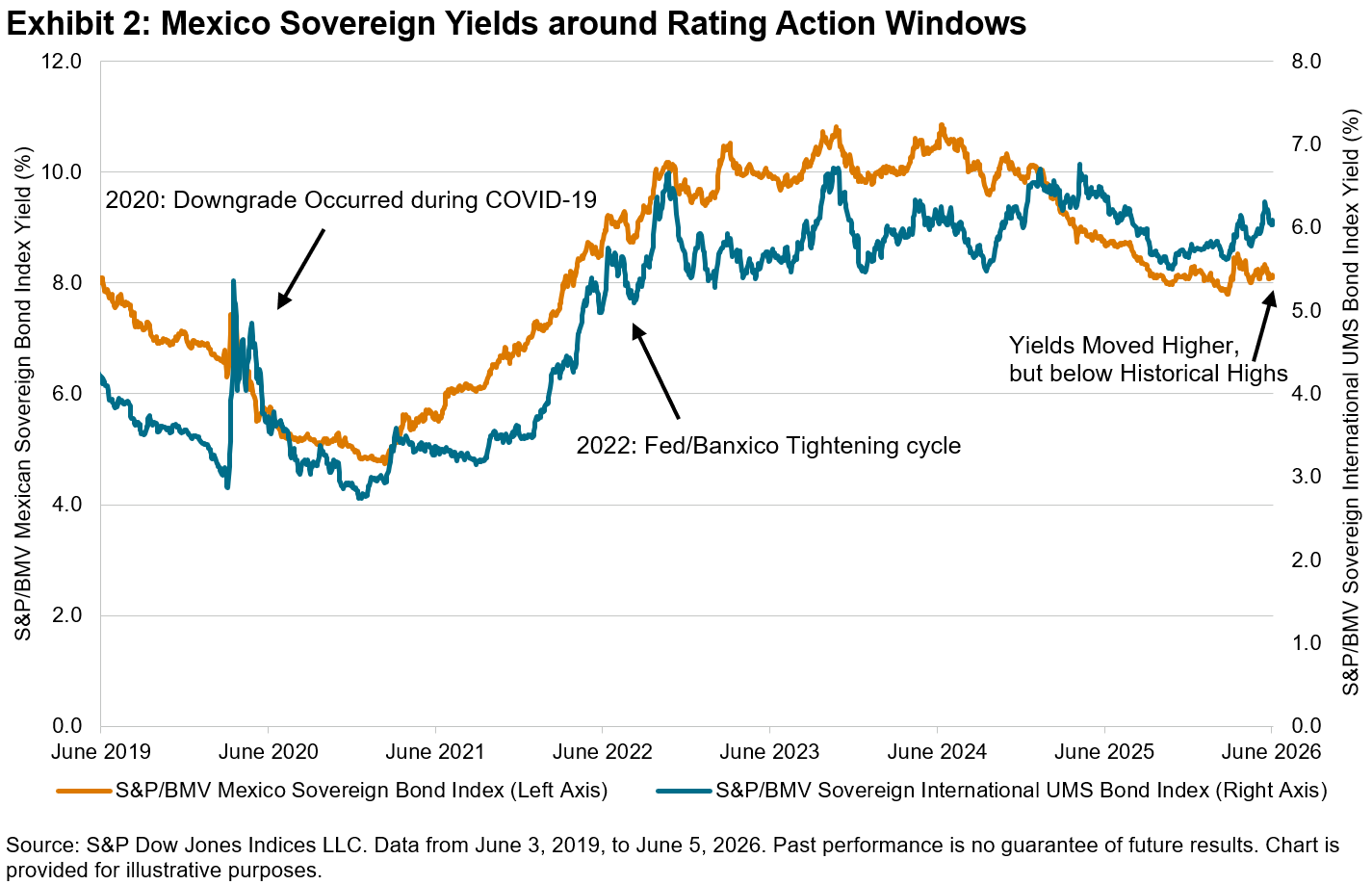

Mexican sovereign yields moved higher around the rating actions, but each episode occurred against a different market backdrop.

In 2020, S&P Global Ratings and Fitch downgraded Mexico in March, followed by Moody’s in April. However, those rating actions coincided with the global COVID-19 market shock, making the moves difficult to separate from broader risk aversion.

In July 2022, Moody’s downgraded Mexico again during a period of aggressive tightening by the Fed and Banxico, so higher yields may have reflected a combination of both interest rate pressures and credit concerns.

In 2026, yields rose around the May rating downgrade, suggesting some repricing of sovereign risk. However, the increase remained below levels observed during periods of prior market stress, pointing to repricing rather than a broader market dislocation.

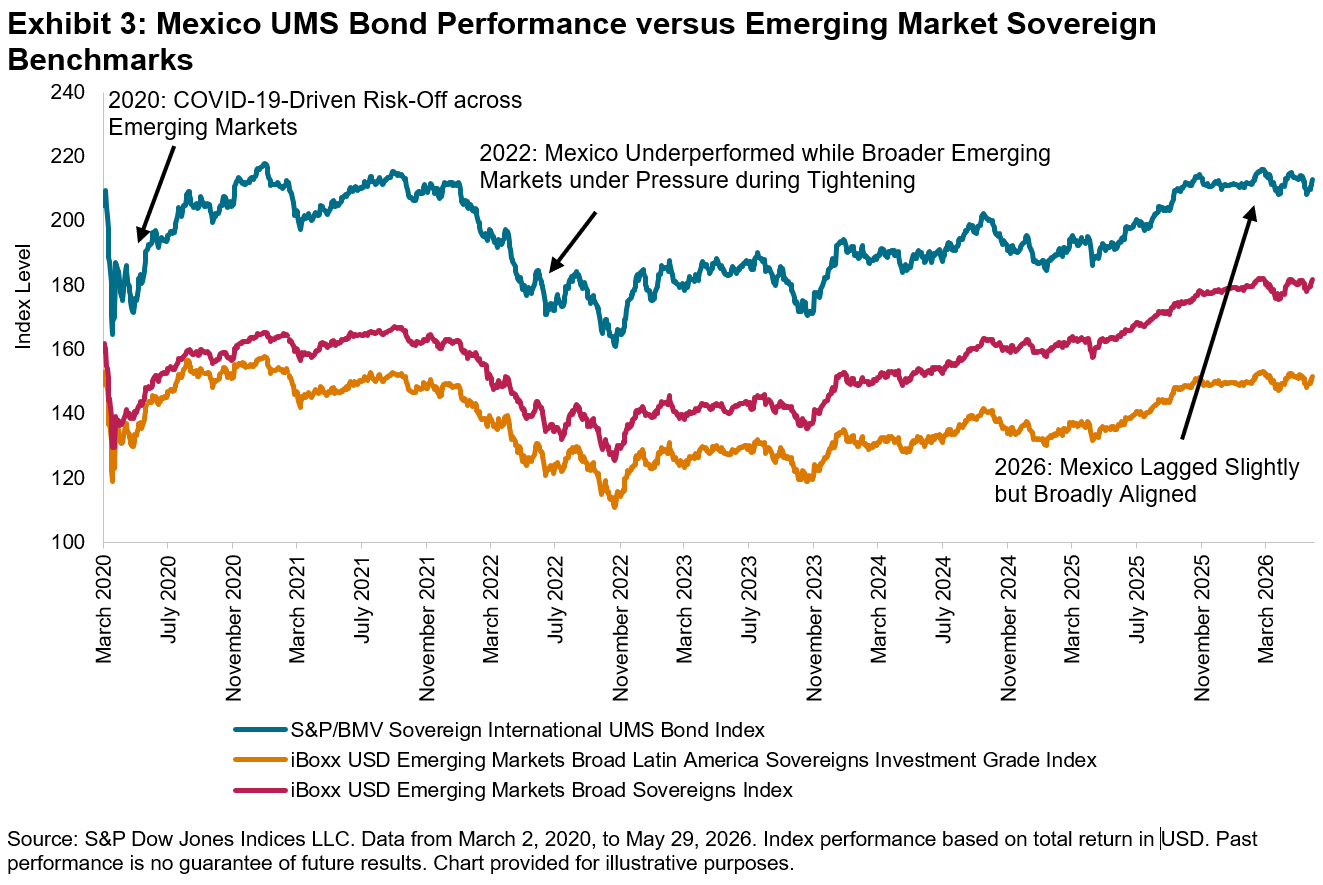

Relative Performance: Broadly Aligned with Emerging Market Benchmarks

Total return performance tells a similar story. UMS bonds saw some weakness around rating action windows, but performance generally moved in line with Latin American and broader emerging market sovereign benchmarks.

In 2020, UMS bonds sold off sharply, broadly in line with Latin American and emerging market sovereigns during the COVID-19 shock. In 2022, Mexico showed modest underperformance around the July downgrade, but other emerging market sovereigns were also under pressure amid Fed tightening. In 2026, Mexico lagged modestly during the May pullback, but its performance remained broadly aligned with emerging market sovereign benchmarks, with early signs of narrowing in June.

The key message is that Mexican sovereign bonds repriced, but index performance does not suggest a standalone or strong Mexico selloff.

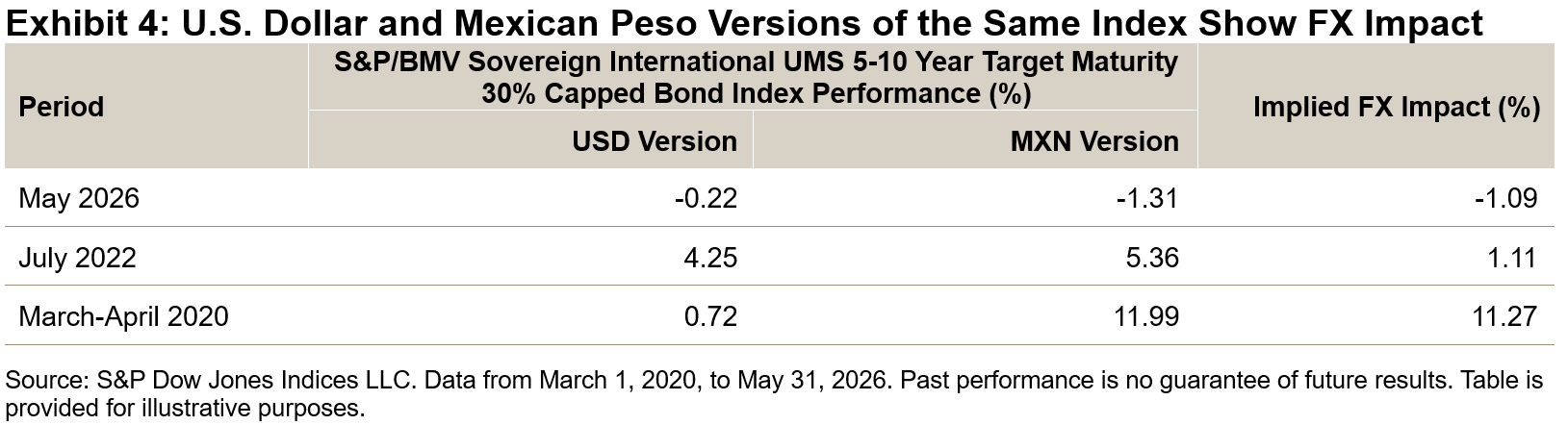

FX Translation: S&P/BMV Index Versions Highlight the Currency Effect

Foreign exchange (FX) matters for Mexican peso-based holders of U.S. dollar-denominated Mexico sovereign debt. Comparing the U.S. dollar and Mexican peso versions of the S&P/BMV Sovereign International UMS 5–10 Year Target Maturity 30% Capped Bond Index helps isolate the currency effect. Across the rating action windows reviewed, FX either reduced or enhanced performance reported in Mexican pesos.

In May 2026, Mexican peso strength reduced performance reported in that currency by approximately 1.09%, while in July 2022 and March-April 2020, FX translation added to Mexican peso-reported performance.

The index comparison shows that the credit signal did not consistently translate into Mexican peso weakness; rather, FX appeared to be influenced by broader factors.

Conclusion: Isolate the Drivers of Mexican Sovereign Debt Performance

The practical takeaway is that evaluating Mexican sovereign debt could involve more than a single risk factor. A more precise view distinguishes between sovereign credit repricing, local rates, broader emerging market risk sentiment and currency effects.

Mexico’s rating headlines matter, but the index data suggest they may be better viewed in a broader market context. Across the periods observed, Mexican UMS bonds generally moved in tandem with Latin American and broader emerging market sovereign benchmarks.

The author would like to thank Sofia Lozada for her contributions to this blog.

This content may be AI-assisted and is composed, reviewed, edited, and approved by S&P Global.

The posts on this blog are opinions, not advice. Please read our Disclaimers.