For more than a century, index providers have served a specific function in capital markets: define the standard, calculate the benchmark and the data, license the IP. The infrastructure was built for a world of market opens and closes, batch file delivery, and intermediated access. That infrastructure continues to work extraordinarily well.

But a parallel system is being built alongside it, and it operates on fundamentally different assumptions.

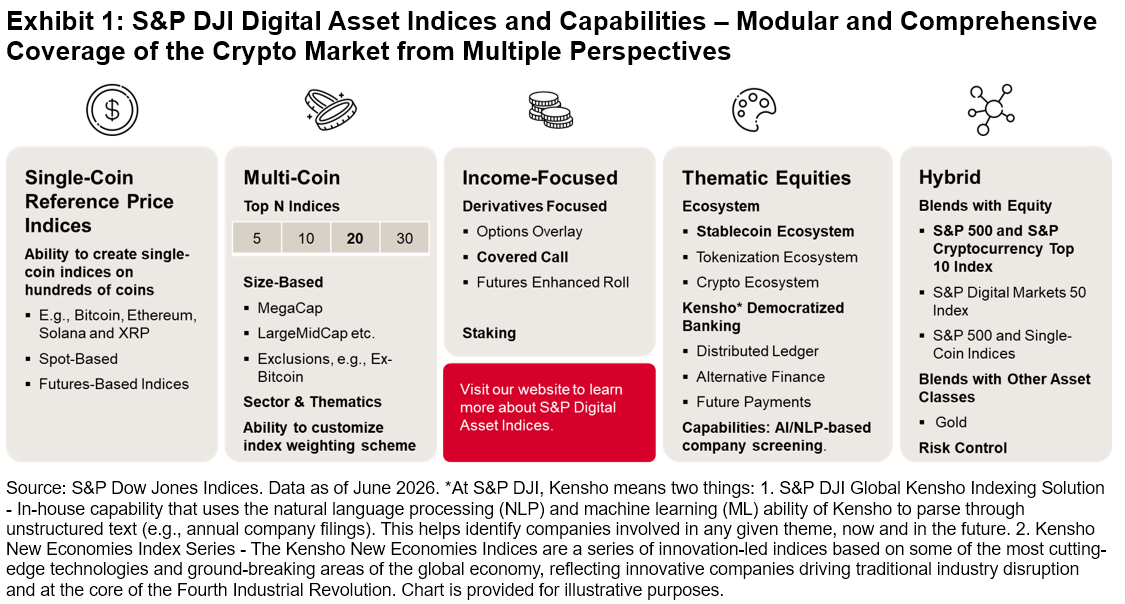

On-chain markets run 24/7. Settlement is programmable. Capital moves across protocols without intermediaries. Products that have no equivalent in traditional markets (perpetual futures without expiration, cross-chain margining, prediction markets scaling to billions in monthly volume) are being created and adopted at a pace that traditional market structure was never designed to match. Tokenized versions of traditional instruments (treasuries, credit, equities) are now accessible on-chain, reaching approximately $30 billion1 and growing rapidly. These are not new asset classes. They are existing assets delivered through new, globally accessible, programmable infrastructure.

S&P Dow Jones Indices has created value by setting the benchmarks markets trust – through transparent methodologies, disciplined governance, and benchmark integrity that institutions rely on to allocate capital with confidence. That same value is now increasingly essential in DeFi, where market growth depends on trusted data, clear standards, and transparent infrastructure.

When spot crypto ETFs launched in the U.S., the benchmarks behind them came from crypto-native providers, not from traditional index firms. Those providers built real-time calculation capability, secured regulatory standing, and locked in relationships with ETF issuers while most of us were still evaluating the space. That is a competitive fact worth acknowledging, not explaining away.

However, the next wave of on-chain financial products will need index standards for asset classes that don’t yet have them: DeFi protocol benchmarks, tokenized equity indices, on-chain structured products. And they will need those standards from providers with the governance, methodology, and institutional credibility that this industry was built on. That is where traditional index providers can meaningfully progress the industry, if we move with intention.

Moving with intention means three things.

First, it means becoming a participant in on-chain infrastructure, not just a licensor to it. Publishing index data through oracle networks. Running validators. Understanding staking not as a speculative activity but as a utility that generates data, connectivity, and credibility within protocol ecosystems. This is unfamiliar territory for the traditional index industry. It requires new models, not the abandonment of old principles.

Second, it means building technology that meets markets where they are. End-of-day batch calculation served a world that closed at 4PM. On-chain markets never close. Real-time, continuous, API-native data delivery is not a feature request. It is the minimum viable infrastructure for credibility.

Third, it means recognizing that standards lock in early. The index methodologies embedded in smart contracts and DeFi protocols today will be the defaults that institutional capital builds on tomorrow. Waiting for the market to mature before engaging is a strategy for irrelevance. The S&P 500® became the global equity benchmark not only because it was the best U.S. large cap equity index when passive investing scaled. But also, because it was already the standard.

The same dynamic is playing out on-chain. The question is whether the next generation of financial market standards will carry the credibility of the institutions that built this industry, and as the world’s leading index provider, we’re aiming to lead the charge.

From Strategy to Execution

As demand for broader, diversified exposure to DeFi continues to grow, S&P Dow Jones Indices serves as a bridge between markets and investors—transforming complexity into transparency, investability, and governance across digital asset markets.

Some of our work is already visible:

- Facilitating fund tokenization. In July 2025, S&P DJI collaborated with Centrifuge to license the S&P 500 for fund tokenization, leading to the first licensed on-chain S&P 500 index fund in September 2025.

- Pioneering indices on-chain. In early 2026, S&P DJI and Kaiko announced the tokenization of the iBoxx U.S. Treasuries Index on the blockchain. The significance is not only symbolic. It marks the first time a major index provider has made a financial benchmark available as a native digital asset, with embedded index data distribution and permissioning ready for licensing.

- Innovative digital asset indices. In October 2025 the S&P Digital Markets 50 Index was launched, combining cryptocurrencies and publicly traded crypto-linked equities into a single benchmark. That approach reflects an increasingly important market reality: the boundary between digital assets and traditional securities is becoming less useful than the broader ecosystem view investors increasingly need.

These are not side projects. They are early signs of what it looks like when an index provider chooses to help shape on-chain finance rather than simply respond to it.

More broadly, as digital assets and tokenized markets continue to institutionalize, S&P Global is uniquely positioned as an enabler between TradFi and DeFi. Through our sister-divisions, Stablecoin Stability Assessments (now on-chain through Chainlink), the first credit rating of a DeFi protocol (Sky Protocol), and tax solutions for digital assets are among the early solutions S&P Global brings to the digital asset community.

If the next era of capital markets will be more programmable, more continuous, and more globally accessible, then the role of the index provider must evolve with it. The opportunity is not just to extend existing benchmarks into new channels. It is to bring the transparency, governance, and institutional trust that defined the last century of market infrastructure into the one now being built.

1 Tokenized Real-World Assets Hit $30 Billion as Crypto Market Matures – CoinCentral

The posts on this blog are opinions, not advice. Please read our Disclaimers.

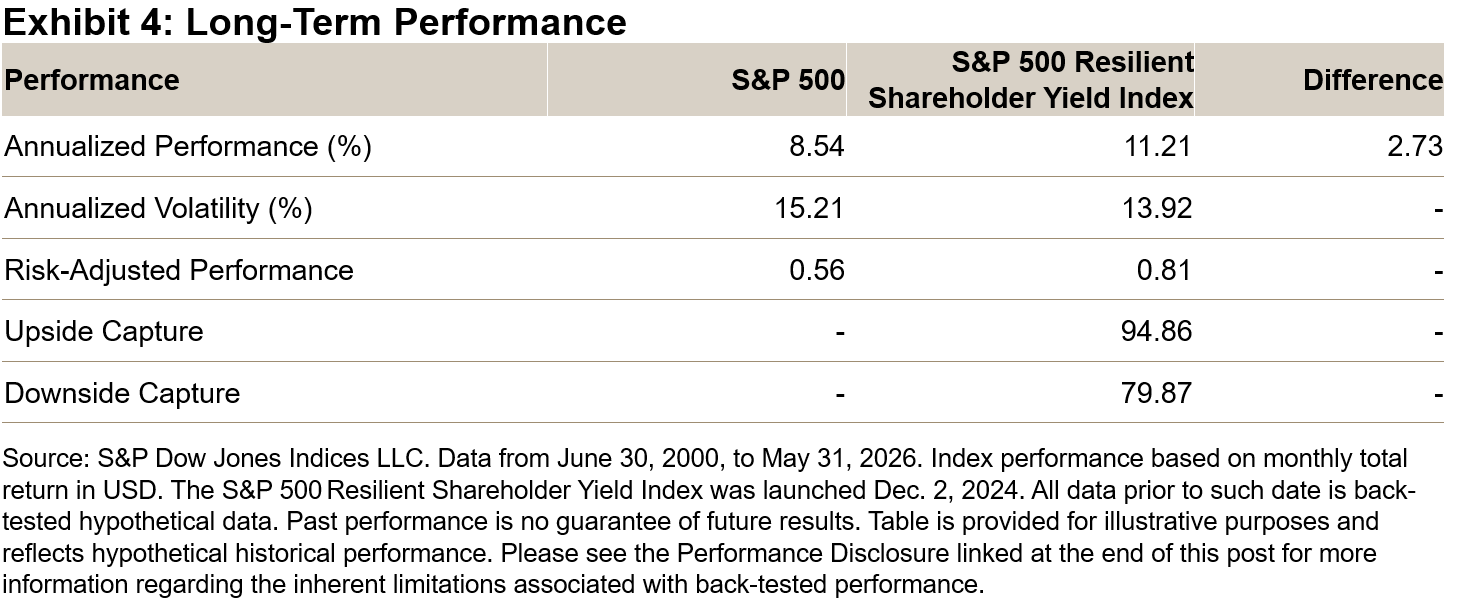

Long-Term Performance Characteristics

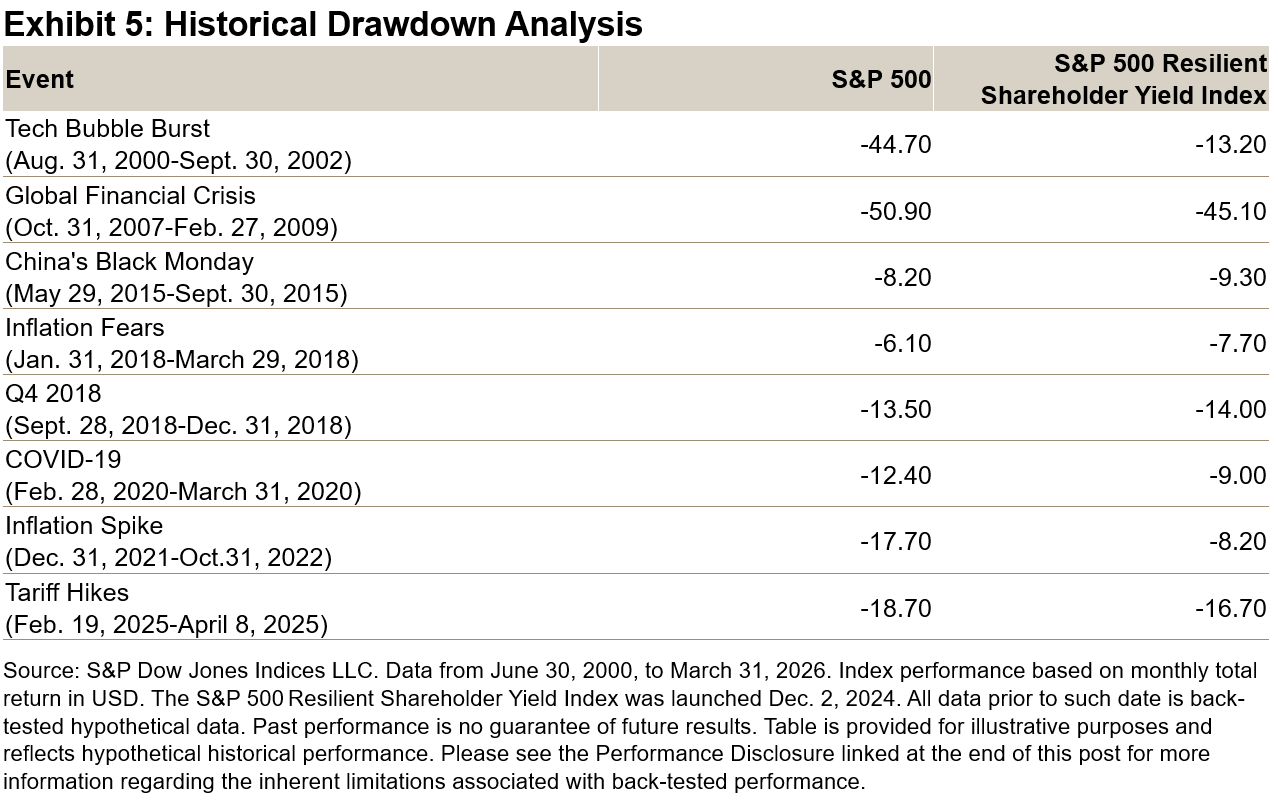

Long-Term Performance Characteristics