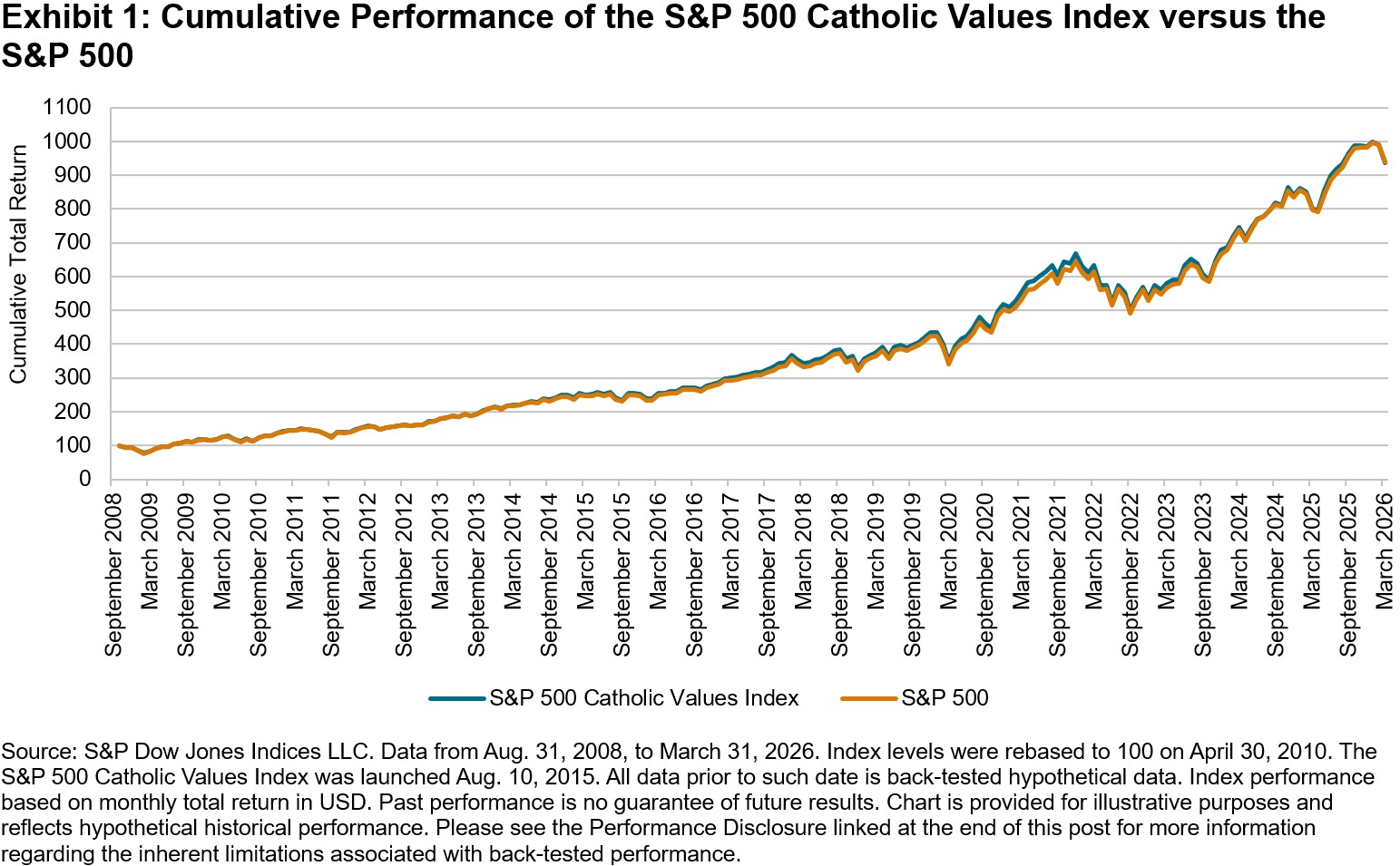

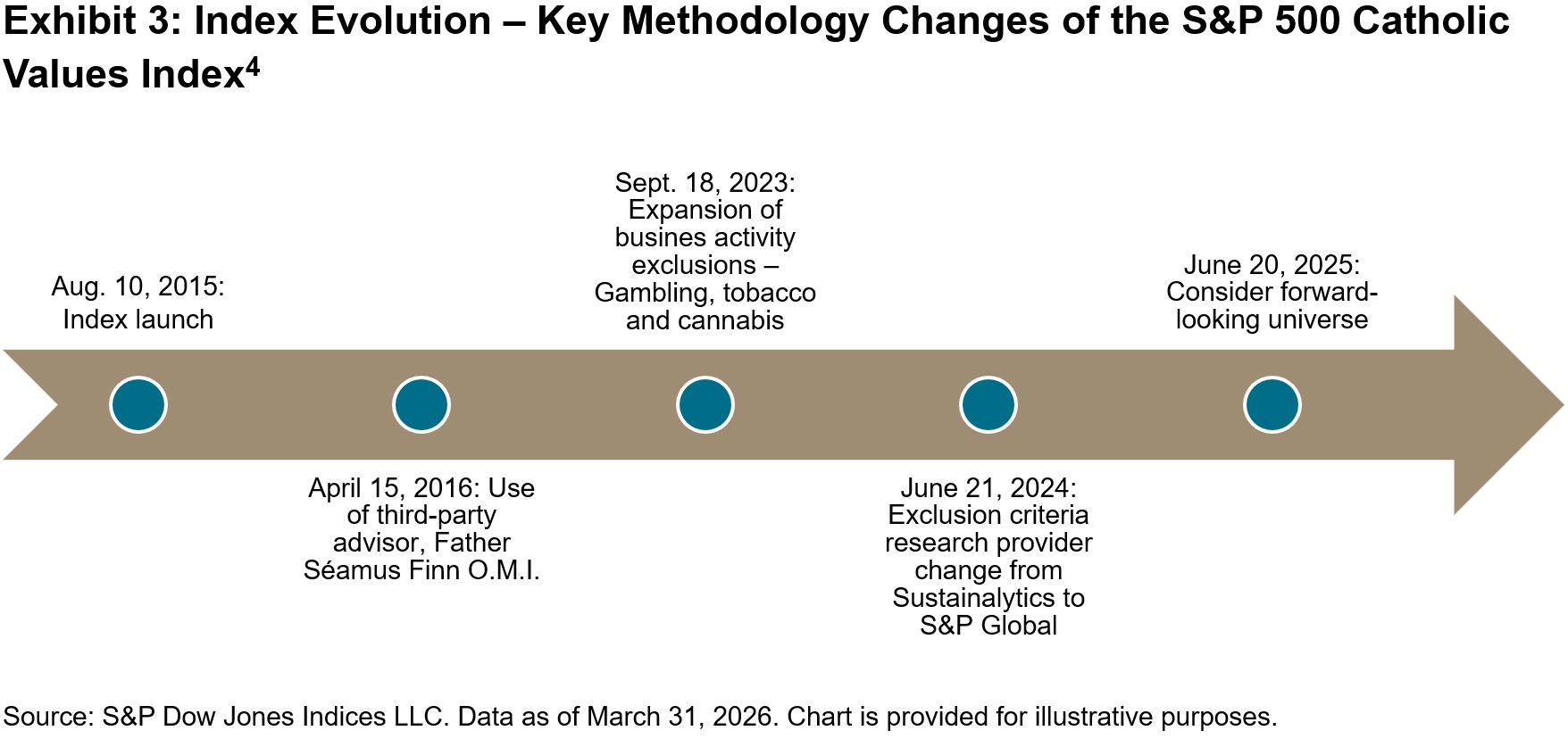

The S&P 500® Catholic Values Index has a decade-long track record that highlights the historical effectiveness of its sector-neutral approach to values-based indexing.

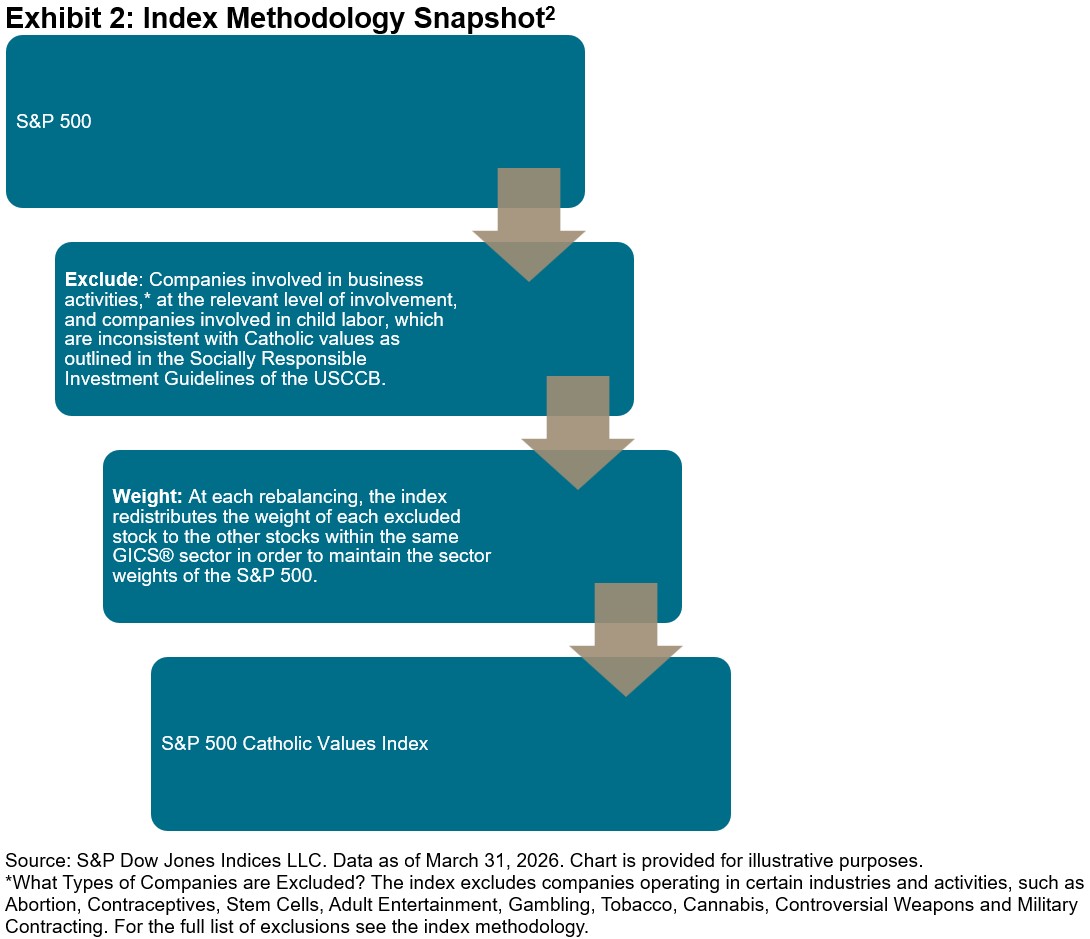

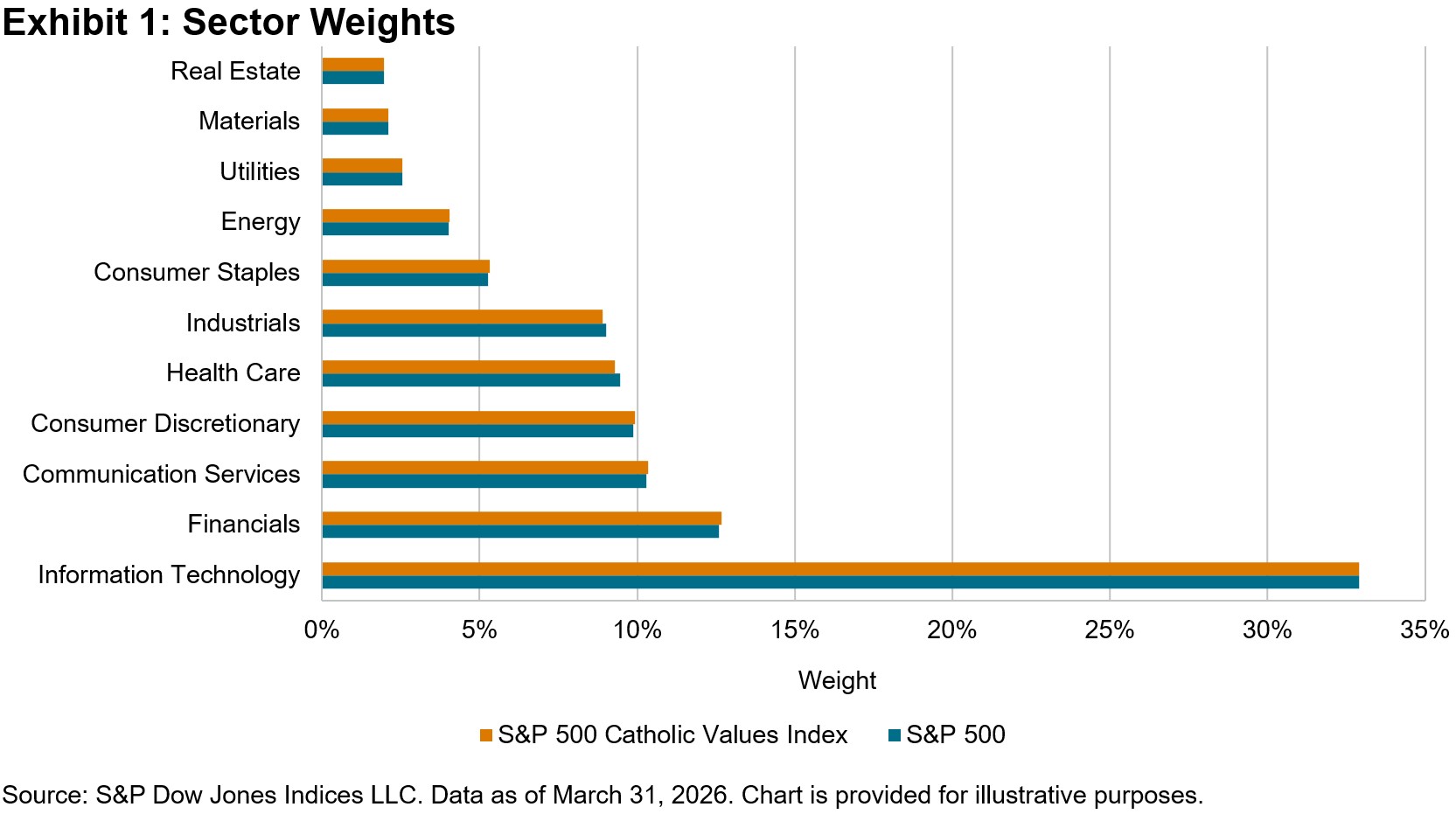

An important feature of the S&P Catholic Values Indices Methodology is its sector weight redistribution approach. Rather than allowing exclusions to create potential sector tilts, the weights of excluded companies are proportionally distributed within their respective GICS® sectors, helping the index maintain its broad market representation. This approach leads to sector neutrality, which is evident in Exhibit 1.

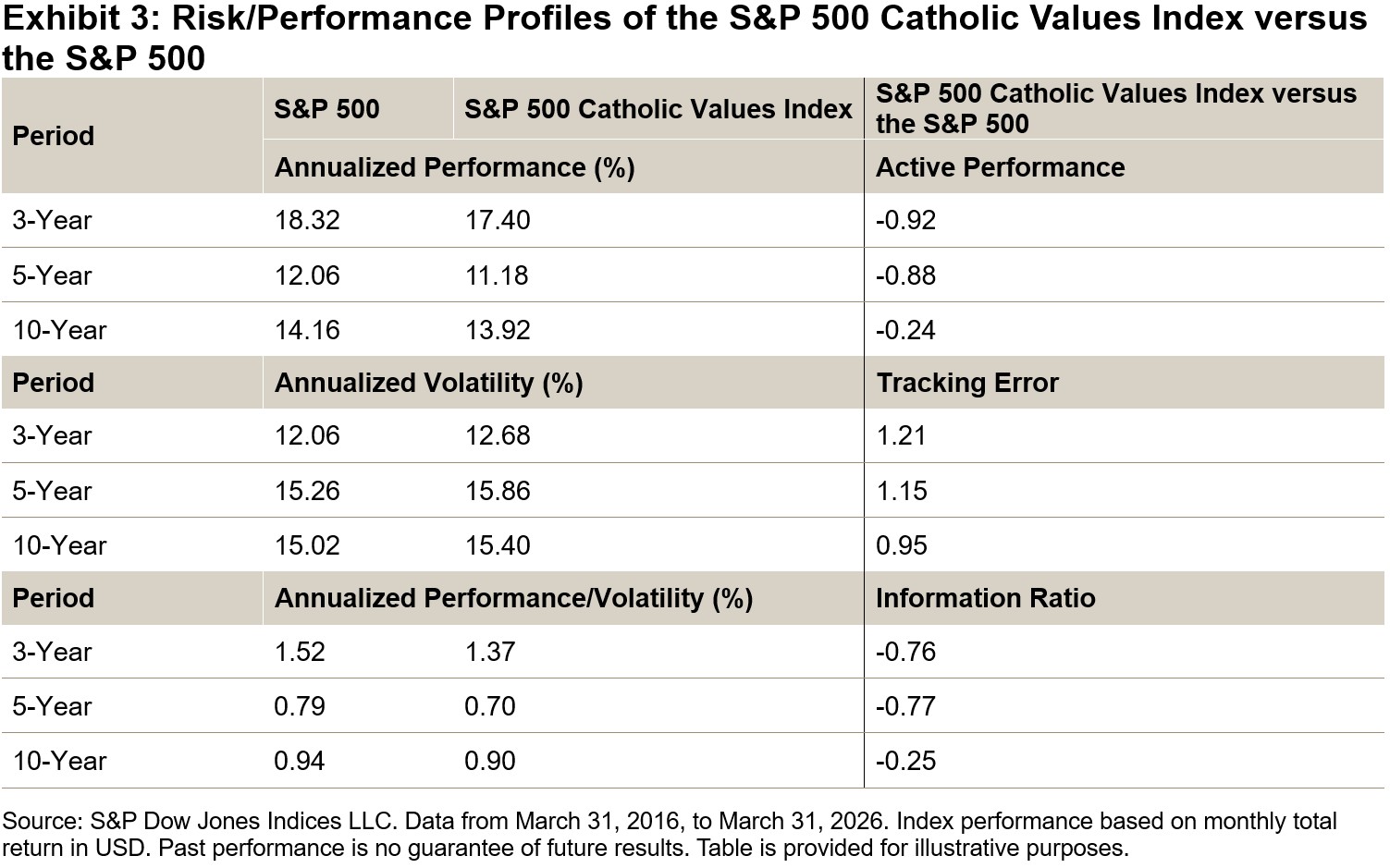

This sector approach has helped the index maintain low tracking error versus the S&P 500 historically, which may be a relevant consideration when evaluating values-based mandates. Over the past decade, the S&P 500 Catholic Values Index has maintained a tracking error within 1.4% of the S&P 500 while excluding an average of 52 companies. During the latest rebalance, effective after the close of March 20, 2026, 55 companies were excluded, representing 12.70% of the S&P 500 as of the reference date. This represents approximately 87% market-cap coverage of the S&P 500.

![]()

The S&P 500 Catholic Values Index has demonstrated risk-adjusted performance comparable to that of the S&P 500 since the index was launched, with annualized performance of 0.86% versus 0.82% for the S&P 500. The historical comparison of the index’s characteristics demonstrates its consistency compared with the benchmark.

The S&P 500 Catholic Values Index’s decade of performance history demonstrates that values-based indices may not mean compromised performance relative to the benchmark. As a result, the S&P 500 Catholic Values Index may serve as a relevant benchmark for those seeking to align religious values with passive investing strategies.

The posts on this blog are opinions, not advice. Please read our Disclaimers.