As investors across the globe have wrestled with the impact of AI on the U.S. tech sector, valuation concerns, inflation jitters and more, U.S. markets have underperformed their Pan Asian peers. The S&P 500® has trailed the S&P Pan Asia BMI by 8% YTD,1 however the tide may be turning. Thanks to optimism surrounding easing geopolitical concerns, The 500® notched three consecutive record highs on April 15-17, 2026.

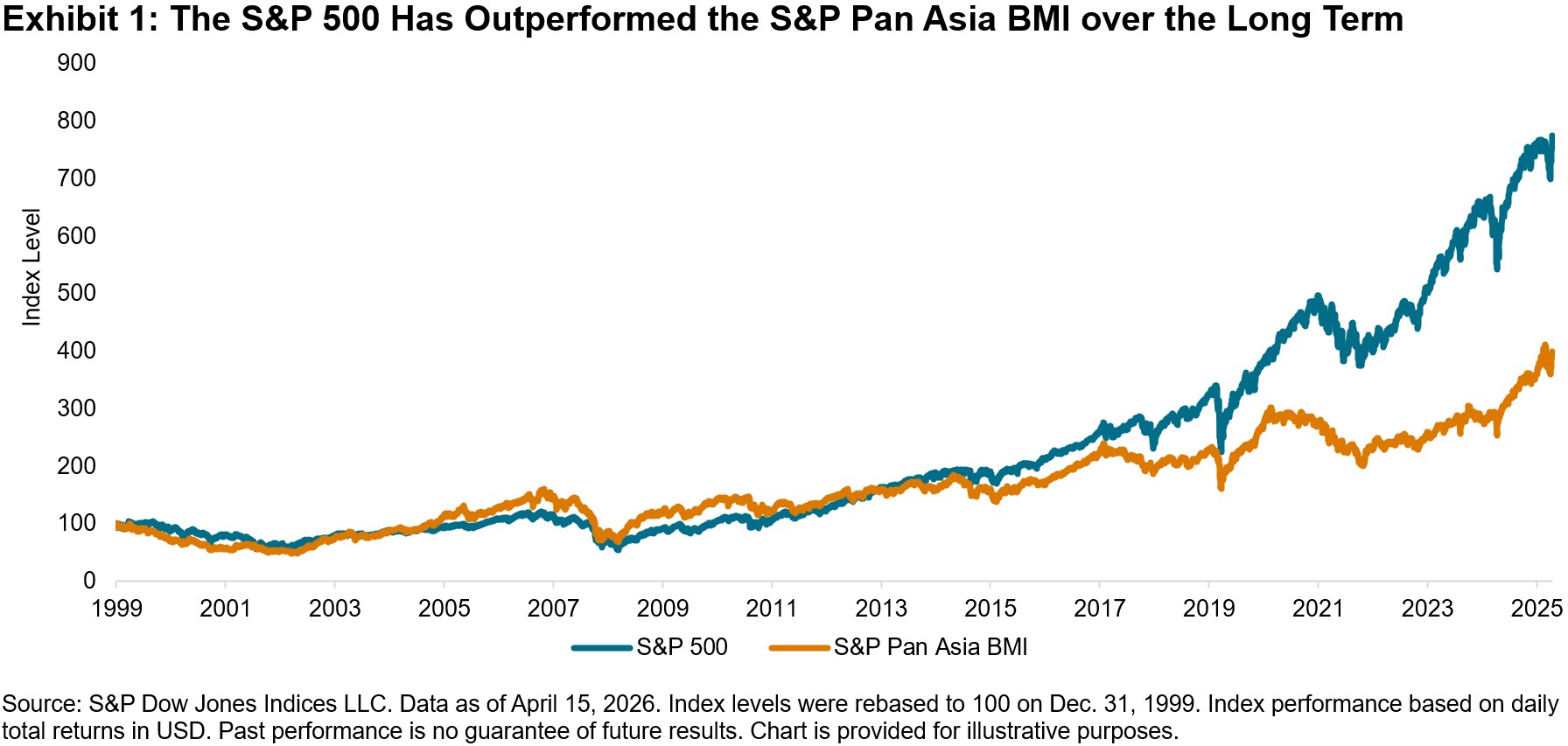

Notwithstanding recent market gyrations, U.S. equities have outperformed their Pan Asian counterparts over the long term,2 with the S&P 500 outperforming the S&P Pan Asia BMI by a cumulative 360% since 2000.

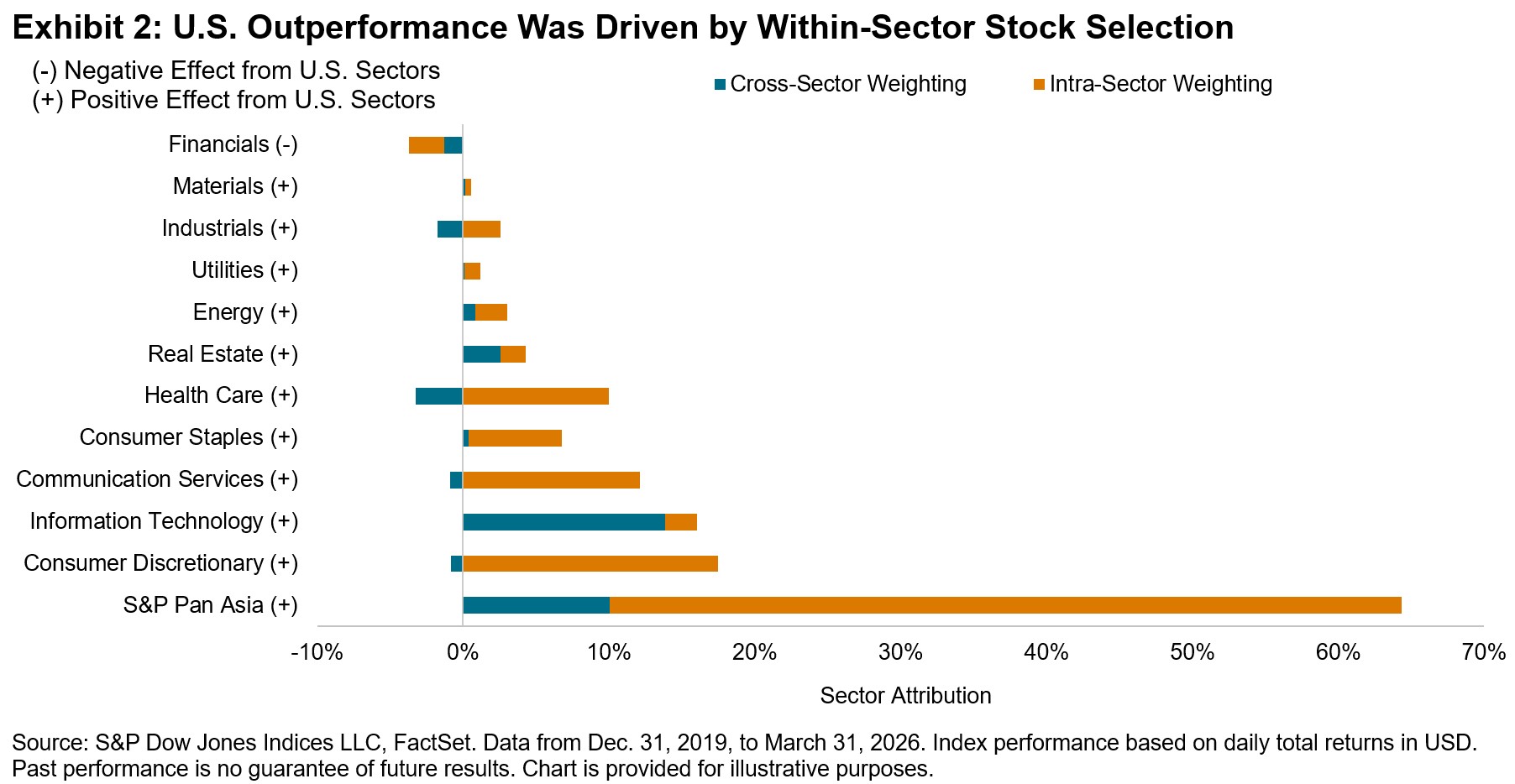

Considering that U.S.-domiciled stocks accounted for a majority of the market cap in 10 of the 11 sectors in the S&P Global BMI as of year-end 2024,3 adopting a sectoral perspective4 can be helpful to understand the sources of U.S. equity outperformance compared with equities in Pan Asia. Exhibit 2 shows that much of this outperformance can be attributed to within-sector stock selection, particularly in the Consumer Discretionary and Communication Services sectors, which house many of the Big Tech names that have dramatically outperformed in recent years.

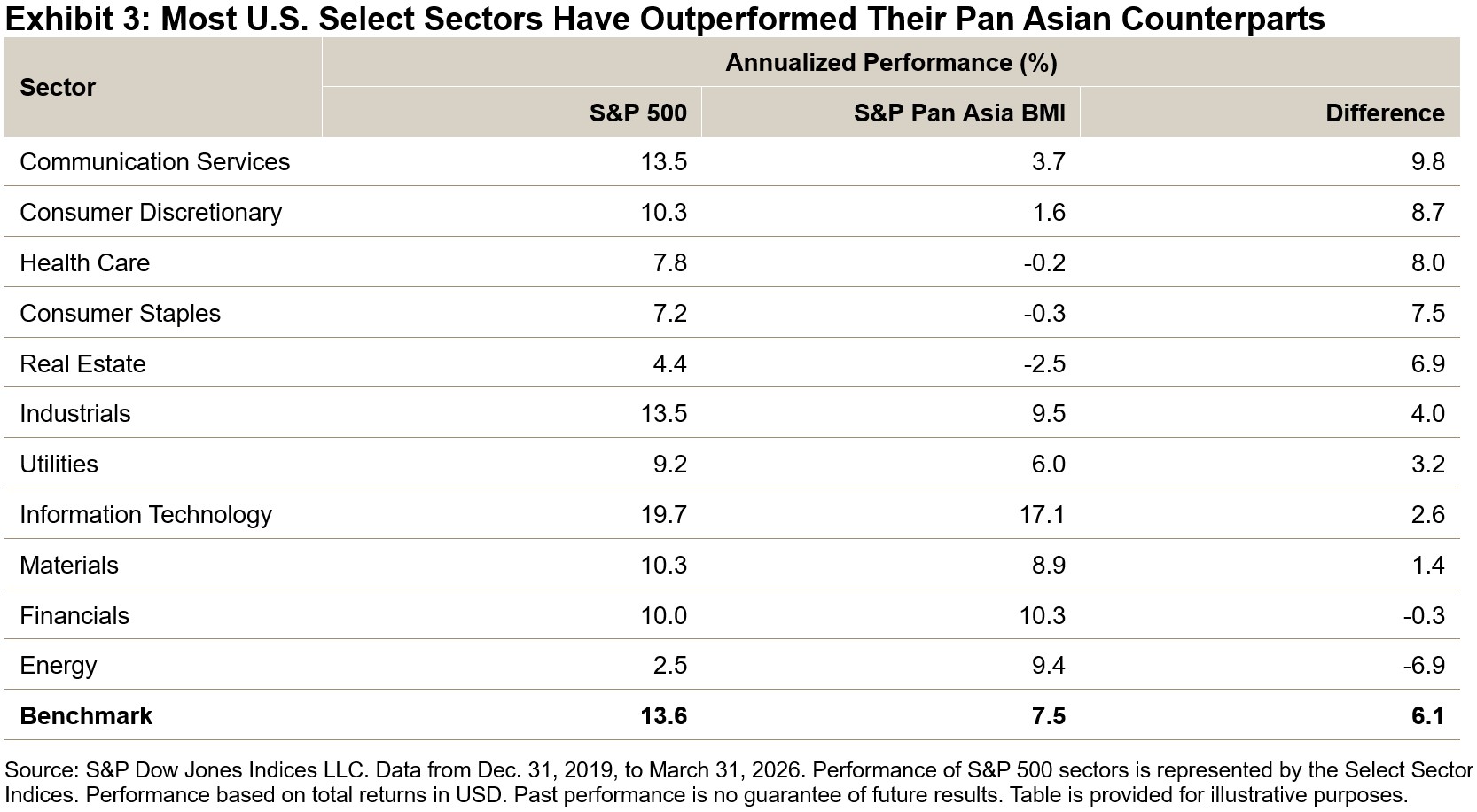

On a more granular level, Exhibit 3 compares the performance of S&P Pan Asia BMI sectors versus the Select Sector Indices, which track the performance of S&P 500 sectors while capping the weight of individual stocks. The exhibit shows that 9 of the 11 Select Sector Indices outperformed S&P Pan Asia BMI sectors and 8 of the 11 Select Sector Indices outperformed the S&P Pan Asia BMI overall. Outperformance was led by the Communication Services and Consumer Discretionary sectors, consistent with the results observed in Exhibit 2.

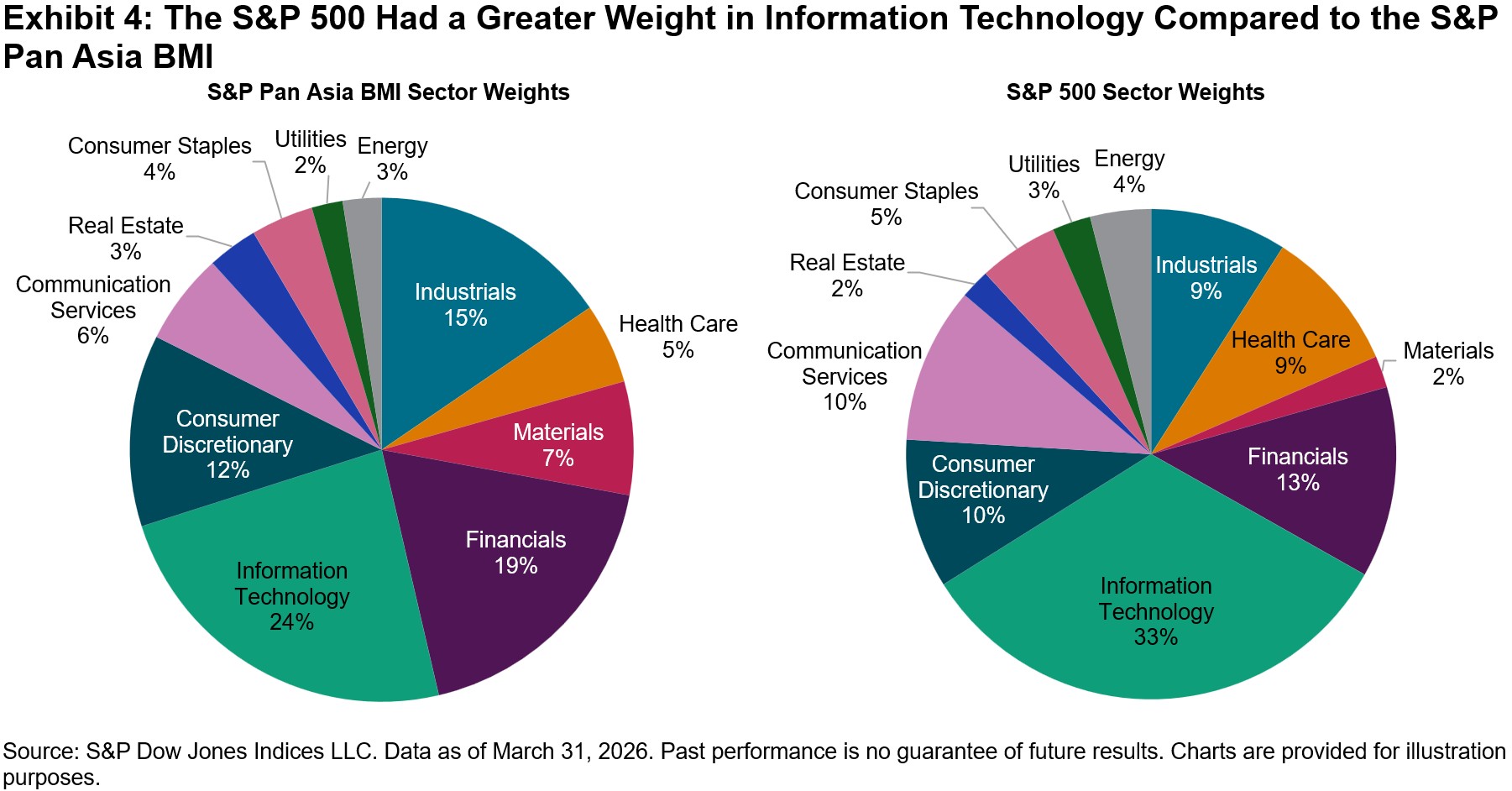

In addition to outperformance from stock selection within sectors, the attribution in Exhibit 2 shows that the U.S. also benefited from selection across sectors, particularly in Information Technology, which contributed more than one-fifth of U.S. outperformance relative to Pan Asia. Exhibit 4 compares the sector weights of the S&P 500 and the S&P Pan Asia BMI. The U.S. had a greater weight in the Information Technology sector, while S&P Pan Asia had greater weights in Industrials and Financials.

The Select Sector Indices can provide APAC investors with a framework for analyzing U.S. sector-level performance, and provide insights into sectors that include some of the largest companies in the world.

1 As of April 15, 2026.

2 Pathak, Amit. “Why Does The S&P 500 Matter to APAC?” S&P Dow Jones Indices LLC. April 25, 2025.

3 Weng, Fei. “U.S. Sector Relevance to China.” S&P Dow Jones Indices LLC. March 6, 2024.

4 Flaherty, Liam. “Stocks, Sectors and Success?” S&P Dow Jones Indices LLC. Feb. 3, 2026.

The posts on this blog are opinions, not advice. Please read our Disclaimers.