For over a decade, the S&P 500® Catholic Values Index has served as a rules-based tool to help market participants that seek to align their investments with their values. The index was officially launched on Aug. 10, 2015, and excludes companies involved in activities inconsistent with the Socially Responsible Investment Guidelines of the U.S. Conference of Catholic Bishops (USCCB).1

To ensure ongoing adherence to these guidelines, S&P Dow Jones Indices consults with Father Séamus Finn O.M.I., Chief of Faith Consistent Investing at the Oblate International Pastoral Investment Trust, regarding the consistency of the S&P 500 Catholic Values Index methodology with USCCB standards.

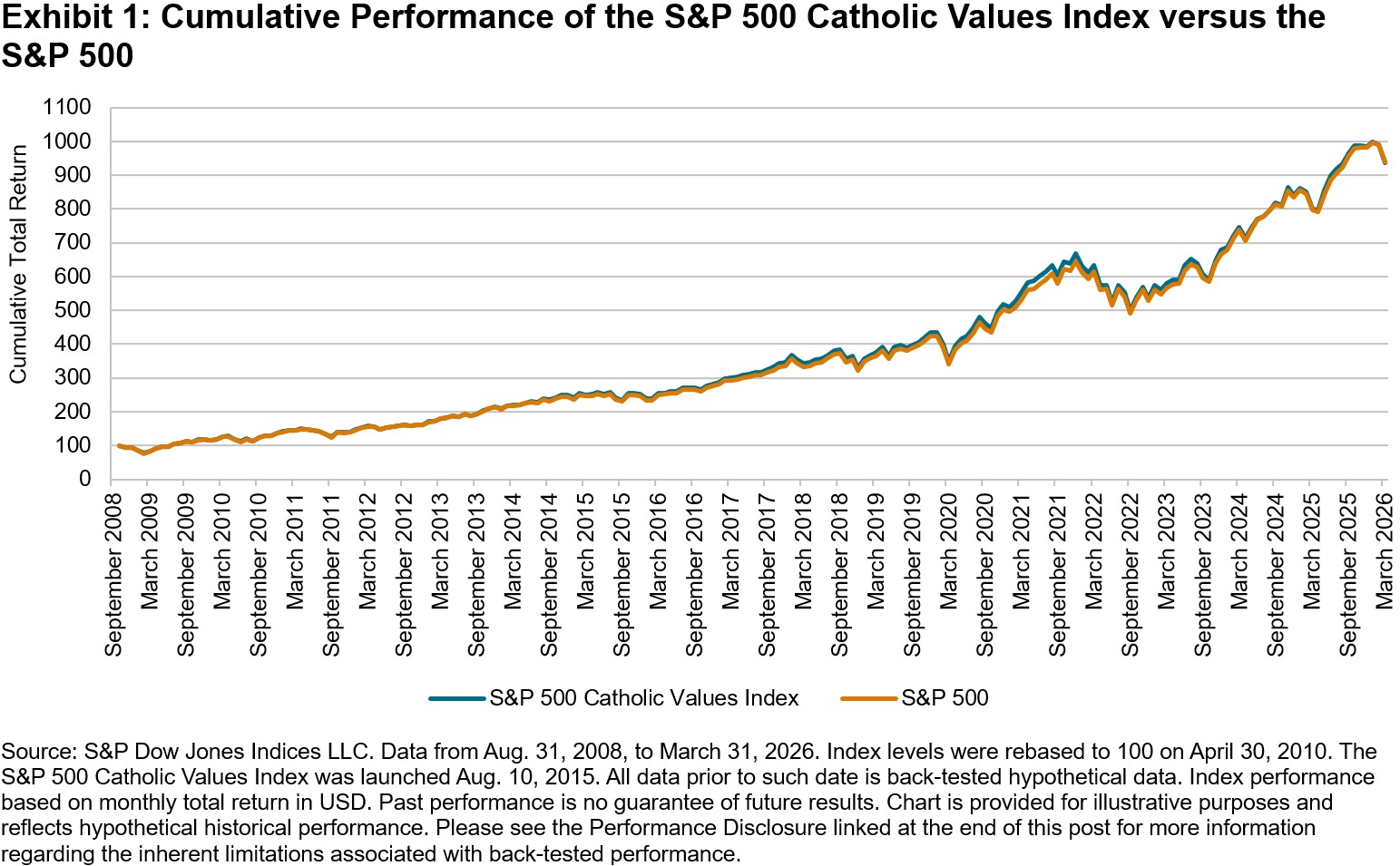

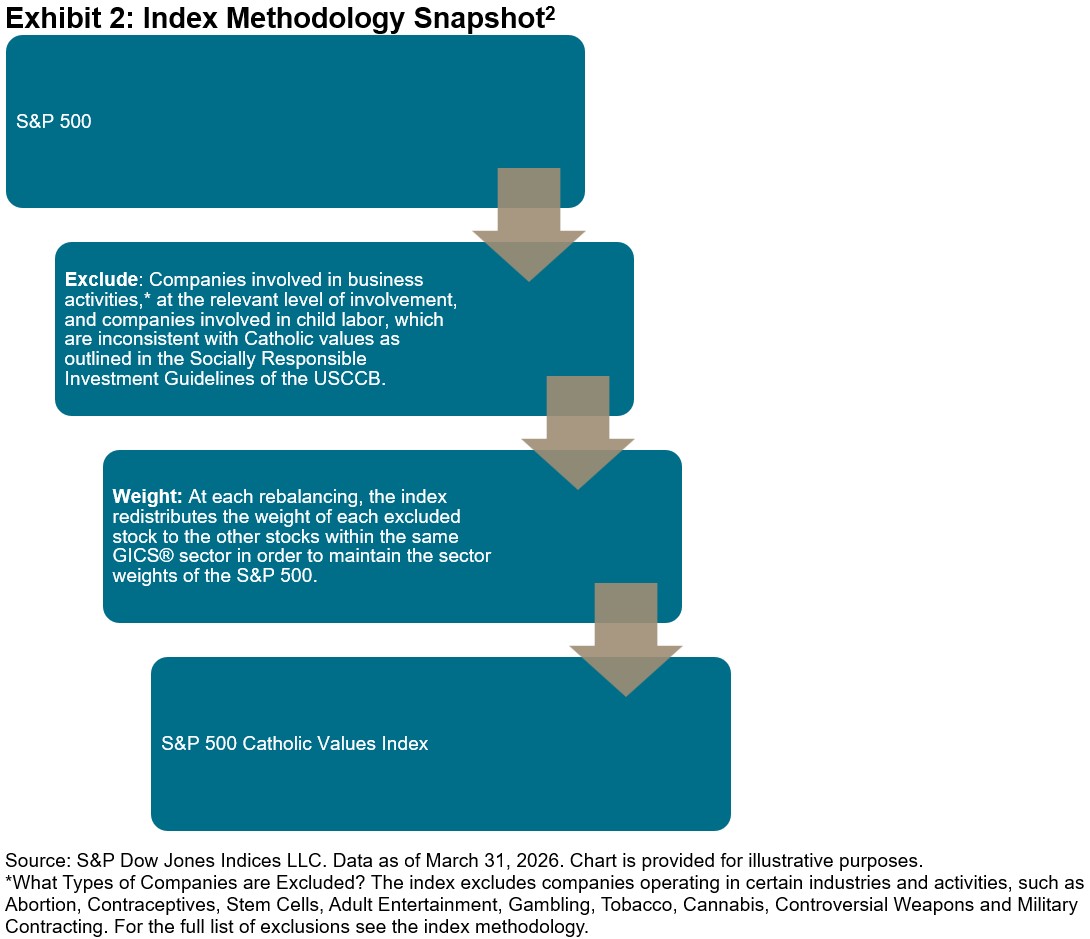

As shown in Exhibit 1, the performance of the S&P 500 Catholic Values Index has closely tracked that of its benchmark, the S&P 500, reflecting its broad market coverage. However, it is intentionally not identical, as its methodology (summarized in Exhibit 2) applies specific values-based exclusions that differentiate its composition.

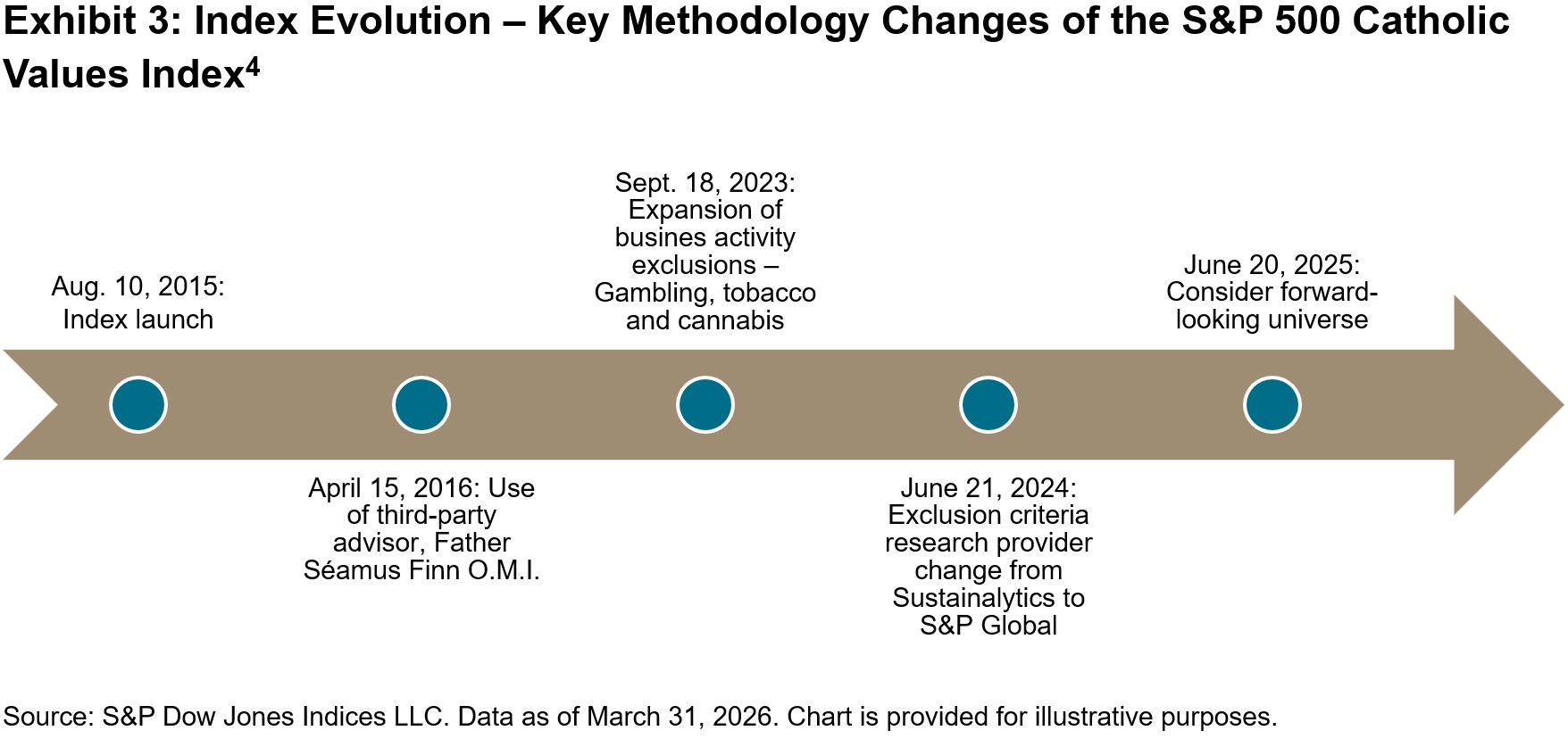

The index’s evolution reflects S&P DJI’s continuous methodology monitoring, including the 2023 expansion of exclusions for companies with business activities in gambling, tobacco and cannabis—ensuring alignment with the updated USCCB guidelines. In addition to updates in guidelines and best practices, the methodology has also evolved to leverage improved data, enabling a more efficient implementation of the USCCB guidelines, and it has been refined to minimize deviations from the S&P 500 by adjusting rebalancing schedules and incorporating a forward-looking universe.3

The 10th anniversary of the S&P 500 Catholic Values Index marks a significant milestone in the evolution of values-based indexing. Its ongoing evolution underscores the index’s capacity to balance values alignment with broad market coverage, reinforcing its relevance for those seeking to integrate faith-based principles into their investment approach.

Read on in Part 2.

1 Socially Responsible Investment Guidelines 2021

2 For the full list of exclusions, see the index methodology.

3 S&P Catholic Values Indices Rebalancing Methodology Update.

4 For the full list of changes, see the index methodology.

The posts on this blog are opinions, not advice. Please read our Disclaimers.