Capital markets offer several primary sources of income to investors, including money market interest, bond coupons and stock dividends. Alternative sources of income abound and, most recently, innovation within the exchange-traded fund (ETF) industry has introduced options-based income strategies to a wider range of market participants.

In the U.S., investors both large and small have long used options markets to generate income, either by trading options directly or indirectly through structured products.1 In more recent years, options-based ETFs have also found popularity, as a range of strategies collectively known as “covered call” (or “buy-write”) strategies are increasingly used to generate income, dampen volatility and enhance risk-adjusted performance in certain market regimes. So, how do they work, and what is their role in generating income?

What Does a Covered Call Really Do?

A covered call strategy combines:

- An investment in an asset (e.g., a portfolio tracking the S&P 500®); and

- The sale (writing) of a call option on the same (or correlated) asset.

By selling call options, the investor receives an upfront premium, and any amounts owed on the call option (occurring if the underlying asset rises above the strike price) are “covered” by the profits of the first investment. The regular repeat of such sales can provide a relatively steady income stream, with the natural trade-off that the investor will not simultaneously benefit fully from price gains in the asset, since all or a portion of those gains are offset by losses on the sold options.

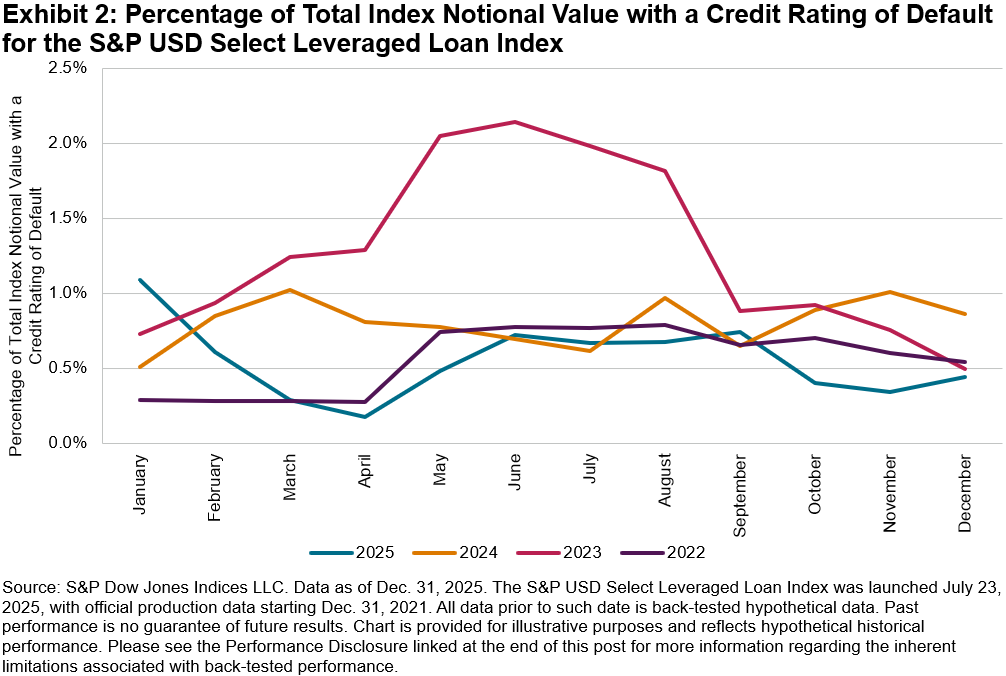

Simply put, covered call strategies exchange some upside potential for option premium income, narrowing the range of outcomes. This trade-off is illustrated through the monthly performance comparison of the S&P 500 at-the-money monthly covered call strategy—as measured by the Cboe S&P 500 BuyWrite Index (BXM)—versus the S&P 500 over a 20-year period (see Exhibit 1).2 For example, over the recent six monthly rolls between Sept. 19, 2025, and March 20, 2026, the BXM’s monthly performance ranged between -3.8% to 3.1% compared to the S&P 500’s range between -5.0% and 2.5%, with the former outperforming in five out of six months.

Why Covered Calls?

The appeal of covered calls extends beyond simple income generation and volatility reduction. Option premiums can provide a distinct income stream that is less correlated with traditional sources such as bonds and dividends. Bond income is sensitive to interest rate policy, and dividend income can be reduced during economic downturns (while dividend yields tend to be driven more by price effects).

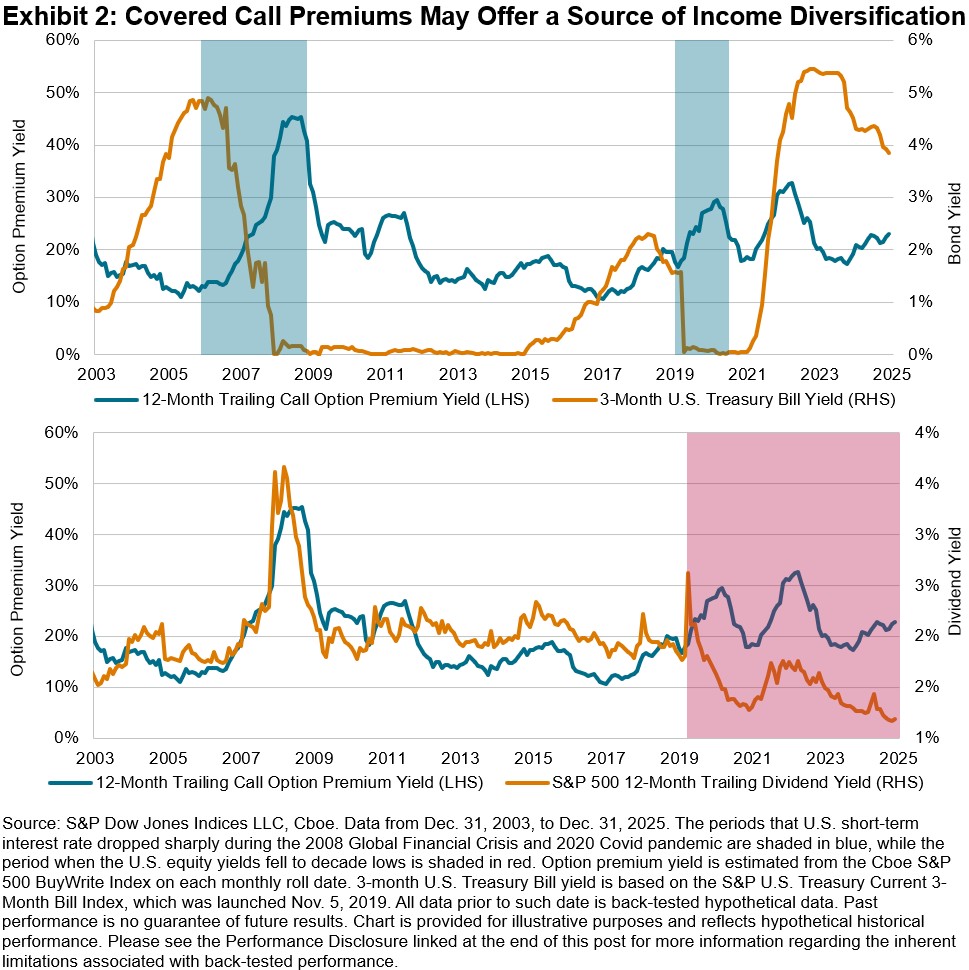

Option premiums, by contrast, are primarily driven by market volatility.3 When markets sell off, volatility typically rises, leading to higher option premiums. This was evident during the 2008 Global Financial Crisis and the 2020 COVID-19 pandemic (periods shaded in blue in Exhibit 2), when interest rates fell toward zero but increased volatility boosted option income. Notably, option premiums have also remained relatively elevated in recent years, even as dividend yields declined to decade lows (the period shaded in red in Exhibit 2).

Covered calls have historically helped support portfolio income when other sources were under pressure, making them a valuable tool for building resilient income.

Design Matters: Variations and Implementation

There are many possible variations of covered call strategies across different maturities and strike prices, and outcomes can vary materially depending on the design of the strategy. The S&P 500’s deep and robust derivatives ecosystem enables effective implementations of various strategies, catering to changing market environments and investor needs. It is important to carefully assess each component of the strategy, for both product issuers and investors, to find the optimal approach that can help achieve desired outcomes.

For a deeper dive into the index-based framework of covered call strategies, see “Defining Paths with Options-Based Index Strategies.”

1 According to SRP, the U.S. structured notes market reached USD 150 billion in 2024, up 46% from the previous year.

2 For details on the index construction, see the BXM index methodology.

3 Options market often exhibits a “volatility premium”—a tendency for implied volatility (the level of volatility reflected in option prices) to exceed the actual volatility that occurs. This phenomenon is largely driven by supply and demand imbalances in the options market (see Defining Paths with Options-Based Index Strategies for more details). Covered call strategies seek to harvest this volatility premium by regularly selling call options, aiming to profit from the persistent gap between market expectations and realized outcomes.

The posts on this blog are opinions, not advice. Please read our Disclaimers.