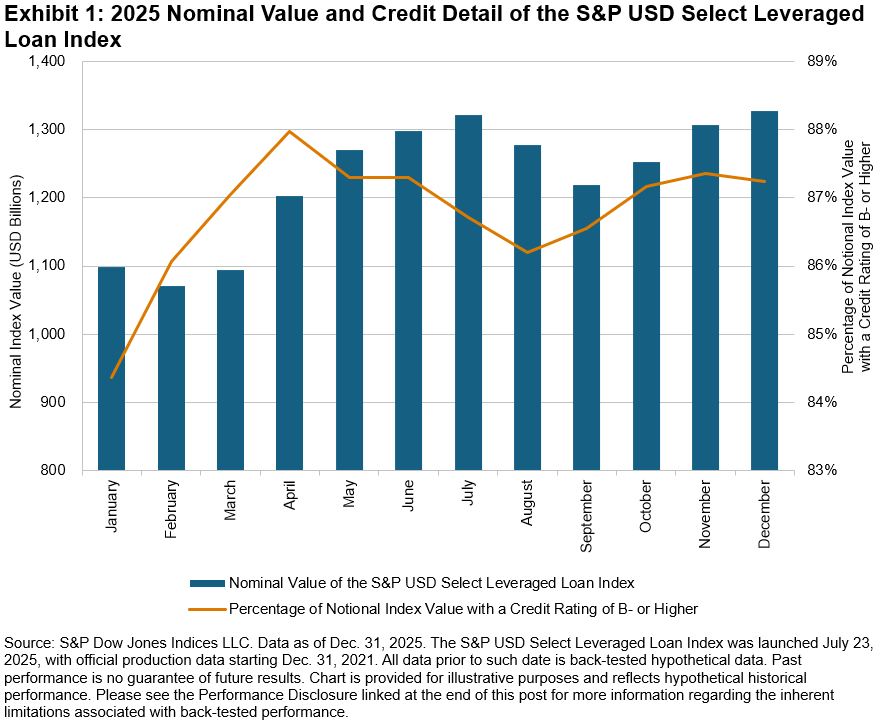

Amid growing uncertainty, small market shifts can have large impacts on companies with lower credit ratings like those found in the S&P USD Select Leveraged Loan Index. This index measures the performance of a liquid and diversified universe of USD‑denominated leveraged loans by tracking all fully funded term loans with a minimum facility size of USD 500 million and credit ratings below investment grade, providing a broader view of the leveraged loan market.

The credit quality of the larger leveraged loans in the S&P USD Select Leveraged Loan Index has improved, and the index’s total notional value is also rising, as shown in Exhibit 1. This suggests that investors are assuming less risk on the larger loans while still pursuing the higher spreads offered further down the credit ladder.

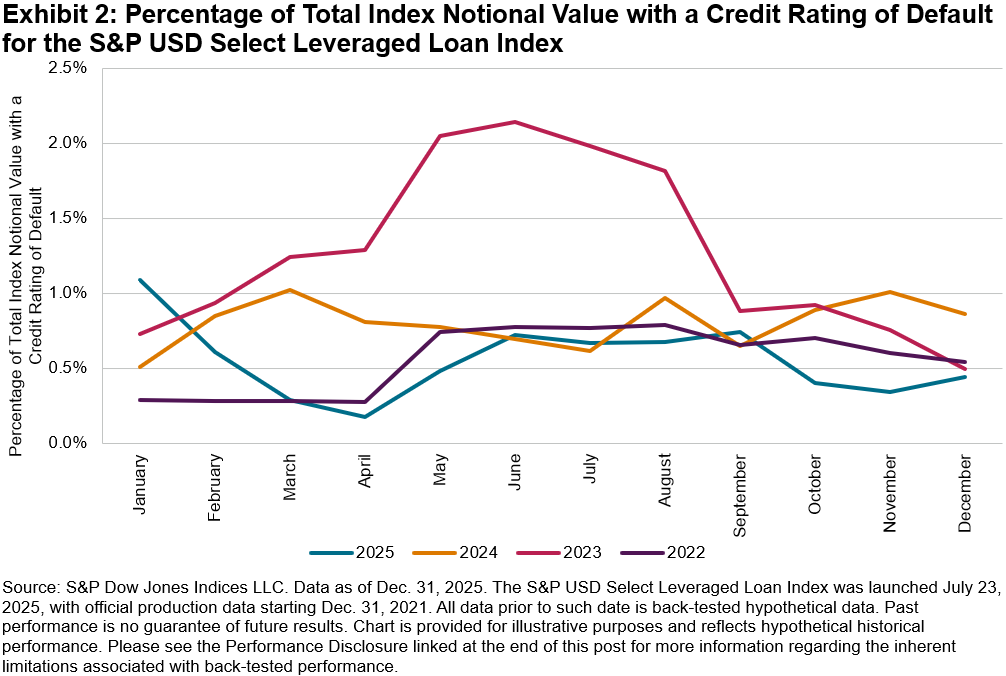

This trend is reinforced by a lower proportion of the index with a credit rating of “default” in 2025, as shown in Exhibit 2. The year‑end 2025 default percentage was below the rates recorded in each of the three preceding years.

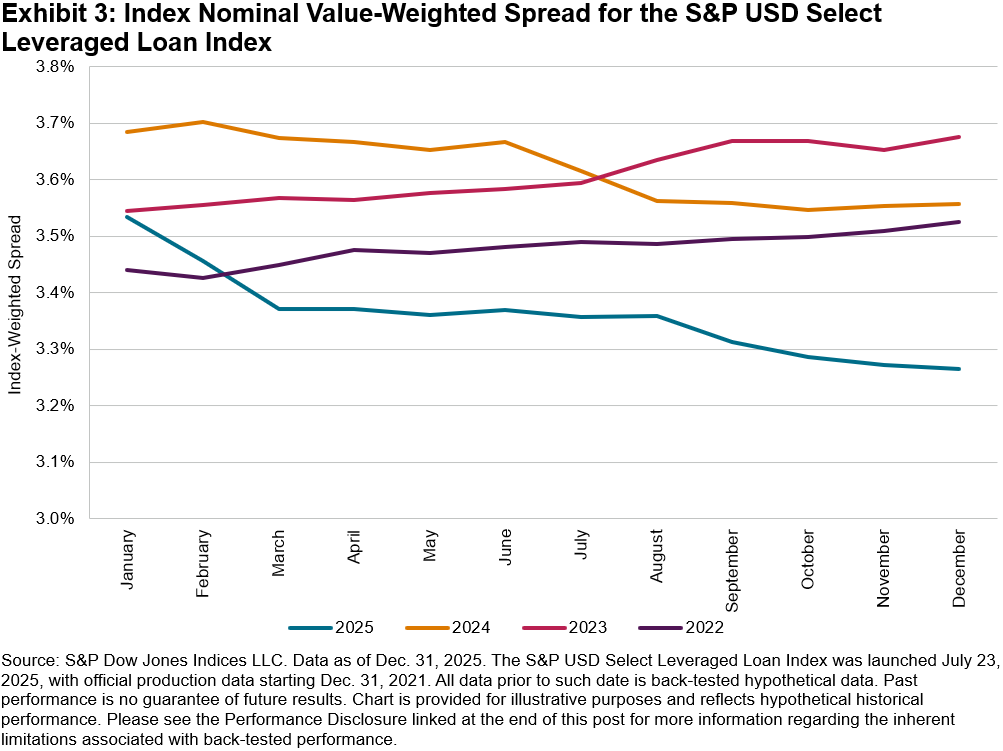

Index‑weighted spreads have been falling, reflecting improving credit quality. Spreads dropped from 3.53% to 3.27%, a 26 bps decline, and finished 2025 more than 40 bps below their 2024 peak (see Exhibit 3). As 2026 unfolds, this spread‑risk relationship could continue to be tested by market uncertainty, and the index will reveal loan market sensitivity to changing macro conditions.

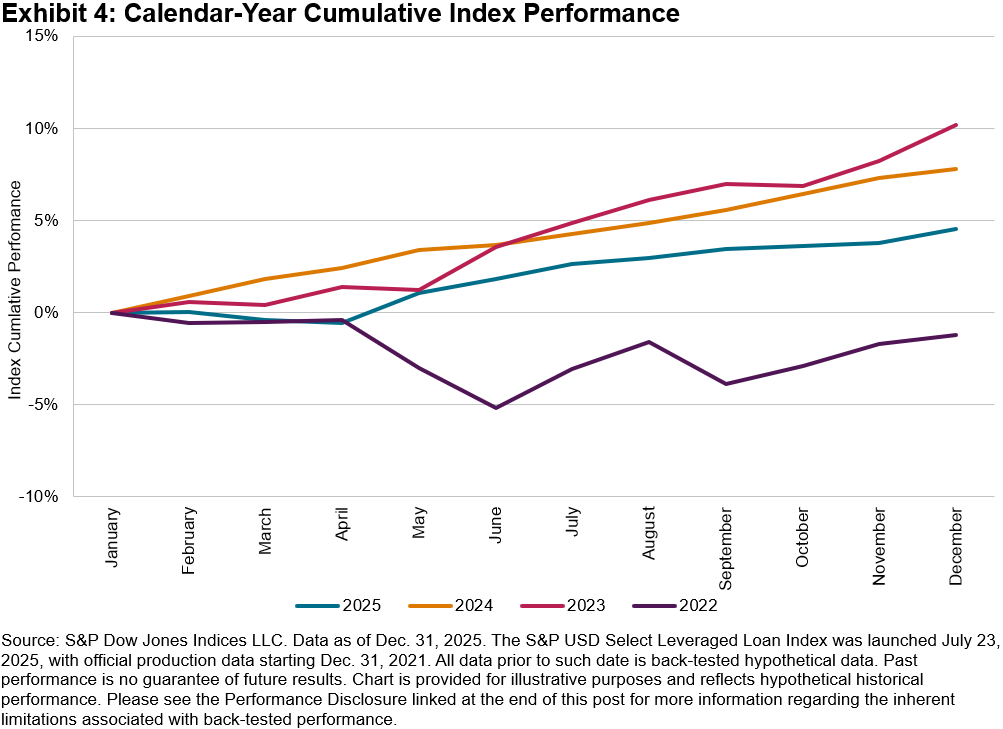

Despite falling spreads, the index increased 4.5% in 2025, driven by the growing nominal value of the index. Higher credit quality also made this performance more resilient, suggesting the market may be seeking stability amid rising uncertainty.

By focusing on the largest leveraged loans, the S&P USD Select Leveraged Loan Index measures broader market shifts and remains a valuable tool for navigating an uncertain environment through an asset class with differentiated risk.

The posts on this blog are opinions, not advice. Please read our Disclaimers.