In May 2022, the Reserve Bank of Australia (RBA) was among the last major central banks to begin raising interest rates during the post-COVID-19 monetary tightening cycle. In Q1 2026, the RBA is not taking any chances with inflation, becoming the first major central bank to implement two consecutive 25 bps rate hikes (in February and March), increasing the cash rate target from 3.6% to 4.1%, returning the rate to levels last seen in May 2025. The decision was driven by persistently above-target inflation and further reinforced by the disruptions in energy supply due to the ongoing conflict in the Middle East.

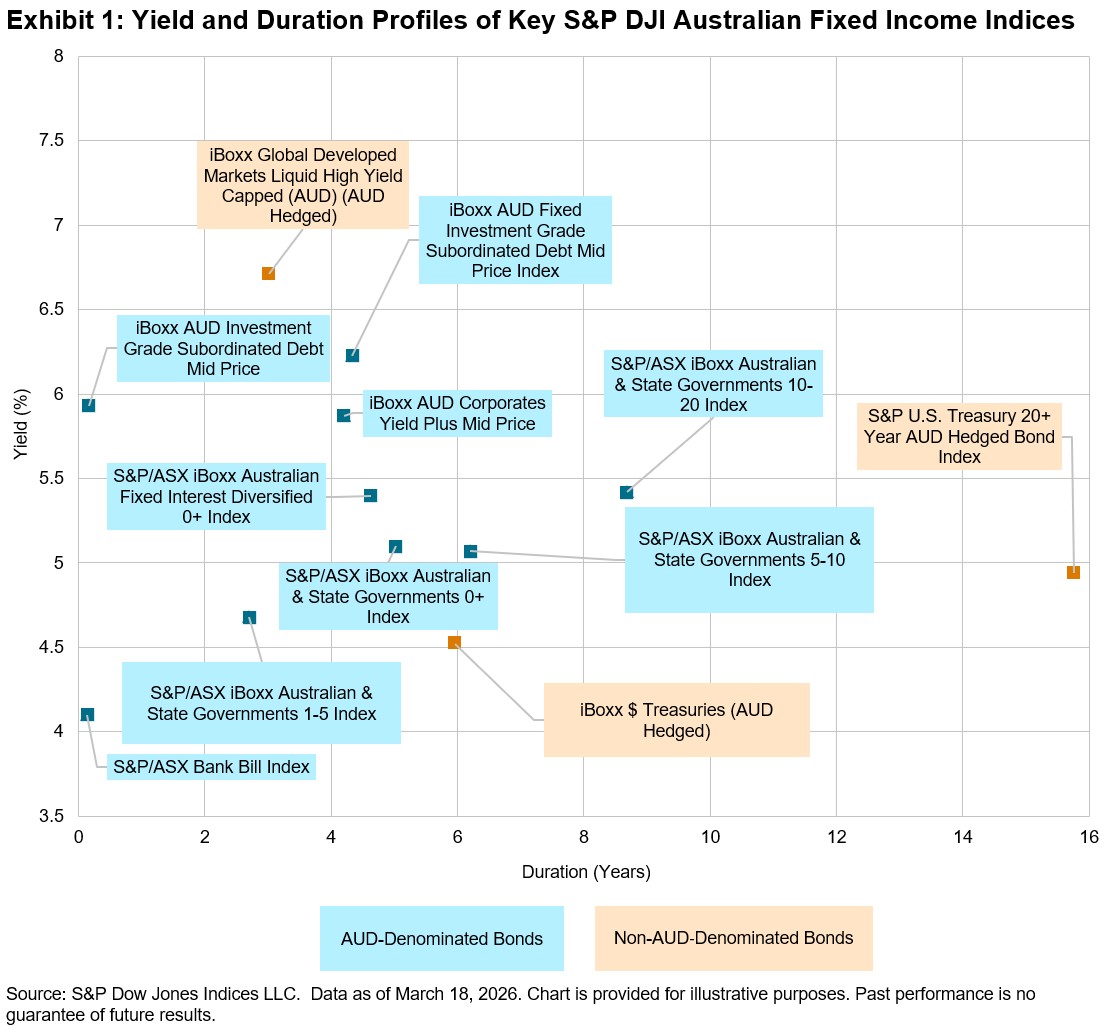

AUD Bond Yields Are above 5% Again

All of the AUD-denominated bond indices in Exhibit 1, except for the S&P/ASX iBoxx Australian & State Governments 1-5 Index, had yields above 5% as of March 18, 2026. The S&P/ASX Bank Bill Index, which generally emulates the RBA cash rate targets, had the shortest duration of 0.13 years and the lowest yield of 4.1%.

The iBoxx AUD Investment Grade Subordinated Debt Mid Price Index, which reflects floating-rate subrdinated Tier 2 instruments, had the second-shortest duration at 0.16 years and the third-highest yield at 5.93%. The ultrashort duration is due to the coupon resetting frequently (floating rate). Its fixed-rate sibling, the iBoxx AUD Fixed Investment Grade Subordinated Debt Mid Price Index, had a yield of 6.23% and duration of 4.34%. The higher yields for both subordinated debt indices were driven by the higher credit and capital-structure risk.

With the U.S. Federal Fund Rate sitting at 3.75%, the USD Treasury indices had lower yields, between 4.5% and 5%. Even with a significantly longer duration of 15.75 years, the S&P U.S. Treasury 20+ Year AUD Hedged Bond Index yield remained below 5%, providing less than 50 bps in spread for the additional duration risk.

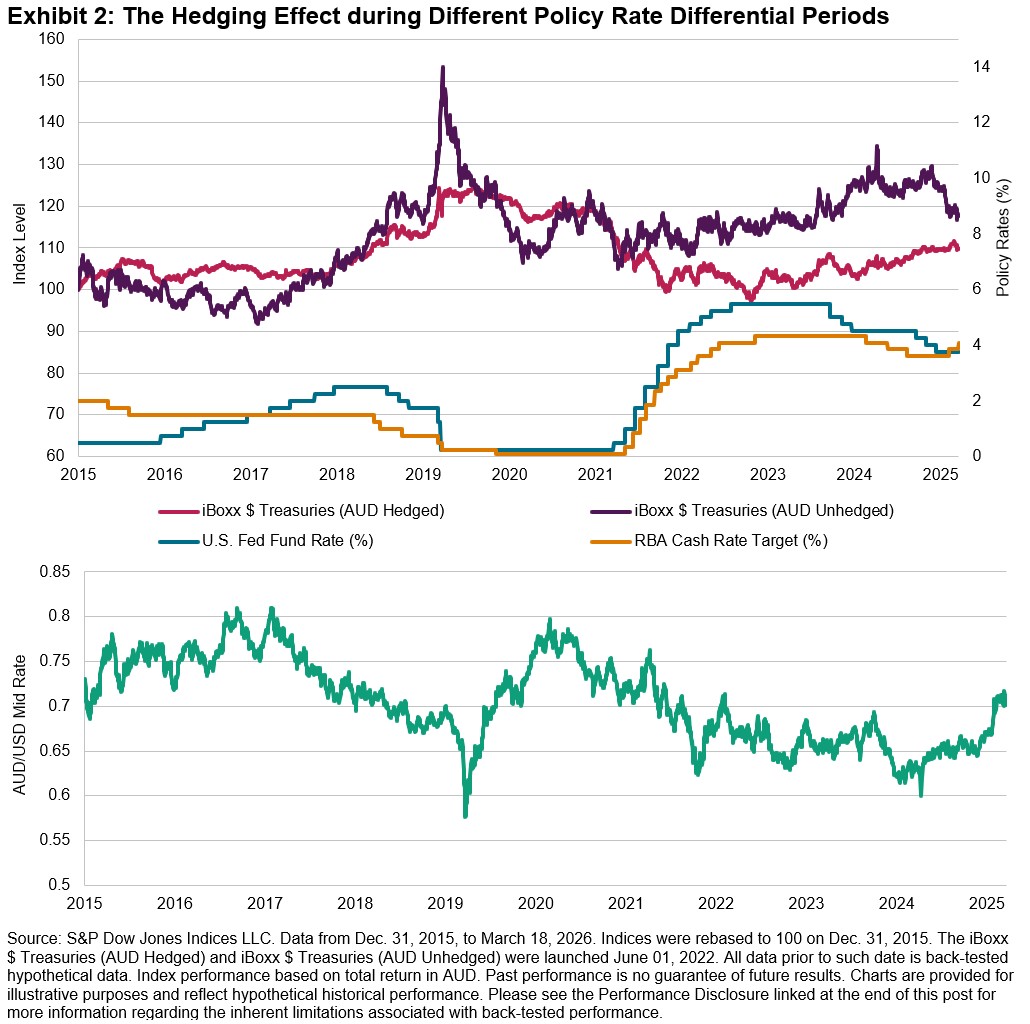

Hedging Is Increasingly Important

With the RBA cash rate at 4.1%—above the U.S. Fed Funds rate for the first time since 2017—AUD-based investors should note that this shift can impact both AUD/USD trends and FX hedging costs. Historically, the iBoxx $ Treasuries (AUD Hedged) outperformed its unhedged counterpart when AUD appreciated between 2015-2017, but unhedged returns became more volatile as AUD/USD fluctuated. Recently, as AUD strengthened since late 2025, the performance gap between hedged and unhedged indices narrowed. With higher Australian rates and rising commodity prices, the Australian dollar may continue to appreciate, making currency hedging for non-AUD exposures more crucial but also potentially more costly, meaning there may be both benefits and costs for hedging in this environment.

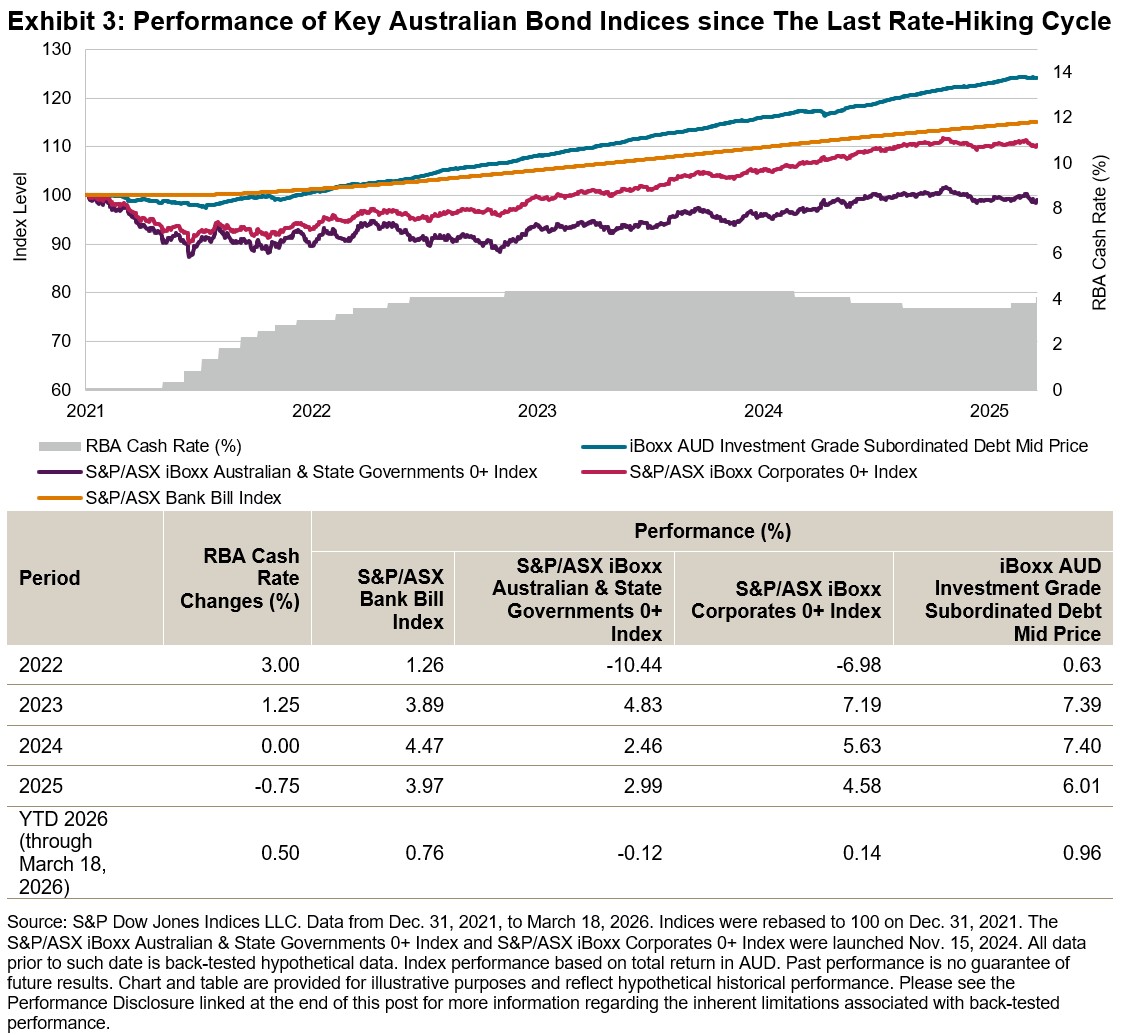

Returns since the Previous Rate Hiking Cycle

Between May 2022 and late 2023, the RBA raised the cash rate target from 0.1% to 4.35%. Over the past five years, the S&P/ASX Bank Bill Index mirrored the changes in the cash rate, delivering steady positive performance in line with policy rates (see Exhibit 3).

The S&P/ASX iBoxx Australian & State Governments 0+ Index and S&P/ASX iBoxx Corporates 0+ Index underperformed the S&P/ASX Bank Bill Index due to their longer duration and greater sensitivity to rising rates. However, higher yield (carry) from corporate bonds allowed the S&P/ASX iBoxx Corporates 0+ Index to outperform the S&P/ASX iBoxx Australian & State Governments 0+ Index every year reflected in Exhibit 3.

Frequent coupon resets from the floating rate structure of the iBoxx AUD Investment Grade Subordinated Debt Mid Price Index constituents helped limit interest rate risk and volatility, while higher yields from additional credit and capital structure spreads boosted performance—delivering a total return of 24.22% since Dec. 31, 2021.

As the RBA embarks on yet another monetary policy tightening cycle to combat inflation, understanding how these indices performed previously can provide valuable insights for navigating this current environment.