Enthusiasm over artificial intelligence (AI) has been one of the driving market forces in recent years, with investors’ expectations that certain companies stand to reap particular rewards from the application of AI propelling their valuations.

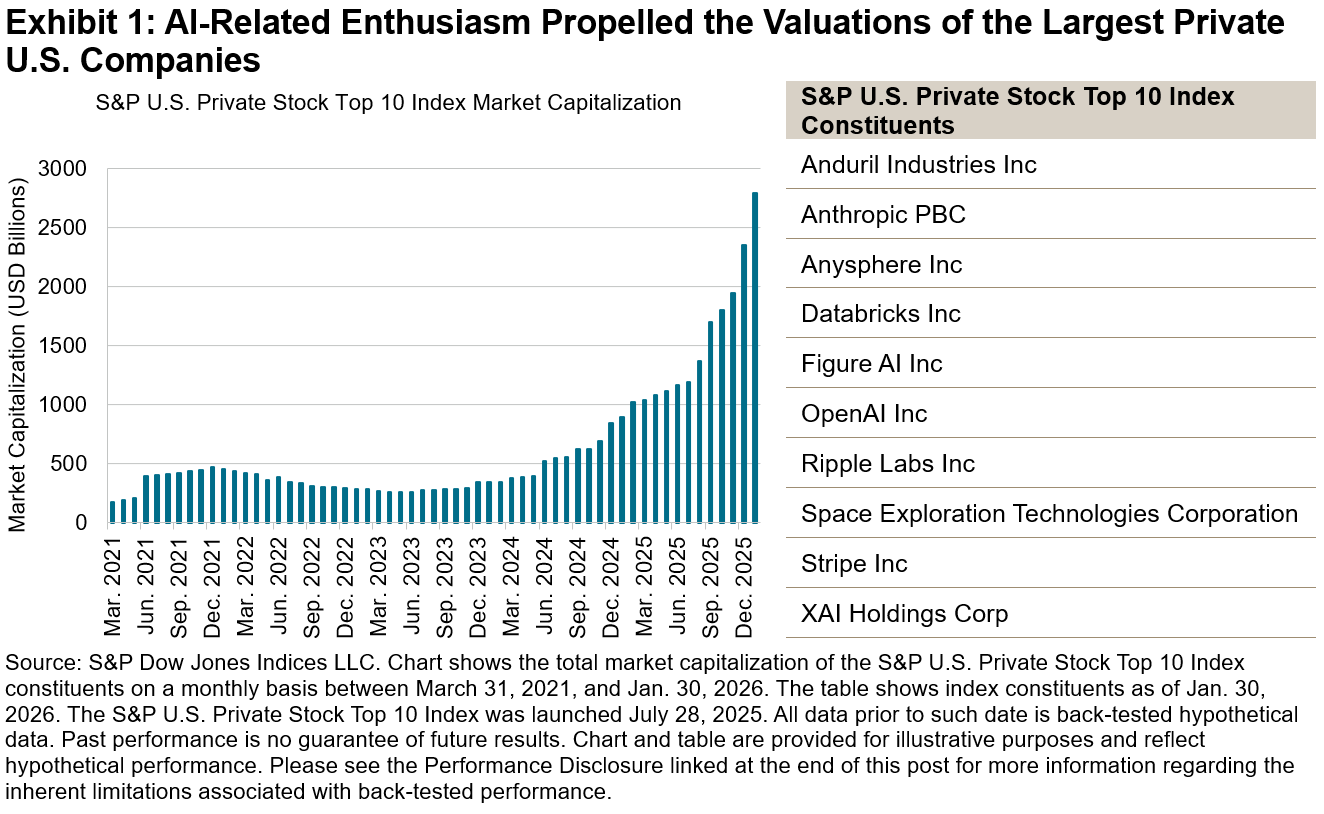

This dynamic contributed to narrowing leadership among public equity market barometers and, coupled with a growing penchant for companies looking beyond Earth’s limits, helped to explain a 1,500% increase in the collective valuations of the 10 largest venture-backed U.S. companies since March 2021 (see Exhibit 1).

The anticipated initial public offerings (IPOs) later this year from some of these companies—including SpaceX, OpenAI, Anthropic and Databricks—have been met with much enthusiasm. Many market participants have started to wonder when such companies could be eligible for addition to various U.S. equity indices, especially the S&P 500® given it is widely viewed as the preeminent U.S. equity gauge.

Collectively, recent valuations of the 10 largest venture-backed U.S. companies would imply (assuming a full IPO of all stock) that they would make up around 4.5% of the S&P 500 if they joined—more than the weight of the Energy sector, but less than that of Microsoft.

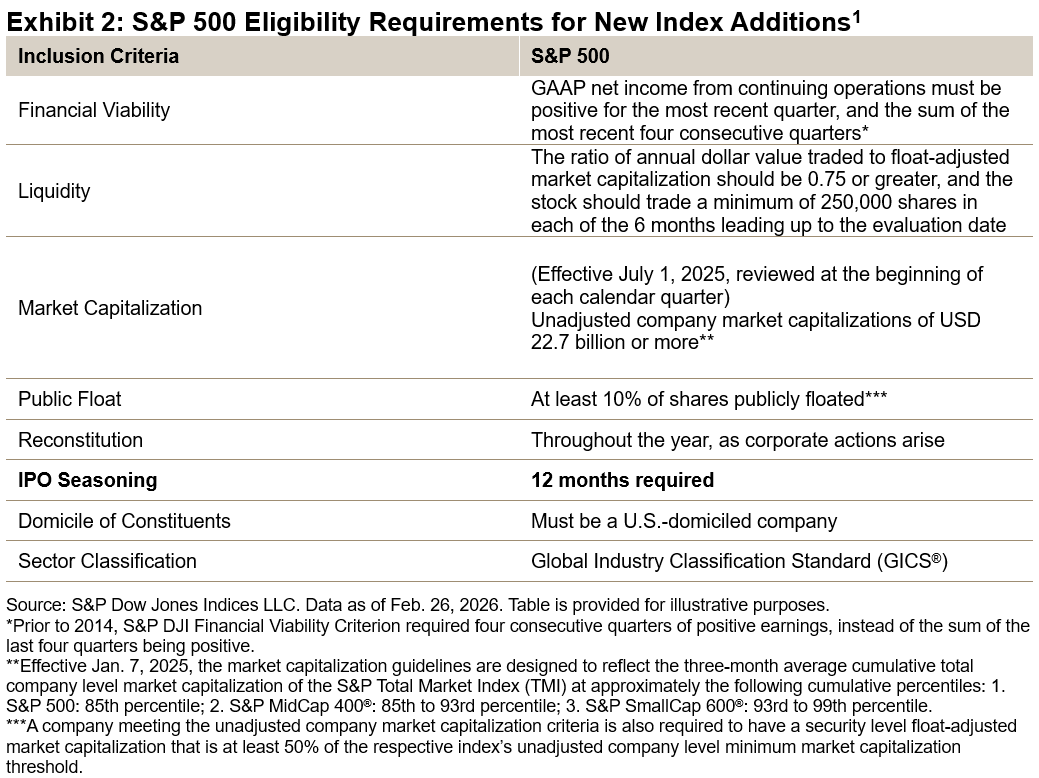

Exhibit 2 outlines the addition criteria that companies must meet to be considered eligible for The 500®. IPOs need to be traded on an eligible exchange for at least 12 months, and index additions must meet size requirements, financial viability and liquidity thresholds, among other criteria. Importantly, index addition is not guaranteed simply by meeting all the eligibility criteria; the index committee is also mindful of other factors such as index turnover and sector balance when considering constituent changes.

The holistic approach to identifying eligible S&P 500 companies can help to distinguish between companies whose elevated valuations may be short lived versus those that are more reflective of the large-cap U.S. equity segment.

The IPO seasoning period is useful in this endeavor given that various eligibility criteria are measured over 12-month periods, but IPO seasoning can also support index replicability. It is common for some investors to be prevented from selling shares for a predetermined time after an IPO; these lockup periods could pose challenges to index trackers that are looking to purchase enough company shares to replicate index weights.

Even if the expected IPOs may not be immediately included under the current methodology, their anticipated scale has motivated market participants to question whether changing the methodology would better support the S&P 500’s objective of representing the large-cap U.S. equity segment. Proponents of IPO fast track eligibility may point to the fact that free float-adjusting index weights, as in the S&P 500, could mitigate replicability concerns, but there are valid arguments in both directions.

Importantly, index methodologies do evolve to ensure that indices continue to represent the market segments they measure, and to ensure indices remain investable and replicable. Indeed, an important role of the index committee is to remain abreast of prevailing market dynamics and longer-term changes to market structure, and where appropriate seek feedback from market participants. Significant methodology changes tend to incorporate public consultations, providing market participants with the opportunity to share their feedback and perspectives on the results.2

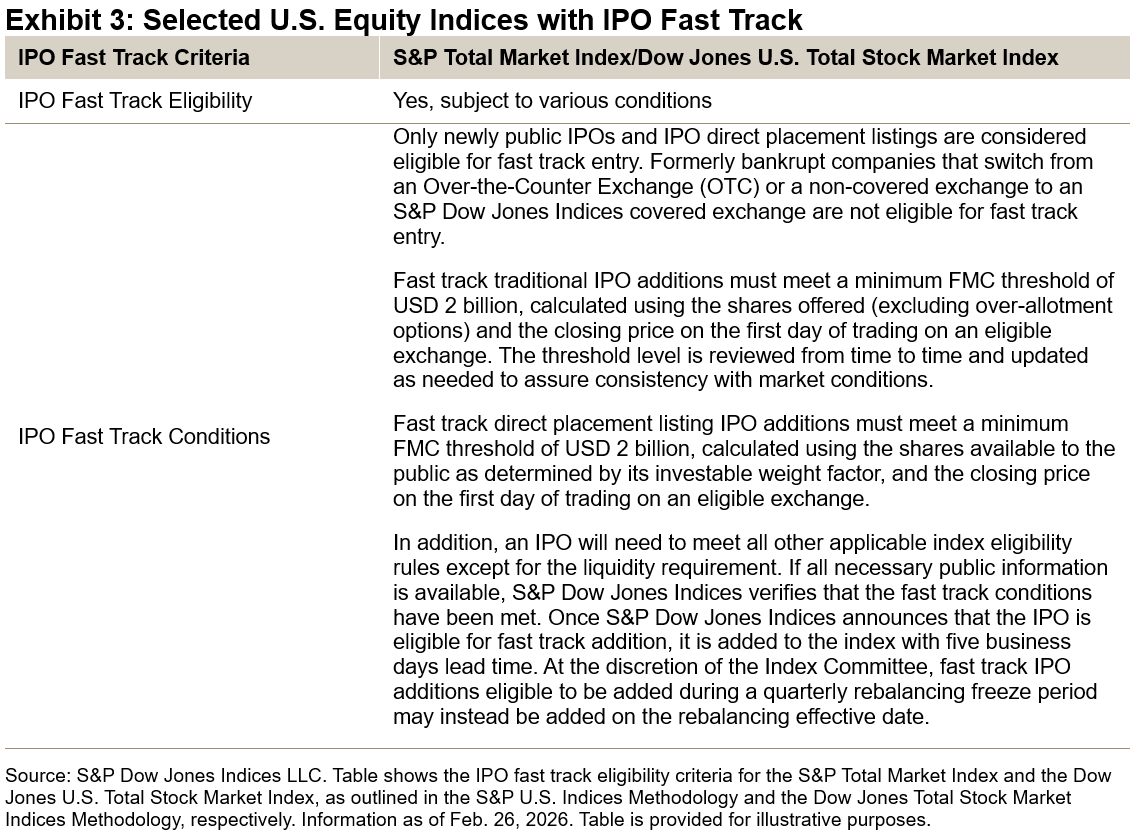

In the meantime, S&P Dow Jones Indices maintains other U.S. equity indices that allow fast track IPO eligibility. For example, the S&P Total Market Index and the Dow Jones U.S. Total Stock Market Index require IPO fast track candidates to meet various rules (see Exhibit 3). Unless exceptions are made, candidates must also meet the underlying index eligibility rules, such as requiring at least 10% of a company’s market capitalization to be available to trade.

As a result, the recent focus on IPO eligibility for various indices provides us with an opportunity to examine the potential treatment. The S&P 500’s 12-month IPO seasoning period aligns with holistic assessments of the large-cap U.S. equity segment, while other S&P DJI U.S. equity indices allow for the possibility of fast track IPO entry. While more details may emerge on anticipated IPOs, readers may rely on our public methodologies and processes to stay informed of their future index treatment.

1 For more information see the S&P U.S. Indices Methodology.

2 A current list of open consultations and related announcements is maintained here.

The posts on this blog are opinions, not advice. Please read our Disclaimers.