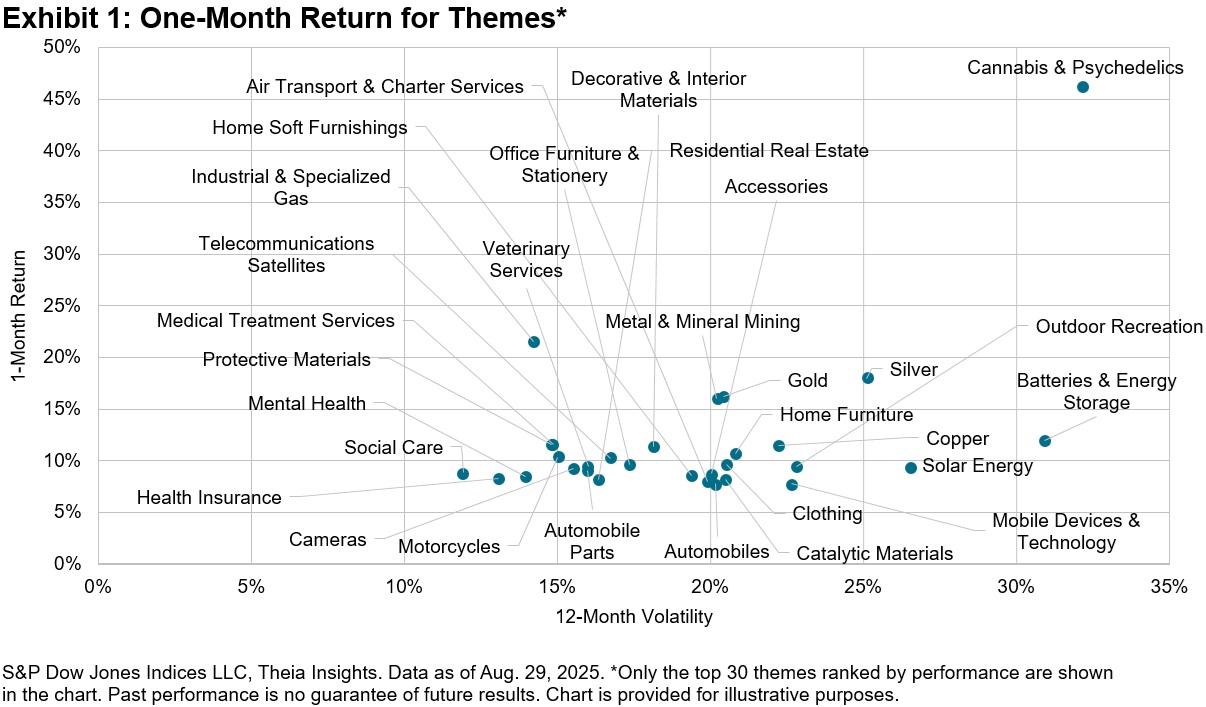

August’s S&P Thematics Dashboard captures a market in motion—from precious metals rallying to multi-year highs to energy and technology themes. With the ongoing macro-political uncertainty in the backdrop, Silver (up 18%) reached a 14-year high, with Gold up 16% on dovish Fed expectations and a weaker U.S. dollar.1 This momentum extended across the metals complex, with Metal & Mineral Mining up 16% and Copper gaining 12% on infrastructure spending prospects and supply-demand tightness.2

Alternative Medicine Takes the Stage

The standout performer of the month was Cannabis & Psychedelics, which soared 46%. Renewed investor enthusiasm was driven by shifting regulatory debates in Europe and the U.S.3 alongside new developments in the cannabis beverage market.4 Clinical confidence is also rising: mid-stage trials report that psychedelics might reduce anxiety symptoms—sometimes with effects lasting up to three months—highlighting renewed interest in psychedelic-assisted therapy’s potential.5 Strength also extended across the broader healthcare space, with Medical Treatment Services, Mental Health and Health Insurance up 12%, 8.5% and 8%, respectively.

Energy Transition Shows Mixed Signals

Large-cap energy was among the top sector performers in the second quarter, with Batteries & Energy Storage climbing 12% on strong electric vehicle adoption, recycling breakthroughs and infrastructure buildout.6 Solar Energy gained 9%, while traditional power sources like Coal (up 6%) and Nuclear (up 4%) reminded investors of their persistence.

By contrast, Wind Energy declined 4% after federal funding cuts and policy reversals nearly completed halted offshore projects.7 The contrasting outcomes highlight how policy decisions and infrastructure investment trends are shaping winners and laggards within the energy transition.

Digital Assets and Regulatory Momentum

The digital asset space showed modest gains in August, with Cryptocurrency & Digital Assets up 3% and Blockchain & Distributed Ledger down -2%. Investor sentiment was positively shaped by regulatory debates, particularly around U.S. policy efforts to establish clearer rules for stablecoins and crypto market oversight. This shift in tone provided a constructive backdrop for the sector, even as price action remained relatively muted. By month’s end, the broader crypto market reached roughly USD 4 trillion in value, supported by growing optimism that regulatory clarity could open the door to greater institutional participation.8

Technology and Defense Overview

Technology themes lagged. Artificial Intelligence (-2%), Digital Transformation (-2%) and Cybersecurity (up 0.1%) all underperformed. Structural progress in AI and robotics continues: OpenAI launched ChatGPT Agent,9 Amazon reached one million robots with its DeepFleet logistic system10 and AWS debuted a marketplace for autonomous AI agents.11

Meanwhile, defense tech gained visibility as the U.S. Army signed a USD 10 billion enterprise AI contract with Palantir, highlighting the growing role of commercial AI in national security.12 European defense was down, with the S&P Europe Defense Vision Index falling 3%, while the S&P Kensho Global Future Defense Index was up 9%, driven largely by U.S. names.

Themes on the Radar: Powering the AI Era

AI-driven data center growth is supporting a renaissance of the U.S. grid dynamics. Electricity demand from AI data centers is projected to surge nearly thirtyfold by 2035, potentially accounting for 70% of all data center electricity consumption,14 and 13% of total U.S electricity demand.[14] In response to this rise, companies are also exploring the expansion of nuclear capacity, including Constellation Energy’s multibillion-dollar commitment to restart key facilities and expand generation capacity.15

These developments are translating into tangible market growth: the Data Center theme was up approximately 39% YTD, while energy infrastructure-linked names—reflected in the S&P U.S. Power Infrastructure Select Index—have climbed approximately 17% YTD.

Conclusion

August’s results highlighted the evolving market across multiple megatrends—from Healthcare & Wellness to Innovative Technology. Many market participants are balancing traditionally defensive positions such as precious metals with growth-driven exposures in areas like alternative medicine, energy transition and AI infrastructure. Track these developments and more in our monthly dashboard updates.

1 Gold Hits Record High on US Rate-Cut Bets, Growing Debt Concerns – Bloomberg

2 Base Metals ETFs Rally as Industrial Demand Surges—Here’s How You Can Benefit – Appreciate

3 Psychedelics regain momentum in 2025 on political tailwinds, clinical wins

4 The buzz around THC drinks is going flat – Business Insider

5 LSD shows promise for reducing anxiety in drugmaker’s midstage study – AP News

7 Trump administration cancels $679 million for offshore wind projects at ports – NPR

8 Crypto sector breaches $4 trillion in market value during pivotal week – Reuters

9 OpenAI’s new ChatGPT Agent can control an entire computer and do tasks for you – The Verge

10 Amazon DeepFleet AI Model for Robotics – Digital Commerce 360

11 The Next Big Theme: August 2025 – Global X

12 US Army pools contracts into up to $10 billion Palantir deal – Reuters

13 Deloitte Report: AI Data Center Power Demand to Surge 30x by 2035 – T&D World

The posts on this blog are opinions, not advice. Please read our Disclaimers.