Index providers do far more than supply the benchmarks that index-based products aim to track. They also offer a range of services that wealth managers may look to in an effort to sharpen their strategies, streamline operations and deepen advisor engagement. Yet, some firms still treat index providers solely as data vendors—underutilizing a broader toolkit available to wealth and asset managers as they seek to gain a competitive edge.

According to new research from Cerulli Associates, most wealth manager home-office executives view index providers primarily as inputs for performance measurement and benchmarking.1 But a select group—particularly those developing customized solutions, proprietary products or building model portfolios—are beginning to unlock the true potential of what index providers can offer. These firms are turning to index providers not just for data but for collaboration, and in doing so, they’re discovering new ways to differentiate and scale.

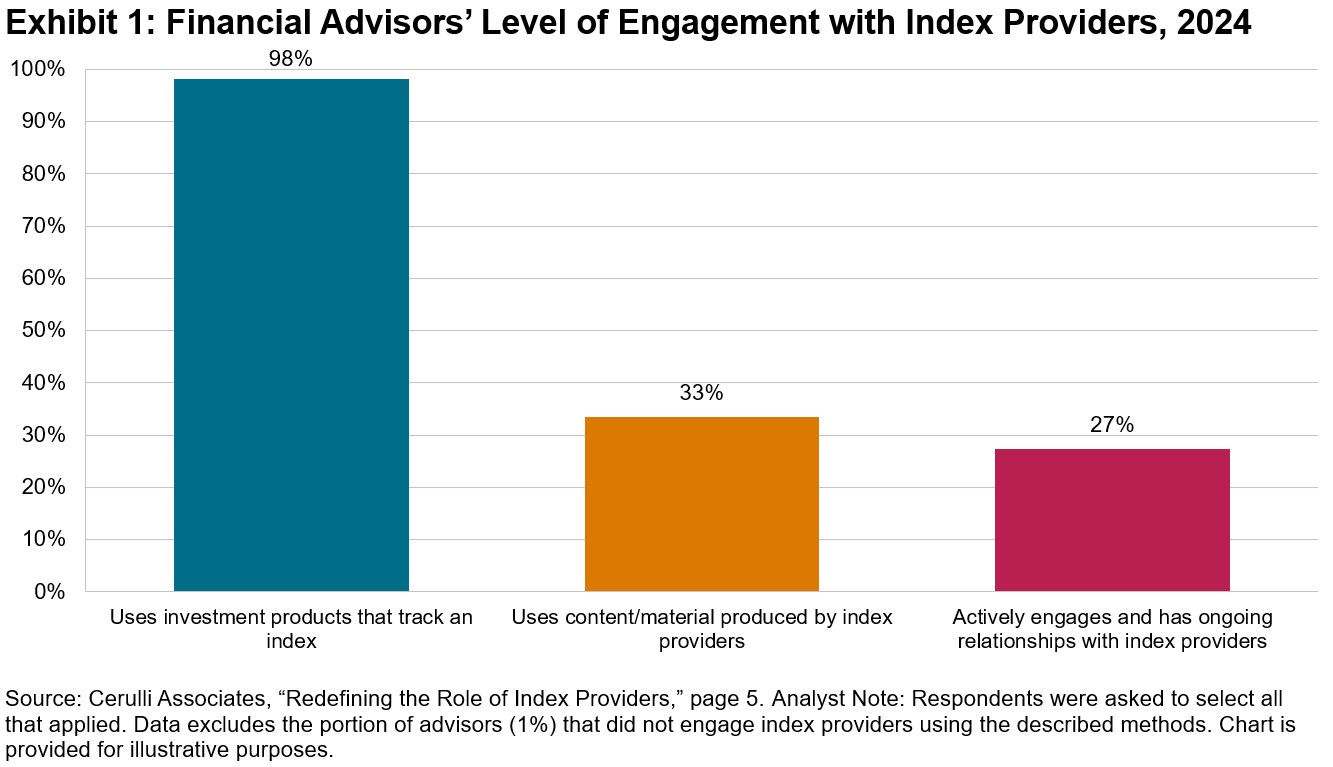

Financial Advisors’ Level of Engagement with Index Providers

A recent blog examined the forces contributing to the rise of indexing in wealth management. While the vast majority of financial advisors use index-based investment products, most aren’t engaging with index providers in other ways (see Exhibit 1).

This invites the question: what other opportunities might be available for wealth managers that seek to leverage index providers’ offerings? Index providers provide various solutions, such as data and thought leadership. Forming a strategic relationship with an index provider that taps into these capabilities can help build a foundation for developing products and solutions that advisors can incorporate into client portfolios in support of their practices.

From Index Construction to Product Development Support

The Cerulli Associates paper explores how index providers can support the product development lifecycle. That includes helping firms choose the right index exposure, offering transparency on index methodology, and advising on how index data is delivered and integrated into internal systems.

For advisory firms looking to stand out in a crowded and highly competitive field, brand alignment also matters. When launching new index-based products, licensing a brand from a known provider may lend recognition to such products, especially for firms that don’t yet have household-name status with advisors or end investors.

Furthermore, index providers can help clients customize existing indices or commission a white-label index using their own intellectual property.

Resources for Education, Distribution and Advisor Engagement

Beyond the mechanics of benchmark construction, index providers are also sources of educational content and thought leadership—another potentially underleveraged tool, especially for wealth managers.

Firms can tap into these resources to inform advisors, support distribution, and supplement product narratives with index-related information. For example, index providers can contribute to educational campaigns that explain the methodology behind a new index objective, share market context, or offer historical performance data. Providers may also support advisor meetings or webinars, giving wealth managers a way to deliver expert insights on indices directly to the field.

As wealth management incorporates outsourced portfolio construction and more scalable solutions, firms that make the most of the full range of services that index providers offer may find themselves better equipped to meet advisor needs and investor expectations. Read the full report by Cerulli Associates to learn about other ways asset and wealth managers can optimize their engagement with index providers.

1 The Cerulli Associates whitepaper “Redefining the Role of Index Providers” was sponsored by S&P Dow Jones Indices.

The posts on this blog are opinions, not advice. Please read our Disclaimers.