In an environment of rapidly evolving trade conditions, understanding the nuances of index performance across countries is essential. As trade policies fluctuate and central banks carefully evaluate the economic outlook, the repercussions for markets and global commerce may be significant.

Reflecting on the past couple of years, it is noteworthy that the 12-month total return differential between the S&P United States LargeMidCap and the S&P World ex-U.S. Index turned negative in March 2025 for the first time since October 2023, marking a notable shift from the 20% difference in 2024, a period characterized by strong performance for U.S. equities. This recent change not only highlights the evolving landscape of global indices but also emphasizes the importance of closely monitoring international market trends, as they can have substantial implications for growth trajectories.

The wavering of U.S. stocks is no less apparent when compared to a titan on the other side of the globe. In both 2024 and YTD 2025, the S&P China BMI outperformed the S&P Emerging Ex-China BMI by a wide margin, a significant reversal from 2023 when it underperformed by 33%.

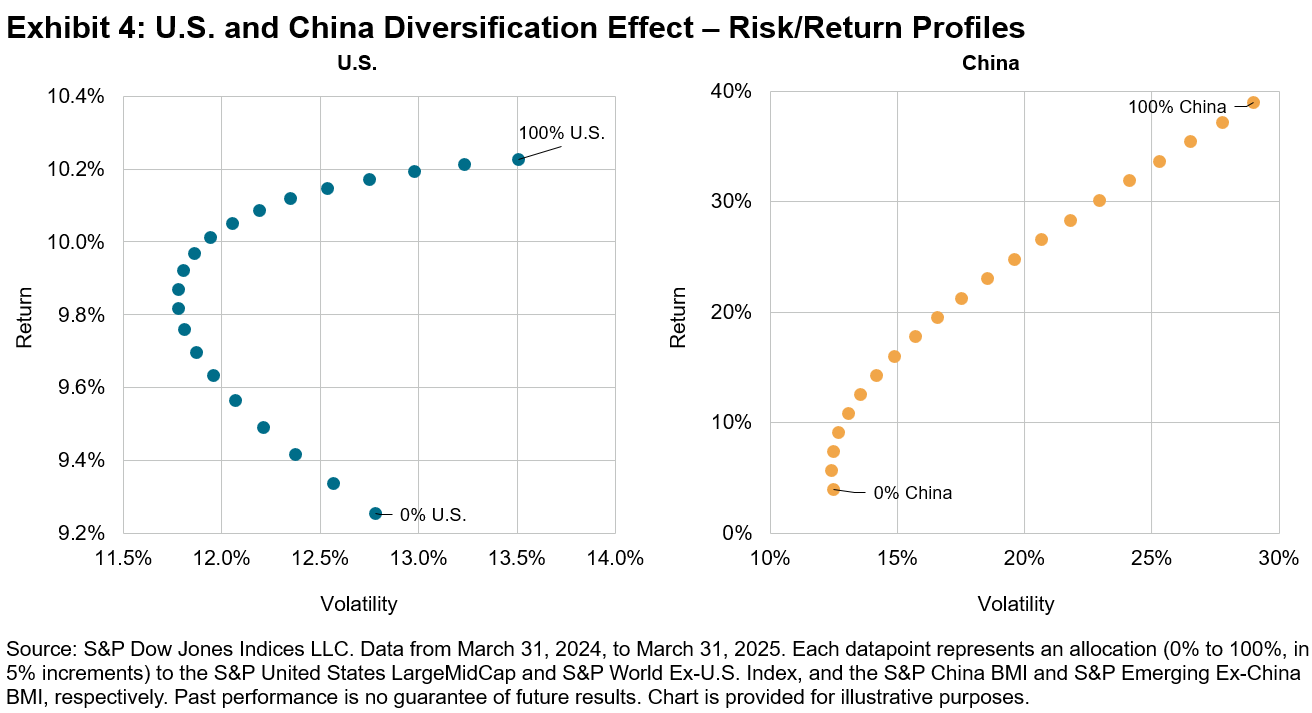

Shifting our focus from performance to risk, we see a continuation of diversification benefits witnessed in the past for both U.S. and Chinese equities. In Exhibit 3, we calculate the trailing 12-month volatility differential between the S&P World Index and S&P World Ex-U.S. Index, and the S&P Emerging BMI and S&P Emerging Ex-China BMI, respectively. When the spread was positive, the inclusion of a country increased the volatility in the benchmark. When the spread was negative, the country acted as a volatility diversifier. Notably, both the U.S. and China have continued to be volatility diversifiers in 2025 (see Exhibit 3).1

As we consider these diversification characteristics, it’s important to recognize that the current shift in trade protectionism may signal a change in market dynamics for U.S. equities. By leveraging a comprehensive toolkit, different combinations of equity indices, such as hypothetically blending the S&P United States LargeMidCap with the S&P World Ex-U.S. Index and S&P China BMI with the S&P Emerging Ex-China BMI, could produce a different risk/return profile. Exhibit 4 displays the risk/return tradeoff of these combinations over the last year.

In summary, thoughtful approaches could be increasingly important for global investors seeking to harness opportunities and mitigate risks in today’s complex landscape. By better understanding the potential benefits of country diversification, market participants can make more informed decisions as they seek to navigate these dynamics.

The author would like to thank Benedek Vörös for his contributions to this post.

1 We recognize that the U.S. represents more than 70% of the S&P World Index. Nonetheless, it’s essential to highlight that this U.S. segment is made up of large multinational corporations whose revenue sources extend across multiple regions.

The posts on this blog are opinions, not advice. Please read our Disclaimers.