In the first part of this blog series, we introduced the S&P 500® Top 20 Select Indices, including their construction and relevance to the equity market. Now, let’s delve deeper into the indices’ historical performance and relative performance to other similar indices.

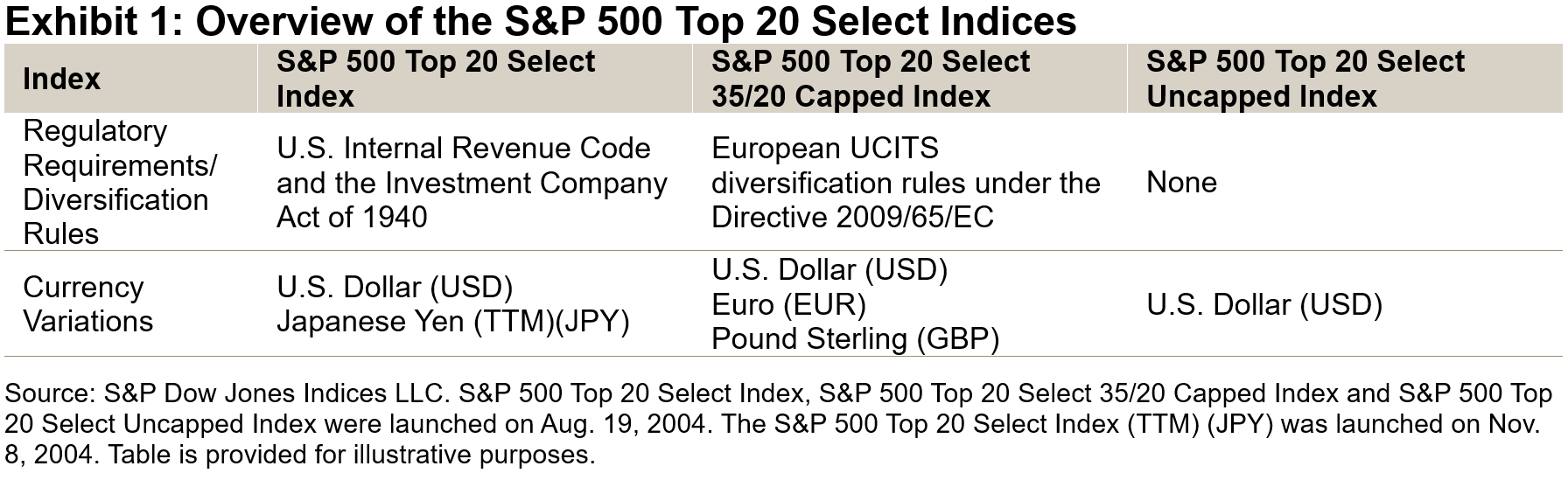

Perhaps unsurprisingly, the S&P 500 Top 20 Select Indices all had similar cumulative returns, as only a handful of mega-cap stocks would have exceeded the capping thresholds historically. Although these indices trailed the S&P 500 for a period after the 2008 Global Financial Crisis, their outperformance after the COVID-19 pandemic reflected the overweighting in the Information Technology sector (see Exhibit 1).

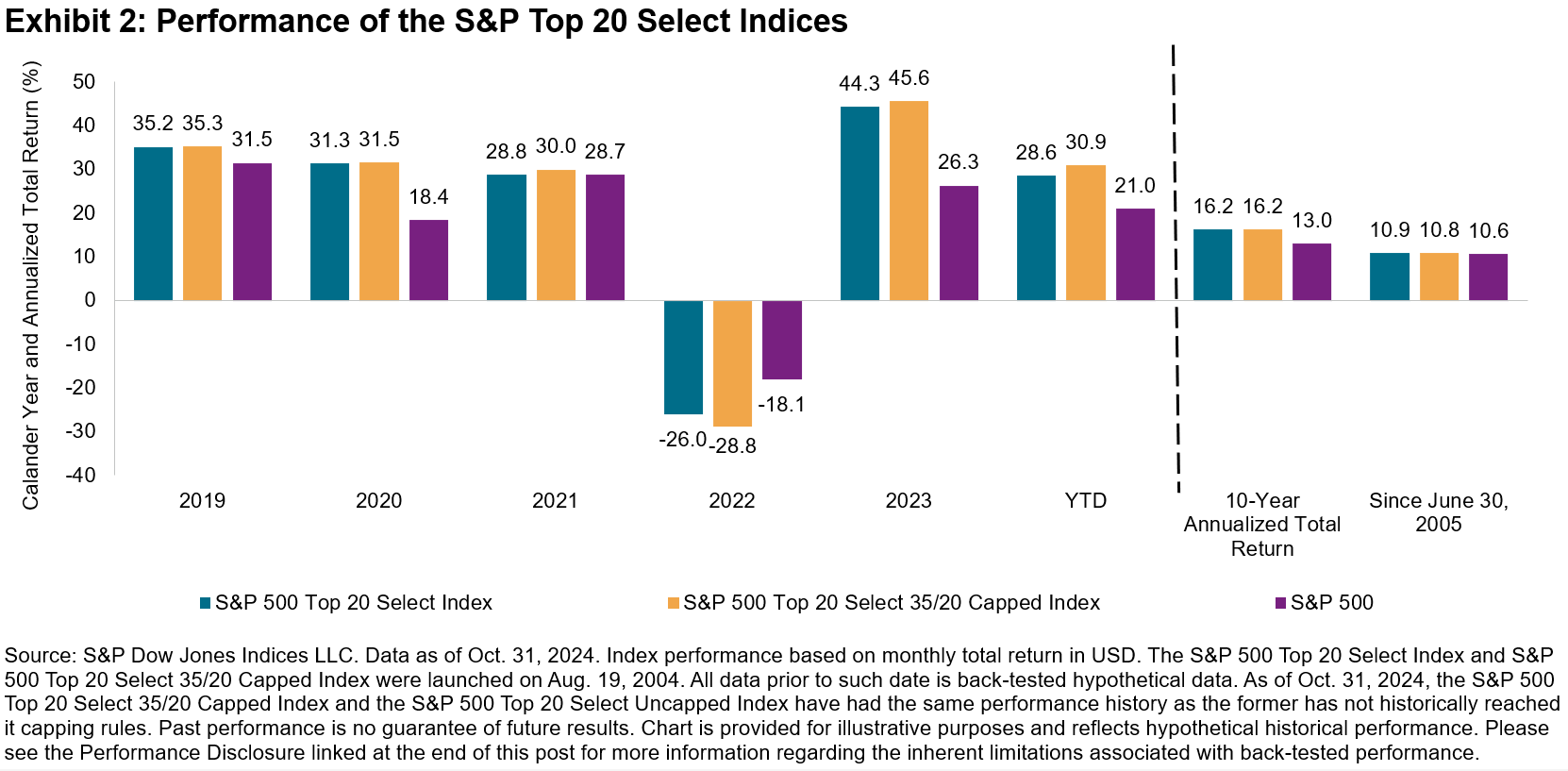

Exhibit 2 depicts an interesting picture when currency is taken into consideration. Over the past decade, one of the drivers of performance of the S&P 500 Top 20 Select 35/20 Capped Index (GBP) has been the depreciation of the British pound sterling against the U.S. dollar post-Brexit. Similarly, the S&P 500 Top 20 Select Index (TTM) (JPY) saw a boost in performance at the end of 2022, likely a reaction to the widening interest rate differentials between the U.S. and Japan that put the Japanese yen under pressure.

Some similar mega-cap index offerings, such as the S&P 500 Top 10 Index, the S&P 500 Top 20 Index and the S&P 500 Top 50 Index, use float-market cap (FMC) weighting with annual reconstitution. While performance may improve when the largest companies have higher weights in FMC indices, this can amplify concentration. By introducing capping mechanisms, the S&P 500 Top 20 Select Index Series helps increase diversification and reduce concentration risks.

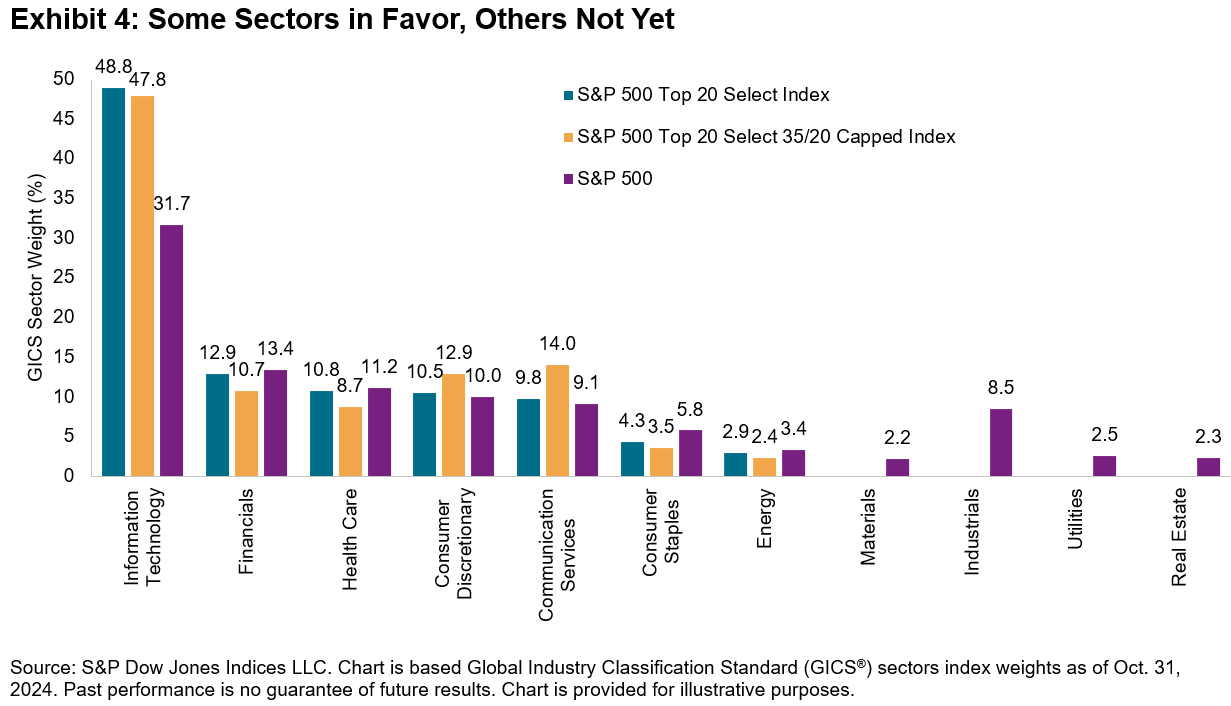

Two examples illustrate how the different capping mechanisms between the S&P 500 Top 20 Index and S&P 500 Top 20 Select Index affect sector weights (see Exhibit 3).

- The 4.2% weight difference in Communication Services was primarily driven by Alphabet A and Alphabet C. Their FMC weights were 4.6% and 3.8%, respectively, as of Oct. 31, 2024. However, since they are share classes of the same company, their combined weight is capped at 4.5% at rebalancing for the S&P 500 Top 20 Select Index Series.1

- In the single stock scenario, Amazon’s weight was capped from its original 8% level, contributing to a 2.4% weight difference in Consumer Discretionary.

As shown in Exhibit 4, the S&P 500 Top 20 Select Index outperformed the S&P 500 over the back-tested period, highlighting that the selection of the largest 20 companies has historically retained the top performers in the S&P 500. While the capping mechanism limits the extent of outperformance compared to the S&P 500 Top 20 Index, the S&P 500 Top 20 Select Index has historically had lower annualized volatility. As a result, the S&P 500 Top 20 Select Index has been able to post higher risk-adjusted returns with lower concentration risk.

Conclusion

The S&P 500 Top 20 Select Index Series offers a focused measurement of mega-cap stocks, addressing the demand for an index that tracks the largest and most influential companies in the U.S. equity market. By providing options with different capping mechanisms and currency offerings, the series provides a variety of index strategies that adapt to market dynamics around leading sectors and companies.

1 For more information on the multiple share classes treatment, please refer to the Multiple Share Classes section and the respective index methodology sections of S&P U.S. Indices Methodology.

The posts on this blog are opinions, not advice. Please read our Disclaimers.