The S&P/ASX 200 High Dividend Index seeks to measure the performance of the 50 companies with the highest 12-month forecast dividend yield from the S&P/ASX 200. Historically, the index has consistently delivered higher-than-market dividend yield and long-term outperformance against its benchmark. From July 2011 to September 2024, the index had an average trailing 12-month gross dividend yield of 5.5% and an annual excess return of 1.8% compared with the S&P/ASX 200.

Exhibit 1 shows the historical performance of the S&P/ASX 200 High Dividend Index. Year-to-date, the index experienced short-term underperformance against the market, lagging the S&P/ASX 200 by 3.6% as of Sept. 30, 2024. To better understand the source of the excess return, we are taking a closer look at the index’s short-term and long-term performance.

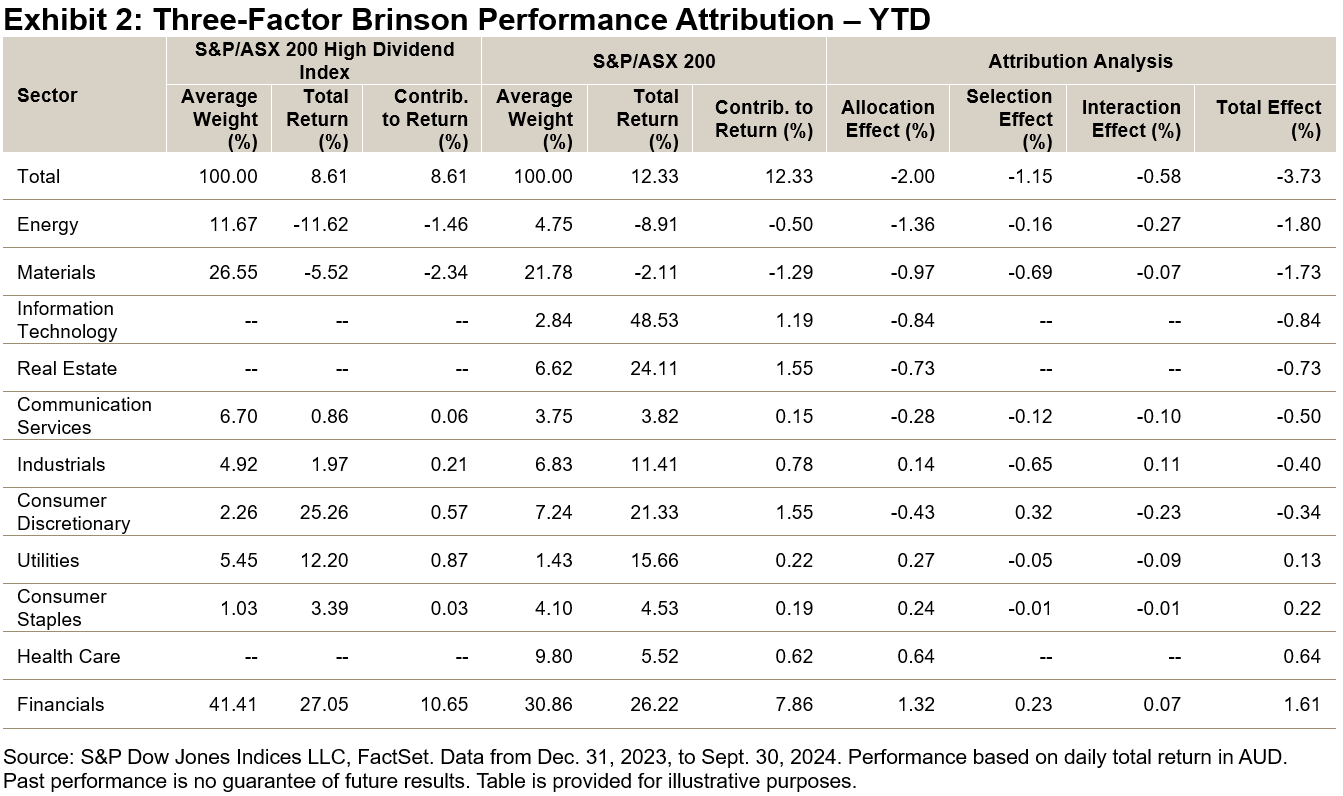

As Exhibit 2 shows, the YTD underperformance against the S&P/ASX 200 could be largely attributed to an overweight in the Energy and Materials sectors and an underweight in the Information Technology and Real Estate sectors. Increased weight in some high-yielding mega-caps such as Woodside Energy Group and Fortescue Ltd was the primary reason for the overweight in Energy and Materials. Lacking weight in Information Technology and Real Estate aligns with a high-dividend-yield strategy based on the S&P/ASX 200 Ex-A-REITs universe.

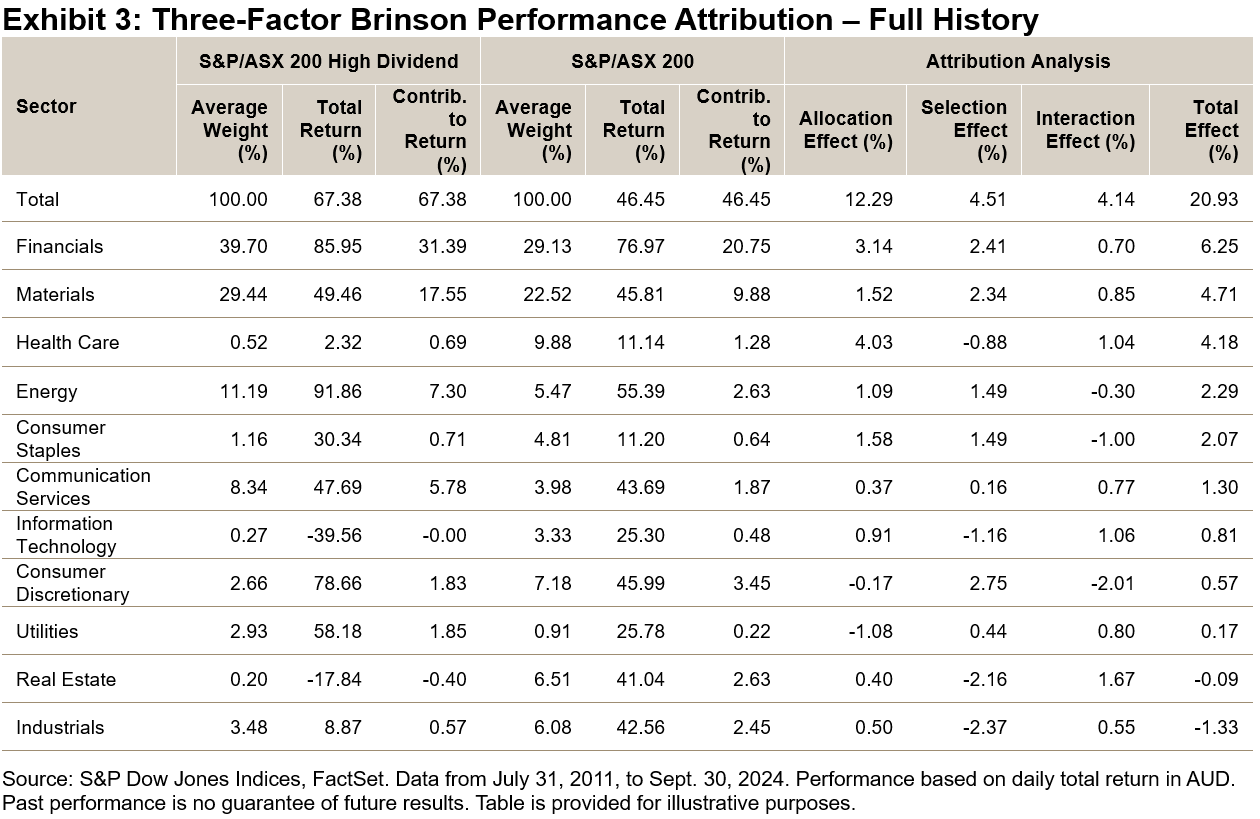

While overweighting Energy and Materials in the S&P/ASX 200 High Dividend Index has not delivered excess return YTD, it has been a major contributor to the long-term outperformance since 2021. From Dec. 31, 2020, to Sept. 30, 2024, the S&P/ASX 200 High Dividend Index had a total return of 68.2%1 in contrast to 46.5% from the S&P/ASX 200. We can mainly attribute the outperformance to allocation effect rather than selection effect (see Exhibit 3). Financials, Materials, Health Care, Energy and Consumer Staples were the largest contributors. Over the longer term, the S&P/ASX 200 Index underweighted Health Care and Consumer Staples, while overweighting Financials, Materials and Energy.

To sustain a higher-than-market dividend yield level, the index selects eligible stocks from the S&P/ASX 200 based on forecast dividend yield. Some familiar names may be excluded due to low yield ranking. As of the July 2024 rebalancing, Wesfarmers, Commonwealth Bank Australia and Macquarie Group had a forecast dividend yield of approximately 3.5%, which is relatively low compared with the weighted average dividend yield of 5.5% for the S&P/ASX 200 High Dividend Index.

As Exhibit 4 shows, the S&P/ASX 200 High Dividend Index has been able to maintain a dividend yield that is about 1.5% higher than the market level for the past 10 years. As of Sept. 30, 2024, the trailing 12-month dividend yield of the S&P/ASX 200 High Dividend Index is 5.14%, while that of the S&P/ASX 200 is 3.47%.

Like all factor indices, the S&P/ASX 200 High Dividend Index has experienced performance reversions during the short term. More importantly, the index consistently targets companies with high dividend yield and has historically delivered some excess return in the long term.

1 FactSet generated index return (see Exhibit 3) is 0.8% less than the official cumulative index total return of the S&P/ASX 200 High Dividend Index.

The posts on this blog are opinions, not advice. Please read our Disclaimers.