As well-known technology giants continue to make headlines globally, acquiring monikers such as FAANG and the Magnificent 7, there are smaller (yet no less innovative) Australian-listed companies across a range of sectors that are at the forefront of fast-paced technology advancements such as AI and digital transformation.

The S&P/ASX All Technology Index outperformed all Australian equity segments, sectors and styles in 2023, posting a total return of 36.0%. The index continued the same growth trajectory in the first half of 2024, ending the period with a total return of 17.0%. Over the longer term, the index has returned 12.7% per year over 5 years and 14.6% per year over 10 years, significantly outperforming the S&P/ASX 200.

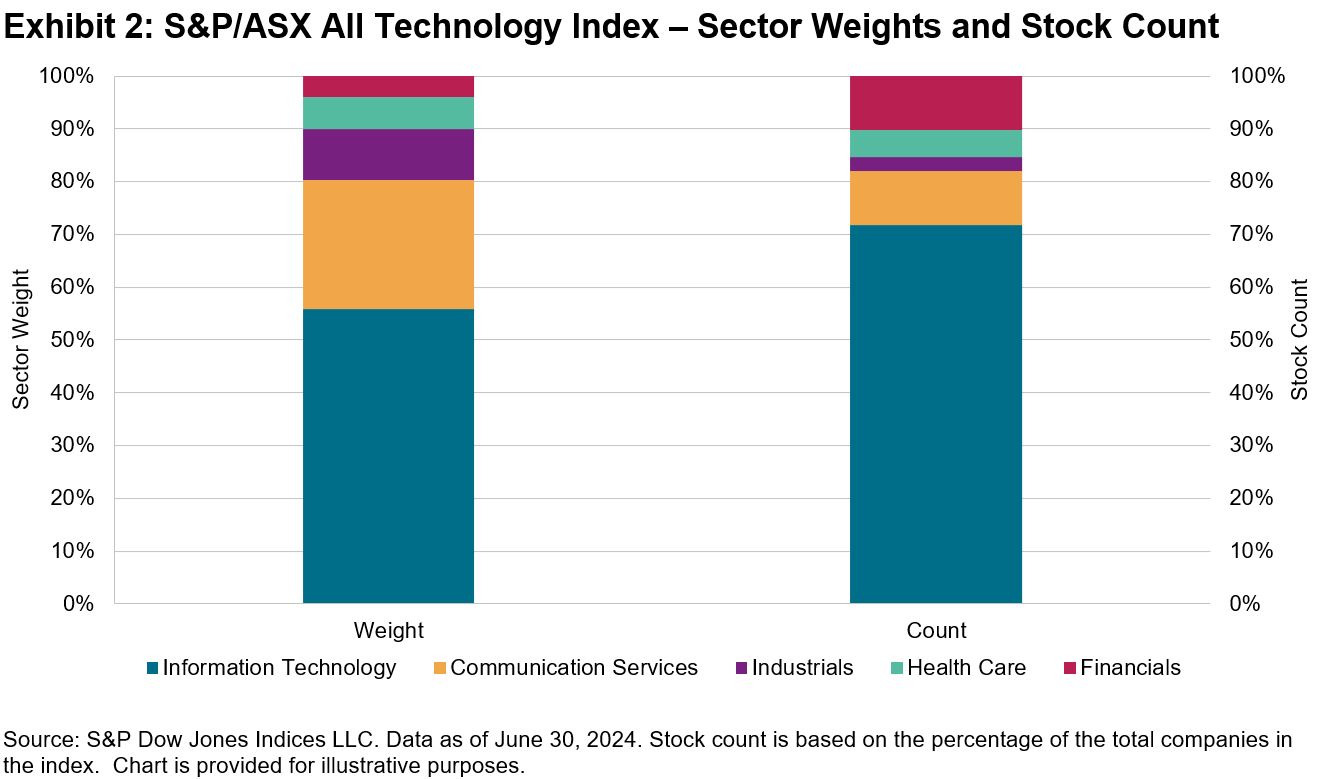

Unlike for the S&P 500®, Information Technology Companies Are Not Driving S&P/ASX 200 Returns

The Magnificent 7 (Apple, Microsoft, Nvidia, Amazon, Alphabet and Meta) make up over 30% of the S&P 500 and are key drivers of performance for the iconic large-cap U.S. equity index. However, the big banks and mining companies are still the main market drivers in Australia. The S&P/ASX 200 contains just 11 Information Technology companies, which comprise just over 3% of the flagship Australian equity index.

A Multi-Sector Approach to Technology throughout Size Segments

Launched in February 2020, the S&P/ASX All Technology Index reflects innovative technology-oriented companies across a broad range of sectors and industries, as well as market capitalization size segments. Currently comprising 39 companies, the index measures not just the Information Technology sector, but also companies in specific technology oriented sub-industries within the Health Care, Consumer Discretionary,1 Communication Services, Industrials and Financials sectors.

The S&P/ASX All Technology Index also looks beyond the well-established companies in the S&P/ASX 200. Smaller companies that could be future technology leaders are also eligible for inclusion, provided they meet the minimum float-adjusted market capitalization average of AUD 120 million over the previous three months at the rebalance reference date.2

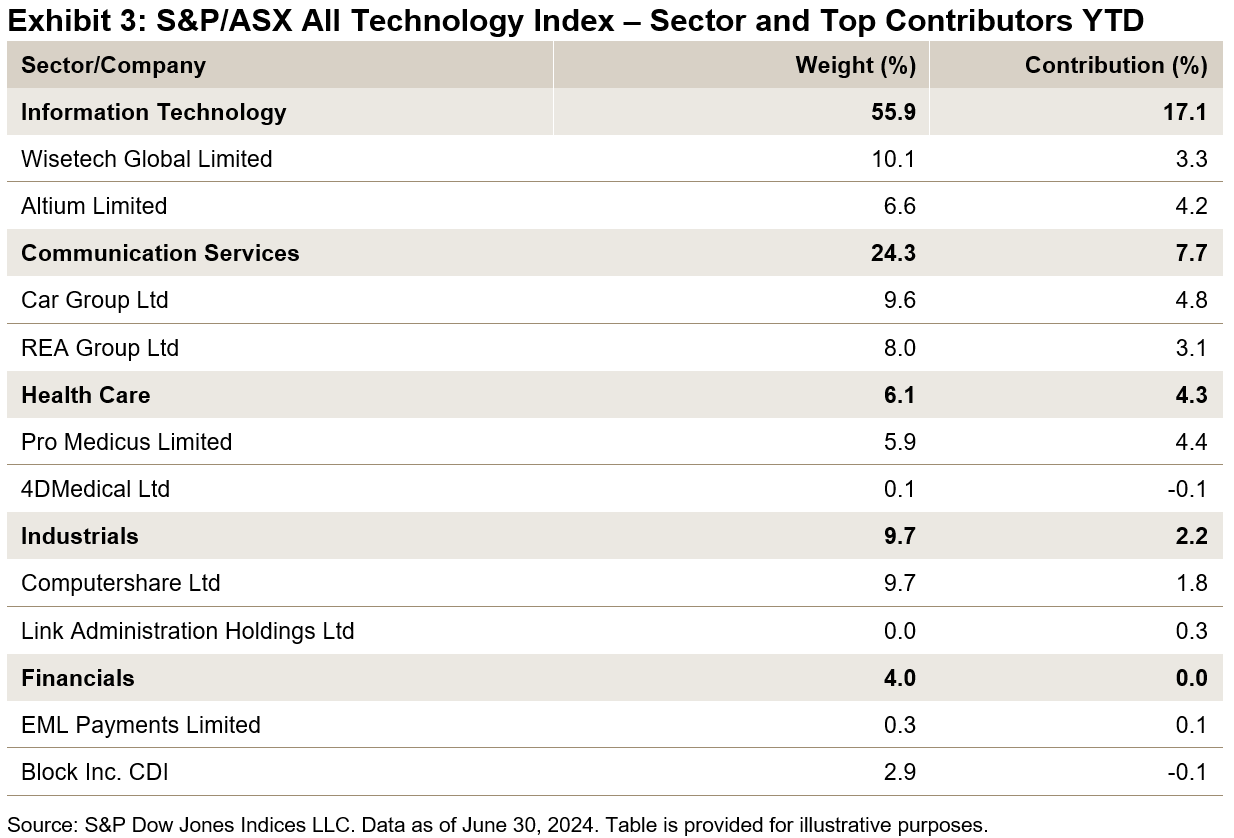

Performance Drivers

While the Information Technology sector contributed the most to performance YTD, key performance drivers at the stock level within the S&P/ASX All Technology Index have come from the Communication Services sector, with Car Group (formerly Carsales.com), and the Health Care sector, via Pro Medicus limited. All sectors contributed positively to the index’s return in the one-year period ending June 30, 2024.

New Index Additions and Deletions

Three new companies were added to the S&P/ASX All Technology Index at the recent June 2024 rebalance: Bravuria Solutions, Gentrak Group and Qoria Ltd. Bravuria Solutions is classified in the Information Technology sector and provides software solutions to financial services businesses. Initially listed on the ASX in 2016, Qoria Ltd. is in the Information Technology sector and provides child digital safety and well-being solutions. Gentrack Group is a New Zealand headquartered company with shares floated on both the NZX and ASX and provides cleantech solutions to Utilities companies.

Link Market Services was fully acquired by Mitsubishi UJF Trust Banking Corporation and exited the index in May 2024 upon the listing removal from the ASX.

1 Note, there are currently no companies that are eligible for inclusion from the Consumer Electronics sub-industry of the Consumer Discretionary sector.

2 For more information on index construction, see the methodology.

The posts on this blog are opinions, not advice. Please read our Disclaimers.