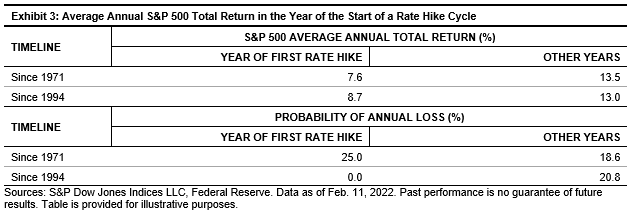

Market Resilience

The financial markets have been witness to numerous market cycles, trends, and crises, from the technology bubble in 2000 to the subprime housing crisis around 2007-08 and the collapse of Wall Street in 2009. 2020 brought the unexpected disruptor, coronavirus, and the ongoing pandemic changed the way markets and economies reacted. As with many disruptions, the first reaction was detrimental, with negative market reactions, as businesses were scrambling to adapt to the new environment. In March 2020, the S&P 500® dropped significantly, including its steepest one-day fall since 1987.1 It recovered from the low of 2,237.40 on March 23, 2020, to a high of 4,796.562 on Jan 3, 2022, a rise of 114%. The S&P BSE Sensex reacted similarly, with index levels falling to 25,981.24 on March 23, 2020, and a quicker recovery on Oct. 18, 2021, with a new high of 61,765.59; a rise of 138%, which has not been surpassed as of Feb. 8, 2022. Many other market indices such as the S&P Europe 350®, S&P/KRX Asia 100, S&P Japan 500, S&P/ASX 200, and S&P China 500 mimicked the recovery trend in other regions, showing the resilience of global financial markets and their ability to recover while adapting to new conditions.

The Shift to Passive

Investing styles and strategies are adapting to the new market, economic, and political dynamics that are compelling portfolio managers to review their objectives and goals. The growth in passive adoption is evident, with global assets under management having surpassed USD10 trillion and over 9,800 products as of December 2021.3 India also experienced a significant shift from being almost a purely active market, with minimal concentrated passive interest, to a boom in passive assets and number of passive products. With assets exceeding USD 50 billion and over 100 products,4 India’s growth in passive investment has ushered in new investor interest for diverse offerings.

The Active versus Passive Debate – Tilting the Scales

The debate of active versus passive has been ongoing. The recurring feature of benchmark outperformance is contributing to the adoption and growth of the passive investment space.

The S&P Indices Versus Active (SPIVA®) scorecard, which reflects on the trends of active fund management vis à vis benchmarks, has been a testament to the argument favoring indexing, as the statistics seem to tilt the balance in its favor. According to our SPIVA India Mid-Year 2021 Scorecard, over 86% of active Indian equity large-cap managers were beaten by the S&P BSE 100 over the previous 12-month period, and the numbers were similar for a three- or five-year horizon, with underperformance rates of 87% and 83%, respectively (see Exhibits 1 and 2). The index outperformance in large caps has been a recurring feature over the past few years. A new trend for the mid-/small-cap segment was a surprise for the market. Over the one-year period, 57% of active fund managers underperformed the S&P BSE 400 MidSmallCap Index, and the number was as high as 69% over the five-year horizon. This marks the beginning of opportunities for passive funds in this segment for India.

In a market that has had participants and product providers showcasing alpha in active portfolios for a long time, there is beginning to be an increased awareness on the merits of including indexing in investment strategies.

These SPIVA results are not unique to India, as similar results have been reflected over the one-year period across the SPIVA scorecards. Besides India, SPIVA is also published across another 10 markets, namely the U.S., Canada, Mexico, Brazil, Chile, Europe, MENA, South Africa, Japan, and Australia.

2 Its highest level as of Feb. 8, 2022.

4 ETFGI report as of September 2021.

The posts on this blog are opinions, not advice. Please read our Disclaimers.