Equity markets have changed considerably over the past 10 years, reflecting the growth of stocks and sectors in each market. While this growth has led to increased concentration in most of the world’s largest equity markets, Australia is a notable exception, as diversification has improved both in terms of stock concentration and along sector lines.

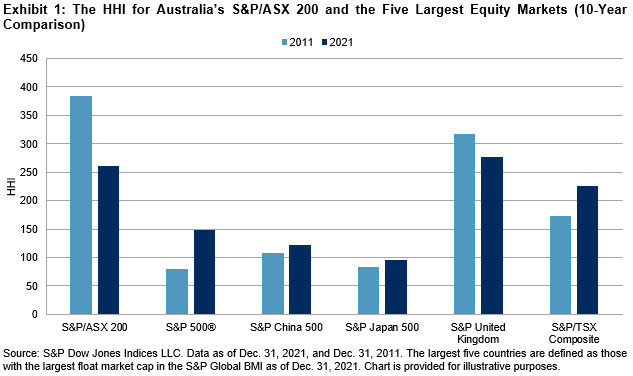

We can analyze stock concentration at a high level by using the Herfindahl-Hirschman Index (HHI). This index is a widely used measure of market concentration that can also be applied to stock market indices. It is calculated by squaring the market share (weight) of each stock in an index and then summing the resulting numbers. A greater HHI indicates a higher level of market concentration, while a lower value indicates less concentration.

Exhibit 1 shows that market concentration declined significantly for the S&P/ASX 200 over the past decade, while it increased in benchmarks measuring four of the world’s five largest equity markets. The S&P 500 and Canada’s S&P/TSX Composite experienced the largest increases, while the U.K. was the only top five market to see a decrease.

Examining the S&P/ASX 200 and S&P 500, we can see how the sector dynamic played out during this period. The weight of Materials and Financials declined for both indices, while Information Technology increased. However, the Information Technology sector had barely any participation in the S&P/ASX 200 10 years ago, which perhaps makes this change even more significant in Australia, given the small initial base.

In Exhibit 3, we can see how much each sector’s weight has changed over the past 10 years. While some sectors declined across all markets, such as Energy and Materials, others like Information Technology have increased—this was most notable in the U.S., with its share in the S&P 500 going up by 13%.

For the S&P/ASX 200, Materials and Financials each declined 6%, while Health Care and Information Technology increased by 7% and 4%, respectively. This is quite notable, as the sectors that have traditionally dominated the index (Financials, Materials, and Energy) accounted for 67% of the index 10 years ago, and now with the growth of Health Care, Real Estate, and Information Technology, this has lowered to 53%.

In conclusion, changes in the level of diversification varied across markets over the past decade. While the S&P/ASX 200 has become more diversified as a result of growth within newly emerging companies and sectors, growth in other markets was centered on previously large companies and sectors, which led to more concentration in the market overall.

The posts on this blog are opinions, not advice. Please read our Disclaimers.