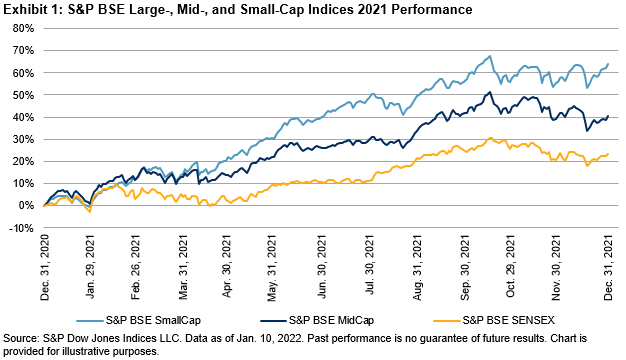

Indian equities had a stellar 2021—the S&P BSE SENSEX rose over 23%, outpacing most major emerging markets, though slightly lagging the S&P 500®, which gained 29%. Information Technology and Financials were the top contributors, adding 9% and 6%, respectively, to the performance of the Indian bellwether. Smaller Indian companies did even better than blue chips; the S&P BSE SmallCap returned over twice as much as the S&P BSE SENSEX, with a thumping 64% total return, while mid caps also provided a bright spot, rising 41% in 2021.

After exhibiting outsized moves in 2020, equities settled back into a more benign volatility regime; the annualized volatility of daily S&P BSE SENSEX returns dropped by more than half, to below 16% in 2021, and the S&P BSE MidCap and S&P BSE SmallCap volatility also subsided, dropping to 18% and 17%, respectively, from over 28% in 2020.

All S&P BSE sectors and industries were up for the year, with Power leading the way, soaring by 74%.

Despite the well-publicized setback for the Paytm IPO, the S&P BSE IPO surged 56% in 2021, the second-best-performing Indian equity strategy we regularly report on, lagging just 1% behind 2021’s winner, the S&P BSE Enhanced Value Index.

Majority state-owned firms have also had an outstanding year following a dismal 2019 and 2020, as the S&P BSE PSU and the S&P BSE CPSE climbed 48% and 43%, respectively.

Unlike equities, fixed income performance was much more muted. The S&P BSE India 10 Year Sovereign Bond Index edged up 2%, while the S&P India Sovereign Inflation-Linked Bond Index was essentially flat, as demand for inflation protection waned in parallel with a deceleration of inflation pressures in the Indian economy.

Consistent with global trends, indices incorporating environmental, social, and governance (ESG) factors are increasingly gaining in popularity with Indian investors. Their interest might have been raised further by the recent strong run of the S&P BSE 100 ESG Index, which outperformed its parent index for the third year running, returning 29% in 2021 against 27% for the S&P BSE 100.

One group that is having difficulty outperforming the S&P BSE 100 is that of active managers. According to our S&P Index Versus Active (SPIVA) India Mid-Year 2021 Scorecard, over 86% of active Indian equity large-cap managers were beaten by the S&P BSE 100 over the previous 12-month period, and the numbers don’t look much different on a three- or five-year horizon either, with underperformance rates of 87% and 83%, respectively. Offering an indication of the breadth of opportunity available to “stock pickers,” annualized dispersion (a measure of the spread of stock returns) in the S&P BSE SENSEX declined to a monthly average of 20% this year, having averaged 21% over the 2010-2019 period. Among other consequences, declining dispersion lowers the magnitude of rewards for active managers seeking to beat their benchmarks by over- or underweighting individual names.

The posts on this blog are opinions, not advice. Please read our Disclaimers.