This blog, the final in a series of three, reviews the performance of the new S&P Dividend Growers Indices and highlights some of their defensive characteristics. They are designed to track companies with consistently increasing dividends while excluding the top 25% highest-yielding eligible companies. Only companies that increase dividends consecutively for at least 10 and 7 years for the S&P U.S. Dividend Growers Index and S&P Global Ex-U.S. Dividend Growers Index, respectively, are eligible to be included.

Risk/Return Statistics

Exhibit 1 shows these indices’ back-tested risk/return statistics over various periods. Over the full period, the S&P Global Ex-U.S. Dividend Growers Index outperformed its benchmark by 2.44% annualized, while the S&P U.S. Dividend Growers Index slightly underperformed by 0.16%. It is important to frame the U.S. index’s underperformance in the context of the index’s defensive qualities (examined in the next section) and from a risk-adjusted perspective.

Here, risk-adjusted return is the ratio of annualized return and annualized volatility. With respect to volatility, both indices were substantially lower than their benchmarks. The full period volatilities of the S&P U.S. Dividend Growers Index and S&P Global Ex-U.S. Dividend Growers Index were 2.15% and 2.60% lower, respectively. Thus, on a risk-adjusted basis, both indices displayed superior risk-adjusted returns.

Down-Market Performance

The first blog in this series showed that companies with consistently increasing dividends displayed greater financial strength. As expected, higher-quality companies tended to outperform during periods of market stress.

Exhibit 2 shows the S&P Dividend Growers Indices experienced lower drawdowns than their benchmarks across the full back-test period. More recently, the S&P U.S. Dividend Growers Index and S&P Global Ex-U.S. Dividend Growers Index outperformed by 4.21% and 1.36%, respectively, during Q4 2018 and by 5.11% and 3.84%, respectively, during the COVID-19-related drawdowns in March 2020.

The defensive nature of the S&P Dividend Growers Indices is further evidenced by their historical capture ratios. A downside capture ratio of less than 100 indicates that a strategy has lost less than its benchmark during months when the benchmark return was negative. Exhibit 3 shows the S&P U.S. Dividend Growers Index and S&P Global Ex-U.S. Dividend Growers Index had downside capture ratios of 78.97 and 78.84, respectively, across the full back-test period.

Conversely, the upside capture ratio measures how a strategy has performed relative to the benchmark during months when the benchmark return was positive. Both S&P Dividend Growers Indices had upside capture ratios of less than 100, indicating they tend to participate less fully during up months.

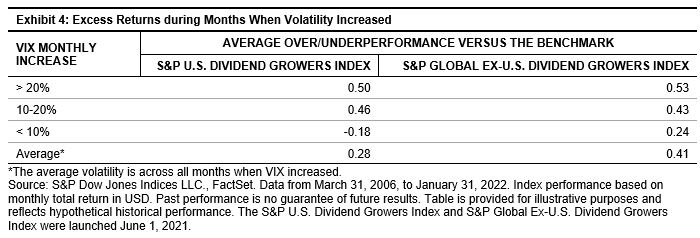

Another interesting way to examine the performance of the S&P Dividend Growers Indices is during periods of increasing volatility. Exhibit 4 shows the average monthly over/underperformance of each index across different thresholds of monthly increases in the CBOE Volatility Index® (VIX®).

Market volatility can cause significant price fluctuations in a portfolio; however, companies exhibiting sustained dividend growth tend to be higher quality and may help reduce volatility. When VIX increased more than 20% over the course of the month, the S&P U.S. Dividend Growers Index and S&P Global Ex-U.S. Dividend Growers Index outperformed by 50 bps and 53 bps per month on average, respectively.

Dividend Yield

Finally, let’s examine the historical dividend yield of the S&P Dividend Growers Indices. Compared with their benchmarks, the full-period average yield of the S&P U.S. Dividend Growers Index was 0.35% higher, while the S&P Global Ex-U.S. Dividend Growers Index was 0.55% lower.

Let’s recall that the objective of the index is to track companies that consistently raise dividends while excluding the top 25% highest yielding. The goal was not to generate superior yield but to select companies that are well managed and demonstrate sustainable growth. Thus, while the realized yield of the S&P Global Ex-U.S. Dividend Growers Index has generally been lower than its benchmark, this approach has produced superior total returns on absolute and risk-adjusted bases.

While dividend-paying stocks offer yield and the potential for price appreciation, not all dividend stocks are the same. Furthermore, certain dividend strategies may not be designed with the goal of earning a higher yield but rather greater price appreciation or lower risk. Overall, dividend growers tend to be higher-quality companies that exhibit superior risk-adjusted return and tend to outperform during down markets.

The posts on this blog are opinions, not advice. Please read our Disclaimers.