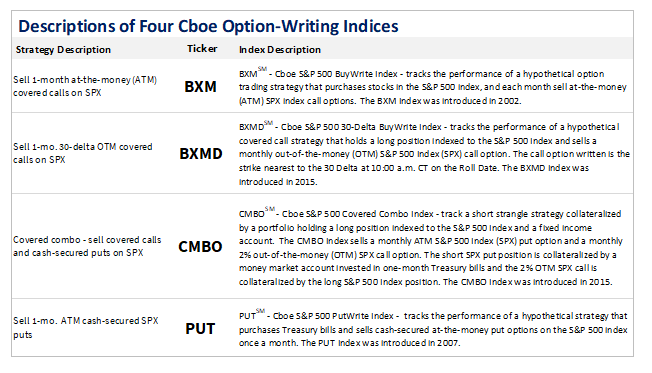

35 Years of Hedging Indices

Below are three Cboe S&P benchmark indices that theoretically “buy “SPX put options as part of their index methodology and have 35 years of back-tested performance history going back to June 30, 1986. As shown below, the three options indices were introduced in either 2008 or 2015, and the data histories before the introductions are back-tested.

- Cboe S&P 500 5% Put Protection Index (PPUTSM) tracks the performance of a hypothetical strategy that holds a long position indexed to the S&P 500 Index and buys a monthly 5% OTM SPX put option as a hedge. The PPUT Index was introduced in 2015.

- Cboe S&P 500 95-110 Collar Index (CLLSM) tracks the performance of a strategy that purchases stocks in the S&P 500 Index, and each month sells SPX call options at 110% of the index value, and each quarter purchases SPX put options at 95% of the index value. The CLL Index was introduced in 2008.

- Cboe S&P 500 Zero-Cost Put Spread Collar Index (CLLZSM) tracks the performance of a hypothetical option trading strategy that 1) holds a long position indexed to the S&P 500 Index; 2) on a monthly basis buys a 2.5% – 5% SPX put option spread; and 3) sells a monthly OTM SPX call option to cover the cost of the put spread. The CLLZ Index was introduced in 2015.

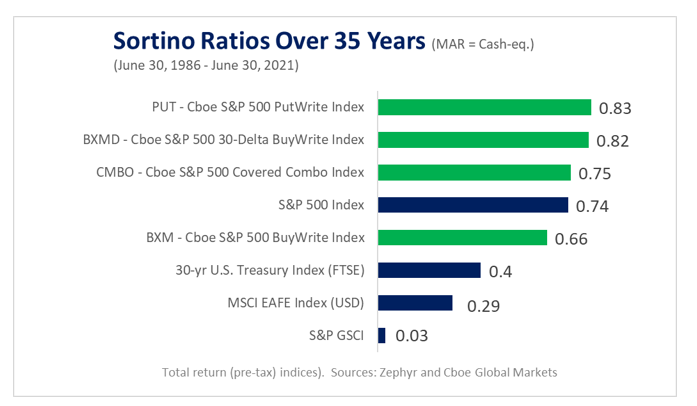

Histogram and Less Tail Risk

The histogram chart shows that the methodology element of theoretically “buying” of puts by the PPUT Index helped lessen the left tail risk when looking at back-tested data over 35 years. The S&P 500 Index had 35 monthly declines of down 6% or more, while the PPUT Index had 18 such declines. There is a hypothetical cost imputed to the Index for the for the paying of premiums for the put options, and the PPUT Index also had fewer monthly gains of more than 4%.

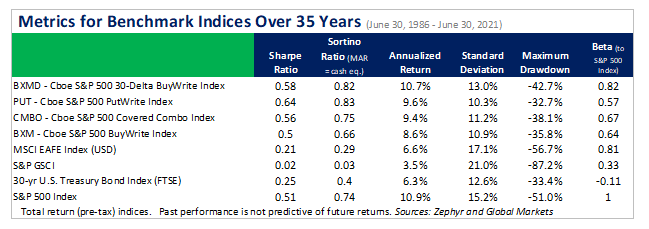

Lower Betas and Standard Deviations for the Indices

In their analysis of potential asset classes for diversification purposes, asset managers may look to see investments with relatively low betas. The table below shows that all three Cboe S&P indices had betas of less than 0.75 over the 35-year period. The three Cboe S&P indices had higher annualized returns than the MSCI EAFE Index, but lower than the S&P 500 Index.

To Learn More

- Please register for Webinar on 35 Years of Options Index Performance on July 28, 2021, featuring four speakers, including Gaurav Sinha, Managing Director, Head of Americas, Global Research & Design, at S&P Dow Jones Indices (S&P DJI)

++++++++++++++++++++

Disclaimer

Options involve risk and are not suitable for all investors. Prior to buying or selling an option, a person must receive a copy of Characteristics and Risks of Standardized Options. Copies are available from your broker or from The Options Clearing Corporation, One North Wacker Drive, Suite 500, Chicago, Illinois 60606 or at www.theocc.com. The CLLSM, CLLZSM, and PPUTSM indexes (the “Indexes”) are designed to represent proposed hypothetical options strategies. The actual performance of investment vehicles such as mutual funds or managed accounts can have significant differences from the performance of the Indexes. Investors attempting to replicate the Indexes should discuss with their advisors possible timing and liquidity issues. Like many passive benchmarks, the Indexes do not take into account significant factors such as transaction costs and taxes. The three Cboe S&P indexes in this blog were announced in either 2008 or 2015 as set forth above. Information presented prior to the announcement dates is back-tested. Back-tested performance is not actual performance, but is hypothetical. A limitation of back-tested information is that it reflects the application of the Index methodology in hindsight. No theoretical approach can completely account for the impact of decisions that might have been made during the actual operation of an index. Cboe Global Indices, LLC calculates and disseminates the Indexes pursuant to an agreement with S&P Dow Jones Indices LLC (“S&P DJI”). CLLSM, CLLZSM, and PPUTSM are service marks of Cboe Exchange, Inc. or its affiliates. S&P®, S&P 500® and SPX® are registered trademarks of Standard & Poor’s Financial Services, LLC (“S&P”) and have been licensed for use S&P DJI and sublicensed by Cboe Exchange, Inc. The S&P 500 and S&P GSCI are products of S&P DJI. Any products (including options) that have the S&P Index or Indexes as their underlying interest are not sponsored, endorsed, sold or promoted by S&P DJI or S&P and neither S&P DJI nor S&P makes any representations or recommendations concerning the advisability of investing in products that have S&P indexes as their underlying interests.

The posts on this blog are opinions, not advice. Please read our Disclaimers.