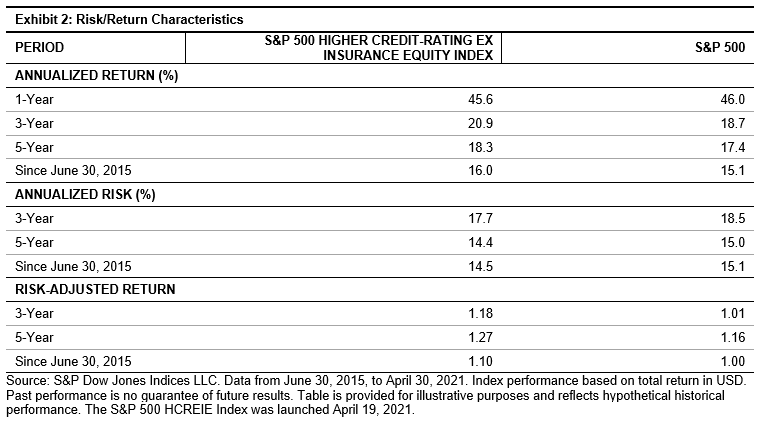

The onset of the COVID-19 pandemic a year ago produced the highest-ever monthly volatility reading for the S&P 500® in March 2020. Volatility began to decline as the market’s recovery began, but if we measure volatility on a 12-month trailing basis, as we do in Exhibit 1, we see the sustained impact of last year’s ructions.

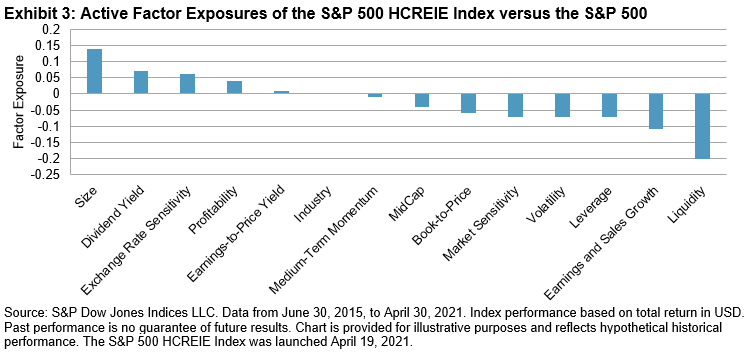

Not only is overall market volatility now close to pre-pandemic levels, the same seems to be true for all sectors of the S&P 500. Exhibit 2 shows that one-year volatility declined significantly in every sector compared to three months earlier. While volatility in all sectors declined by at least 10%, the biggest drops came in Energy, Financials, and Utilities, which declined by approximately 20%.

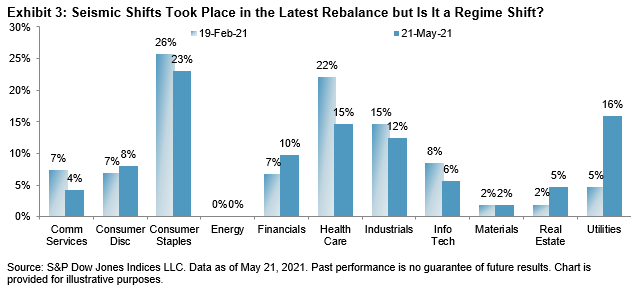

Significant changes also took place in the latest rebalance for the S&P 500 Low Volatility Index, effective after market close May 21, 2021. The new allocation, as shown in Exhibit 3, is much closer to the allocations of pre-pandemic times. Stalwarts like Financials, Real Estate, and Utilities resumed their places in the index; Utilities added 11% to its weight. Health Care, Communication Services, and Technology (sectors that were the lifelines of locked-down livelihoods) scaled back to make room. Energy’s volatility remained too high to make the cut. In all, 34 names changed in the index, the largest change since the record rebalance of May 2020.

The S&P 500 Low Volatility Index chooses its constituents based on volatility at the stock level, but sector level volatility can give us insight into the dynamics that drive the changes. Hopefully, in this instance, sector volatility is also a narrative of better things to come.