On May 29, 2020, I joined S&P Global’s The Essential Podcast, “A View to the Future – China Beyond the Pandemic,” to discuss the Chinese equity market’s performance and the macroeconomic trends during and beyond the COVID-19 pandemic. This blog includes some key highlights we discussed, along with the related index performance observed in the Chinese equity market.

As mentioned in our previous blog, “How the Chinese Equity Market Responded to the Domestic and Global Coronavirus Outbreak,” the China A-shares market experienced a substantial drawdown, with significant industry return spreads during the early and middle stages of the COVID-19 pandemic in China. The Health Care sector performed the best, while consumer-based constituents such as airlines and hotels lagged the most.

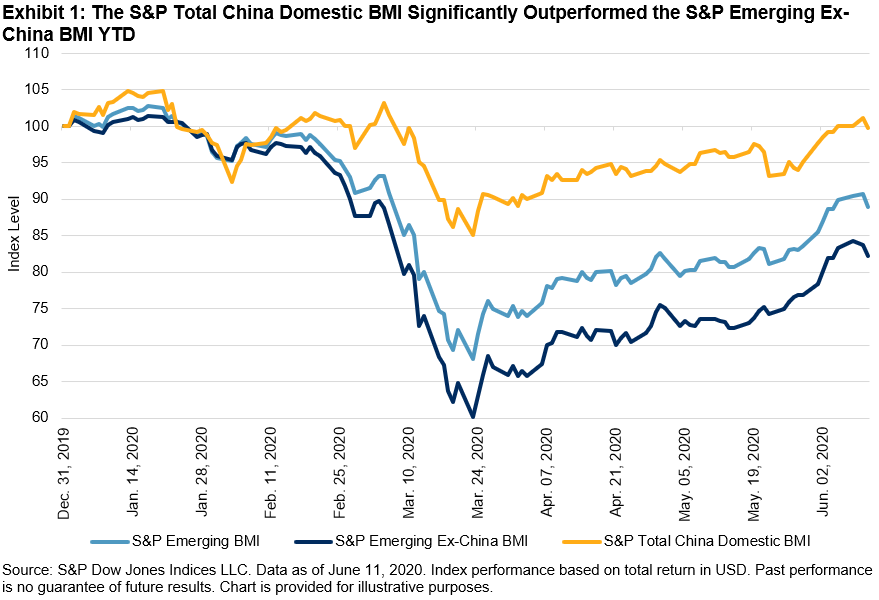

However, as China is a non-oil-exporting country with minimized exposure to falling oil price and the Chinese renminbi has remained largely stable relative to other emerging market currencies, Chinese equities have experienced lower volatility and have become an unexpected stabilizing force for emerging markets (see “An Unlikely Stabilizer in Emerging Markets” for more details). Year-to-date, the S&P Total China Domestic BMI outperformed the S&P Emerging ex-China BMI by 21.4% in USD terms.

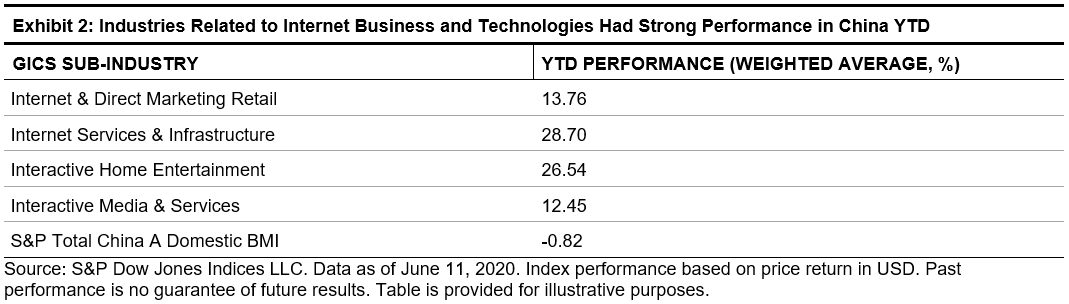

Companies engaging in internet business and technologies that provide contactless services performed relatively well during the pandemic. Due to the lockdown, the time people spend working from home, online shopping, and viewing social media and online entertainment has significantly increased. This resulted in a shift in business and consumer behavior, and this trend has continued even post-lockdown.

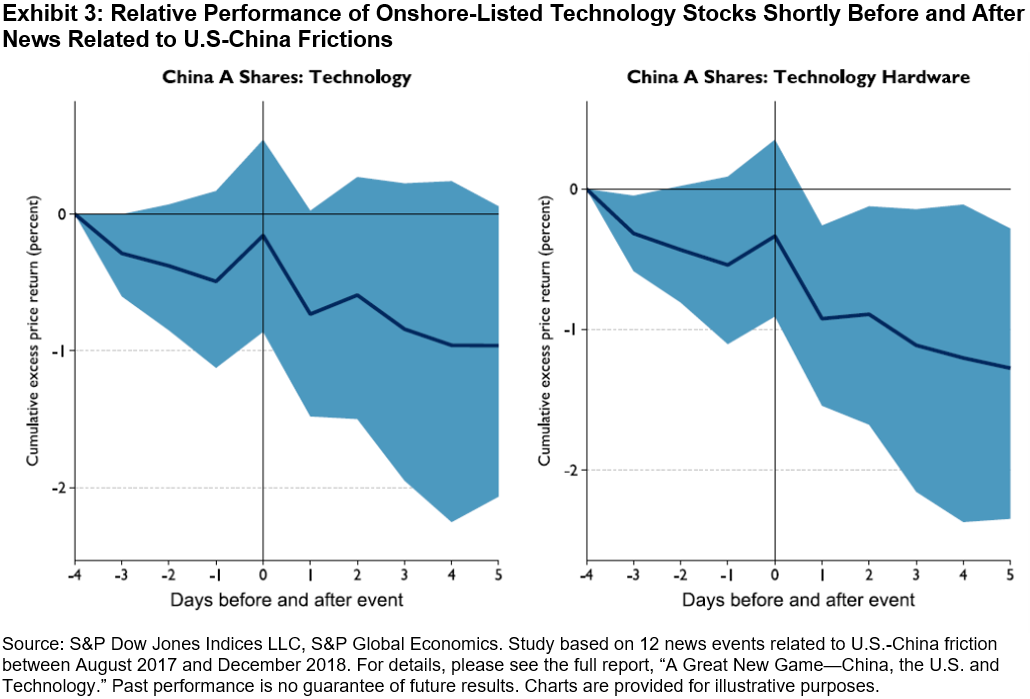

During to the COVID-19 crisis, rising tensions between the U.S. and China were seen with continuous investment restrictions, export controls, tariffs, and policies to slow the pace of technology transfer to China. As pointed out in “A Great New Game—China, the U.S. and Technology,” published by S&P Global’s China Senior Analyst Group last year, the focus of U.S. trade and investment policies has turned to technology more than shrinking the bilateral trade deficit. In response to that, Chinese onshore technology stocks tended to suffer more than the overall market shortly after news related to U.S.-China friction.

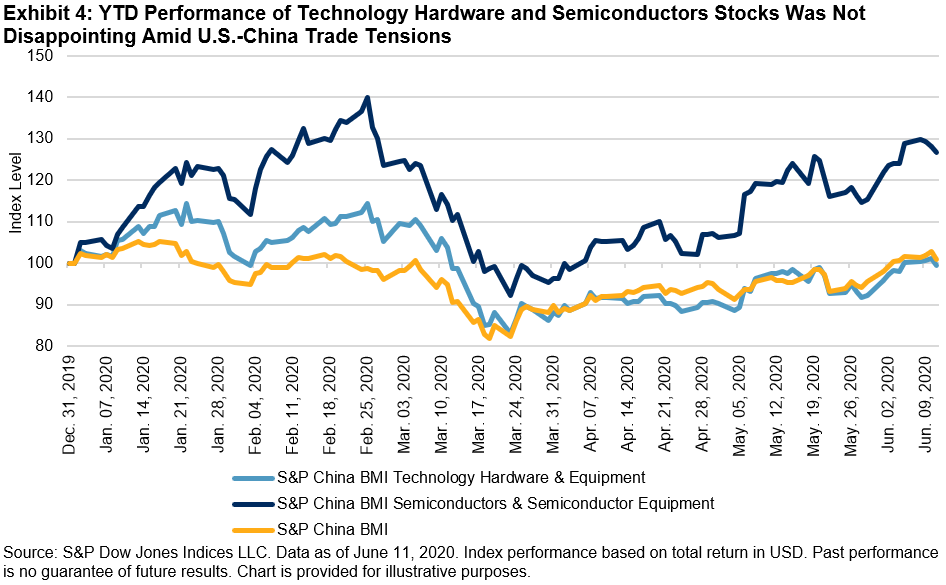

If friction between the U.S. and China continues to persist, foreign companies may reduce their supply chain reliance on China, and the slowing pace of technology transfer from foreign countries in the production process in China may also hurt China-based companies’ competitiveness over time. However, S&P Global Rating’s recent comment, “Decamping Factories Unlikely To Unplug China’s Growth Advantage,” suggested many foreign manufacturers are also likely to continue investing in China due to the fast-growing domestic market. Equity prices seemed to align with this view, as we did not see significant underperformance in Technology Hardware stocks and saw outperformance in Semiconductors stocks in China since the beginning of this year.

References:

The Essential Podcast, Episode 11: A View to the Future – China Beyond the Pandemic, Priscilla Luk and Nathan Hunt, S&P Global (May 29, 2020)

How the Chinese Equity Market Responded to the Domestic and Global Coronavirus Outbreak, Priscilla Luk, S&P Dow Jones Indices (April 5, 2020)

An Unlikely Stabilizer in Emerging Markets, John Welling, S&P Dow Jones Indices (Apr 3, 2020)

A Great New Game—China, the U.S. and Technology, The China Senior Analyst Group, S&P Global (May 14, 2019)

Decamping Factories Unlikely To Unplug China’s Growth Advantage, KimEng Tan & Rain Yin, S&P Global Ratings (May 21, 2020)

The posts on this blog are opinions, not advice. Please read our Disclaimers.