Over the last few months, the COVID-19 pandemic has taken its toll on the global economy in a way that no one could have expected. Unsurprisingly, many companies have had to reassess their dividend policy—in many cases resorting to cutting, postponing, or even suspending dividend payments.

Against this background, it is beneficial to review the selection criteria of S&P DJI’s dividend indices. Not only do all of our dividend indices select constituents based on yield, but they also use a quality screen that focuses on their ability to pay dividends in the future. The quality screen varies with each index and is also dependent on the region.

Simply because a company pays a high dividend (whether absolute amount or relative to its price) doesn’t always make it a wise investment. After all, a company paying too much in dividends may be left with little to no reserves in times of market turbulence; as a result, its dividends may be at higher risk for cancellation. Also, a high dividend yield may simply be a result of a decline in the company’s stock price, all else equal. These scenarios are often referred to as being “dividend traps,” and in order to avoid these traps, it is important to incorporate quality screens.

This blog looks at three core dividend series offered by S&P DJI—S&P Dividend Aristocrats®, Dow Jones Select Dividend, and S&P Dividend Opportunities—with respect to their individual screening features to shed more light on the factors that each considers when selecting constituents.

S&P Dividend Aristocrats Indices

The S&P Dividend Aristocrats Indices are well known for their stringent quality screen which is the hallmark of their methodology. This family focuses on stable dividend growth, requiring constituents to have consistently increased dividends every year for a certain period of time that varies by region.

The longest of these is the S&P 500® Dividend Aristocrats, for which constituents must have consistently increased dividends every year for at least 25 years, subject to stock diversification criteria (see Exhibit 1).

Dow Jones Select Dividend Indices

The Dow Jones Select Dividend Indices strive to strike a balance between high yield and dividend sustainability. This index series incorporates stability and quality criteria, which are put in place to avoid dividend traps.

The Dow Jones U.S. Select Dividend Index is designed to measure the performance of 100 high-dividend-paying companies that meet specific criteria, excluding REITs. Exhibit 2 includes more details on the index methodology. The quality screens serve to include companies with a solid track record of dividend payments (I and II), sufficient coverage to sustain its current dividend level (III), and positive earnings (IV).

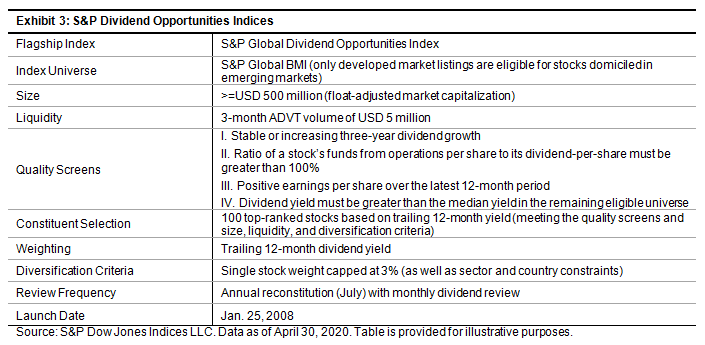

S&P Dividend Opportunities Indices

The S&P Dividend Opportunities Indices are designed to measure the performance of high-yield common stocks from global markets that meet diversification, stability, and tradability requirements.

The S&P Global Dividend Opportunities Index seeks to track 100 common stocks from around the world that offer high dividend yields. As Exhibit 3 shows, constituents are subject to quality screens in order to include companies with a track record of stable or increasing dividend growth (I), enough cash flow from core operations to support dividends (II), and positive earnings (III).

The recent market volatility underscores the importance of including additional criteria, beyond yield, to select constituents within dividend indices. As illustrated above, the different dividend indices offered by S&P DJI attempt to avoid potential pitfalls of dividend investing by incorporating quality screens.

The posts on this blog are opinions, not advice. Please read our Disclaimers.