Introduction

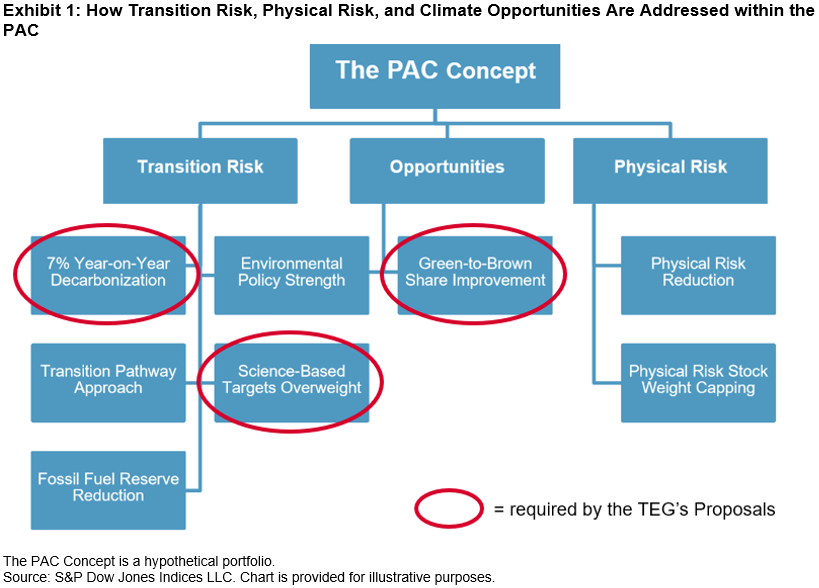

In January 2020, S&P Dow Jones Indices (S&P DJI) released a paper for the S&P Eurozone Paris-Aligned Climate Index Concept (PAC Concept). The PAC Concept conceptualizes the proposals of the EU Technical Expert Group on Sustainable Finance (TEG), as published in its Final Report on Climate Benchmarks and Benchmarks’ ESG Disclosure dated September 2019,[1] for the Paris-aligned benchmark and incorporates transition risk, physical risk, and climate opportunities, as laid out by the TCFD[2] (see Exhibit 1). The PAC Concept implements innovative and forward-looking Trucost[3] datasets: physical risk and the transition pathway approach. This blog outlines two methods, which the PAC Concept applies to meet the TEG’s proposals.

7% Year-on-Year Decarbonization

To align with the TEG’s proposals for the Paris-aligned benchmark, a 50% carbon footprint reduction and decarbonization[4] by 7% year-on-year are required. Complexity lies in the 7% year-on-year decarbonization: this must occur not only at rebalance but also when calculated using average weights over the period. Consequently, as weights drift between rebalances, the carbon footprint must stay below the 7% year-on-year trajectory on average. Therefore, the PAC Concept’s trajectory targets 5% below the required level of decarbonization and is rebalanced quarterly. This allows for intra-rebalance weight fluctuations, while remaining compliant.

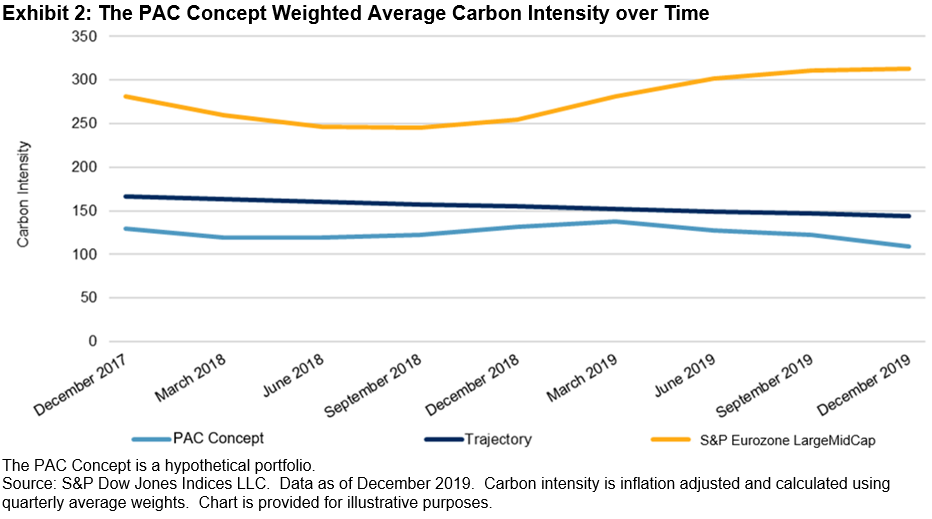

The middle line in Exhibit 2 shows the required 7% year-on-year decarbonization, the yellow line represents the carbon intensity of the parent index, and the bottom line the PAC Concept’s carbon intensity, measured using average weights.[5] Over the period, the parent index’s carbon intensity decreases then increases—a good methodology test for the PAC Concept. The PAC Concept’s carbon intensity starts to increase toward the trajectory line; however, at rebalance the index’s decarbonization buffer[6] forces it below required carbon intensity.

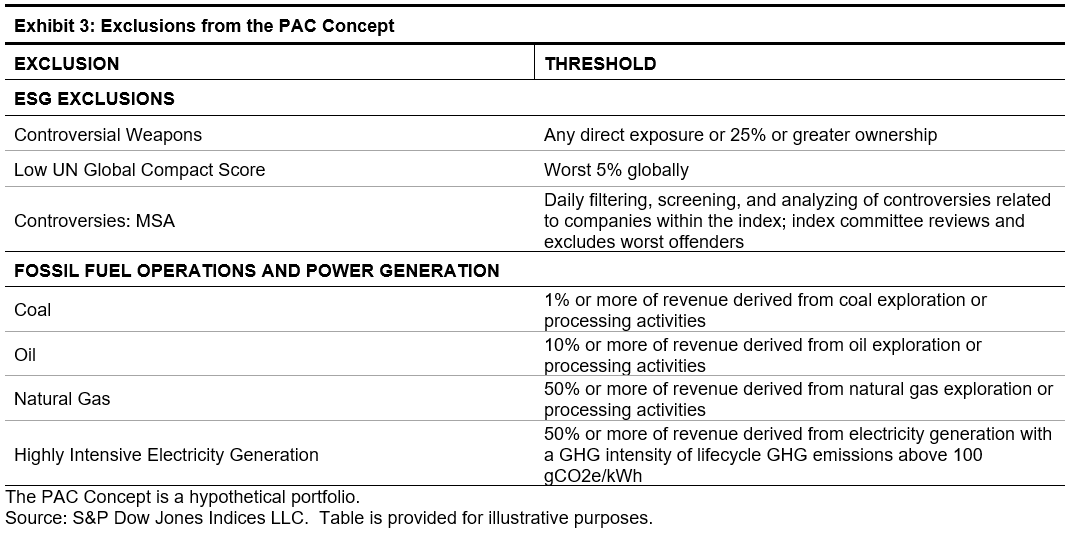

Exclusions

The TEG’s proposals also require certain exclusions. These exclusions are based on:

- Controversial weapons;

- Societal norms (which the PAC Concept tackles through the use of UN Global Compact exclusions);

- Severe controversies surrounding environmental issues (the PAC Concept excludes severe controversies in all areas of ESG);

- Coal exposure;

- Oil exposure;

- Natural gas exposure; and

- Highly intensive electricity generation.

Exhibit 3 outlines the exclusions that have been implemented.

Please refer to the PAC concept paper for further details.

[1] The EU Technical Expert Group on Sustainable Finance Final Report on Climate Benchmarks and Benchmarks’ ESG Disclosure, September 2019. The final report will serve as the basis for the European Commission for the drafting of the delegated acts under Regulation 2019/2089.

[2] TCFD. (2017). Final Report: Recommendations of the Taskforce on Climate Related Financial Disclosures.

[3] A part of S&P Global.

[4] Decarbonization refers to the reduction of an index’s carbon footprint.

[5] As advised by the TEG.

[6] The buffer is referring to targeting below the 7% year-on-year trajectory line.

The posts on this blog are opinions, not advice. Please read our Disclaimers.