Several catalysts, including U.S. Corn Belt production issues, drove corn futures prices to a new five-year high in June 2019. Investors were net short corn in May 2019, and the short covering contributed to the break higher. Prices broke through the 2017 peak after heavy floods in the Midwest prevented farmers from planting corn in a timely manner. While they have typically finished planting by May, this year U.S. farmers continued to plant until the end of June. As seen in Exhibit 1, it took a full extra month to get the crop planted. With new farming technology, farmers are able to plant 24 hours a day and can get the crop into the ground quickly when given the opportunity. This season, the new U.S. farmer bailout package encouraged farmers to continue planting even under less-than-ideal conditions because government payments are based on acres planted.

There are risks associated with planting corn so late in the season because it can negatively affect the final yield, and this is already apparent with 2019’s crop conditions. As can be seen in Exhibit 2, farmers are experiencing some of the worst crop conditions of the past five years. At this point in the season, we have not seen lower rated conditions since 2012. According to Farm Futures, growers continue rating crop conditions behind those reported in the USDA Crop Progress report. This leads to speculation about how the final crop will turn out, with the potential for a significant cut to supply affecting prices in the second half of 2019.

In past similar scenarios (like in 1995), corn prices moved higher throughout the growing season and the bull run continued into the end of the year after the harvest verified that the poor crop conditions had translated into a lower yield and a smaller crop. This year, much will depend on weather conditions over the remainder of the growing season and, possibly more importantly, the final acreage number. Many market participants expect that the final acreage level will eventually be adjusted lower to reflect the late planting pace.

The S&P GSCI Corn offers market participants the ability to capture these idiosyncratic movements. The index was up 12.655% YTD as of July 11, 2019. Supply shocks can drastically affect the price of the underlying commodities in agricultural markets. Tactical investments in commodities when the conditions are good offer an interesting return stream for investors. This recent move in corn is an example of how an allocation to commodities can do just that.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

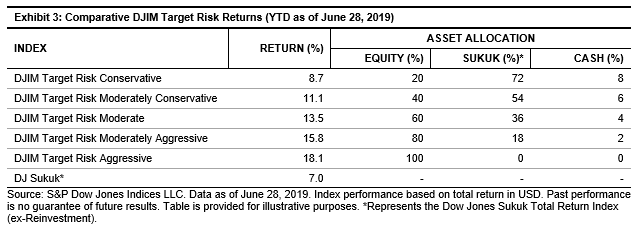

The outperformance trend played out across major regions as Shariah-compliant benchmarks measuring U.S., Europe, Asia Pacific, and developed markets each continued to outperform conventional equity benchmarks by meaningful margins. Emerging markets and the Pan Arab region were exceptions, as Shariah-compliant benchmarks in these regions underperformed their conventional counterparts.

The outperformance trend played out across major regions as Shariah-compliant benchmarks measuring U.S., Europe, Asia Pacific, and developed markets each continued to outperform conventional equity benchmarks by meaningful margins. Emerging markets and the Pan Arab region were exceptions, as Shariah-compliant benchmarks in these regions underperformed their conventional counterparts.

Financials—representing the largest sector of the index by weight—contributed most to the overall performance in Q2, adding 0.9% to the S&P China 500. The Financials sector gains were easily negated however, as the next three sectors by size—Consumer Discretionary, Communication Services, and Industrials each contributed -0.6%, -0.8%, and -0.8%, respectively, representing over 80% of index performance during the quarter.

Financials—representing the largest sector of the index by weight—contributed most to the overall performance in Q2, adding 0.9% to the S&P China 500. The Financials sector gains were easily negated however, as the next three sectors by size—Consumer Discretionary, Communication Services, and Industrials each contributed -0.6%, -0.8%, and -0.8%, respectively, representing over 80% of index performance during the quarter.

We also studied the distribution of fund returns and calculated their mean, standard deviation, and skew (see Exhibit 2). The study compared the fund returns data distribution with a hypothetical normal curve constructed with the same mean and standard deviation. Again, we considered the large-cap category and mid-/small-cap category for this analysis.

We also studied the distribution of fund returns and calculated their mean, standard deviation, and skew (see Exhibit 2). The study compared the fund returns data distribution with a hypothetical normal curve constructed with the same mean and standard deviation. Again, we considered the large-cap category and mid-/small-cap category for this analysis.