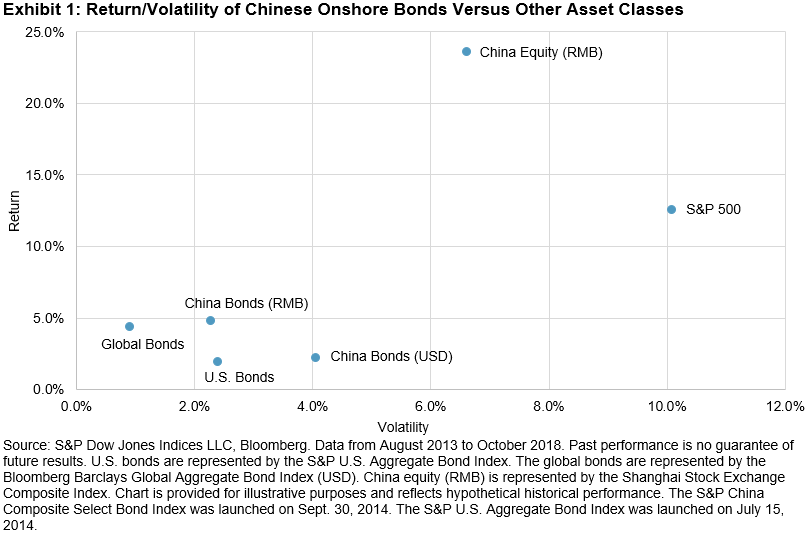

While many investors are concerned about the fact that benchmark indexes for major investment classes are down year-to date, more investors are using S&P 500® options for goals related to risk management and income enhancement.

- On December 20 open interest for Cboe S&P 500 (SPX(SM) and SPXW) options surpassed 21 million for the first time ever in its history of more than 35 years, and hit a new all-time record high of 21,424,148 contracts, and

- The Cboe S&P 500 95-10 Collar Index (CLLSM), an index that tracks the performance of a strategy that buys SPX puts for protection and sells SPX calls for income, rose 2% in 2018 (through December 20).

CHARTS ON RECORD OPEN INTEREST FOR S&P 500 OPTIONS

The chart below shows that open interest for Cboe’s S&P 500 options rose from 1.1 million in 1993, to 16 million in July 2018, to a record 21.4 million contracts on December 20.

RECENT COMMENTS FROM TRADERS AND PORTFOLIO MANAGERS

In the past week I spoke with a number of traders and portfolio managers to inquire about their thoughts about the growth to record open interest in S&P options. The responses I heard included –

- “Higher volatility levels in recent months make the markets more attractive for options sellers who wish to generate more premium.”

- “Cash-secured put-writing has gained more mainstream acceptance”

- “There is more interest in portfolio protection and generation of income”

- “There is more trading in SPX call spreads. Look at SPX call open interest which has been beefed up by the sheer quantity of multi-legged call trades that have been trading to hedge the other tail. Millions of calls since the Sept 21st expiry!”

- “We are seeing SPX volatility sellers with some big multi-leg positions”

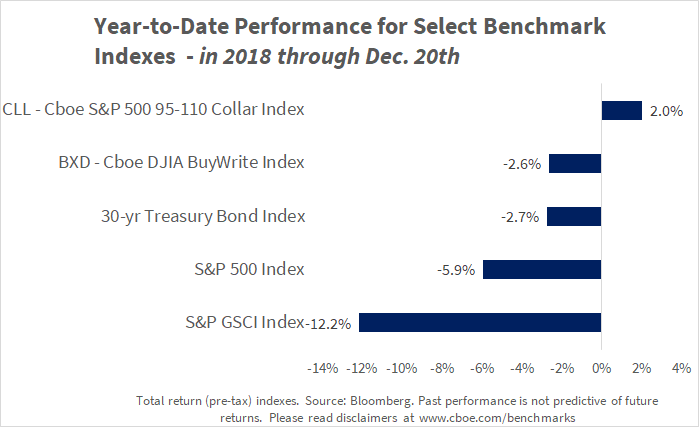

YEAR-TO-DATE PERFORMANCE AND MITIGATION OF LOSSES WITH CLL INDEX

The chart below shows that “traditional” key benchmark indexes for large-cap US stocks, small-cap US stocks, emerging markets stocks, Treasury bonds and commodities all fell in 2018 (through December 20), but that the Cboe CLL index rose 2% in the same time period.

The Cboe S&P 500 95-10 Collar Index (CLL) is an index designed to provide investors with insights as to how one might protect an investment in S&P 500 stocks against steep market declines. This strategy accepts a ceiling or cap on S&P 500 gains in return for a floor on S&P 500 losses. The passive collar strategy reflected by the index entails:

- Holding the stocks in the S&P 500;

- Buying three-month S&P 500 (SPX) put options to protect this S&P 500 portfolio from market decreases; and

- Selling one-month S&P 500 (SPX) call options to help finance the cost of the put options.

The term “95-110” is used to describe the CLL Index because (1) the three-month put options are purchased at a strike price that is about 95 percent of the value of the S&P 500 at the time of the purchase (in other words, the puts are about five percent out-of-the-money), and (2) the one-month call options are written at a strike price that is about 110 percent of the value of the S&P 500 at the time of the sale (in other words, the calls are about ten percent out-of-the-money). The starting and base date for CLL Index is June 30, 1986, at which it was priced at 100. The CLL Index is designed to be a valuable resource for investors who want to explore ways to manage their portfolio risk in bear markets.

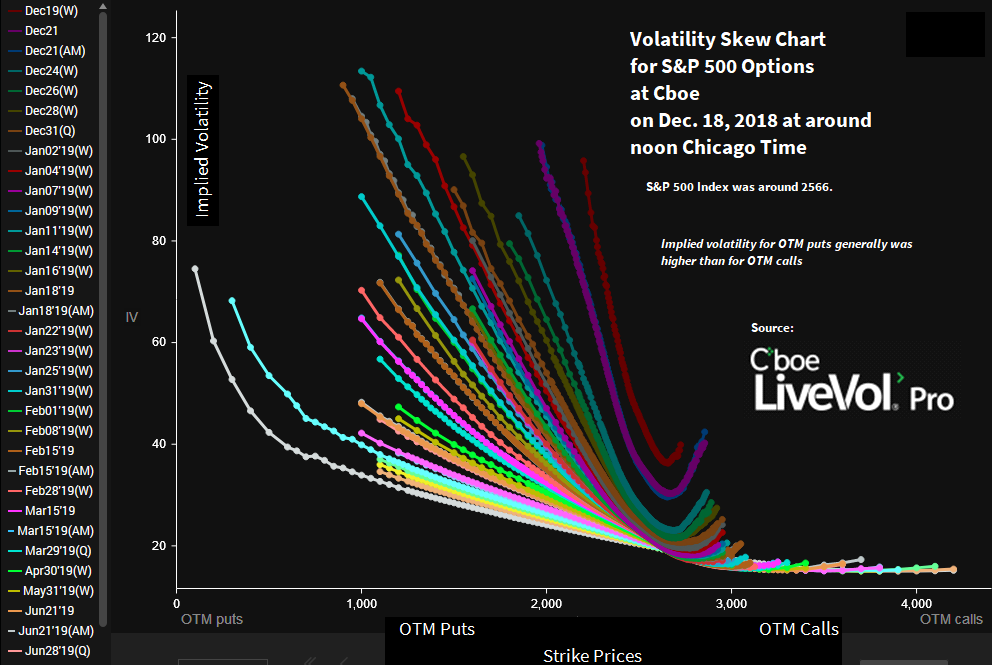

SPX SKEW CHART SHOWS HIGHER IMPLIED VOLATILITY FOR OTM PUTS

The volatility skew chart below shows estimates for implied volatility (y-axis) for S&P 500 options for the Monday, Wednesday and Friday expirations (dates in legend at left) and at various strike prices (in x-axis). Note that the implied volatility estimates for many of the out-of-the-money (OTM) S&P 500 put options range from 22 to 110, while the implied volatility estimates for many of the S&P 500 call options range from 15 to 40, a much lower range. One could infer from this chart that there probably is quite a bit of strong demand for downside protection with use of the OTM puts. In addition, in recent years many investors have seen the performance of the Cboe S&P 500 PutWrite Index (PUT) and become more comfortable with the idea of selling cash-secured puts on the S&P 500.

MORE INFORMATION

To learn more about ways in which index options and volatility products can be used in portfolio management, please visit these links –

- www.cboe.com/SPX S&P 500 index options

- www.cboe.com/benchmarks Cboe’s strategy benchmark indexes, and related research papers by Wilshire and other firms.

- www.cboe.com/funds Funds that use options

- www.cboe.com/strategies Options strategies

- www.cboe.com/education Options education

- www.cboeRMC.com Cboe Risk Management Conferences in Europe, Asia and the U.S.

++++++++++++++++++++++++++