A couple of months ago, we took a look at the Chilean sovereign bond market and indices. This time, we will analyze the case of Mexico, starting with the local bond market, followed by its structure, and ending with its index performance.

Mexican domestic sovereign debt is issued by the Ministry of Finance (Secretaría de Hacienda y Crédito Público—SHCP) through the Central Bank (Banco de México—Banxico). It is issued through weekly auctions based on the annual finance plan, and on a quarterly basis, the Auction Program of Sovereign Securities is published.

The auctioned securities are:

- CETES: Mexican Federal Treasury Certificates are the oldest tradable debt instruments issued by the federal government, issued for the first time in 1978. They are zero-coupon securities that are traded at a discount rate, with a face value of MXN 10 and maturity terms of 28, 91, 182, and 364 days.

- MBONOS: Mexican Federal Government Development Bonds with a fixed interest rate are securities issued for terms longer than one year. They pay a coupon every six months, have a nominal value of MXN 100, and have maturity terms of 3, 5, 10, 20, and 30 years.

- UDIBONOS: Federal Government Development Bonds, denominated in Investment Units (UDIs), which are inflation linked, were developed in 1996. They are investment instruments that protect the holder from unexpected changes in the inflation rate. UDIBONOS pays a coupon every six months based on a fixed rate plus a gain or loss that is indexed to the performance of the UDI. They have a face value of 100 UDI’s and maturity terms of 3, 10, and 30 years.

- BONDES D: Federal Government Development Bonds are instruments that pay floating coupons every 28 days based on the weighted average interbank funding rate, with a maturity term of five years.

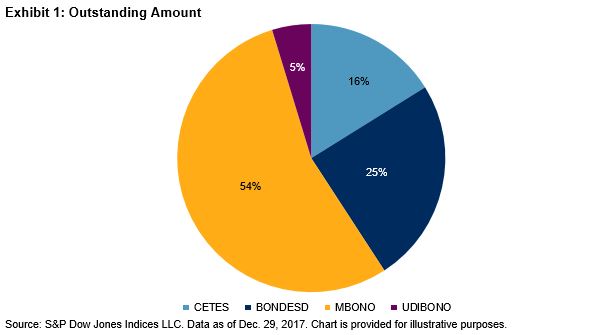

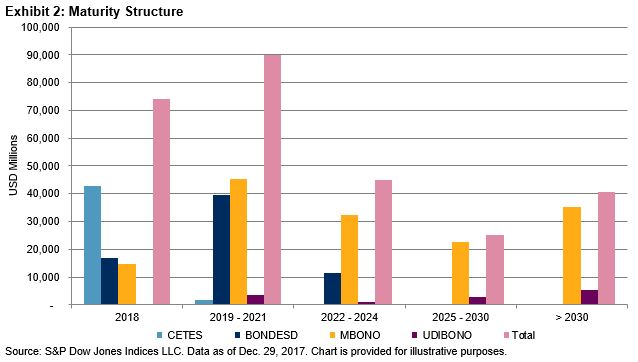

Using outstanding amount data, we can see the structure for these four types of bonds with a total of USD 270,000 million (see Exhibit 1). Exhibit 2 shows the maturity profile, including the total per bucket, and we can see that one-third of the total maturities occur between 2019 and 2021. In 2018, without taking into account CETES, USD 32,000 million in bonds are expected to mature between Bondes D and MBonos.

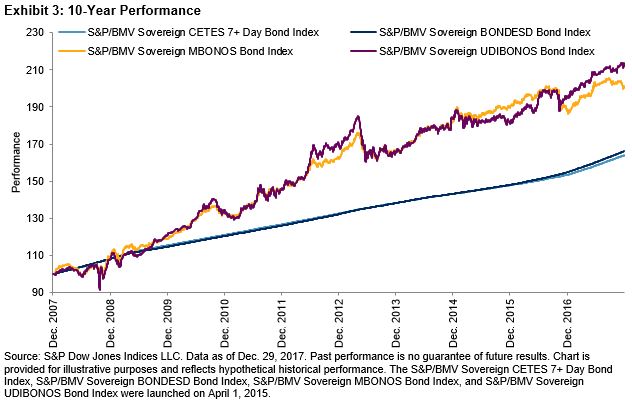

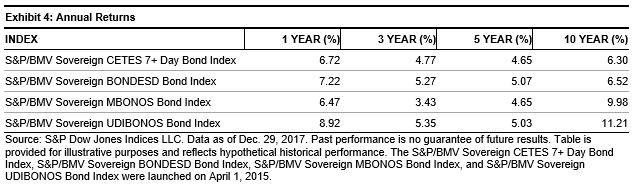

The S&P/BMV Fixed Income Indices have more than 25 different indices, which are mainly divided into maturity buckets, that track the performance of such bonds. Four of them cover the complete curves, tracking more than 170 bonds. Their performance and annual returns are shown in Exhibits 3 and 4.