In our previous blog, Earnings Revision Strategies in Asia, we discussed how those strategies performed in Asia. Although they worked well in various markets except Japan, there were some implementation challenges, such as high portfolio turnover and low liquidity for small-cap stocks. Therefore, implementing this strategy in combination with other fundamental factors with lower overall portfolio turnover may be more practical than implementing it as a single-factor strategy. Let us examine how an earnings revision strategy has worked historically in combination with a value strategy in the Asian market. The combination seeks to track the performance of undervalued stocks with high earnings expectations.

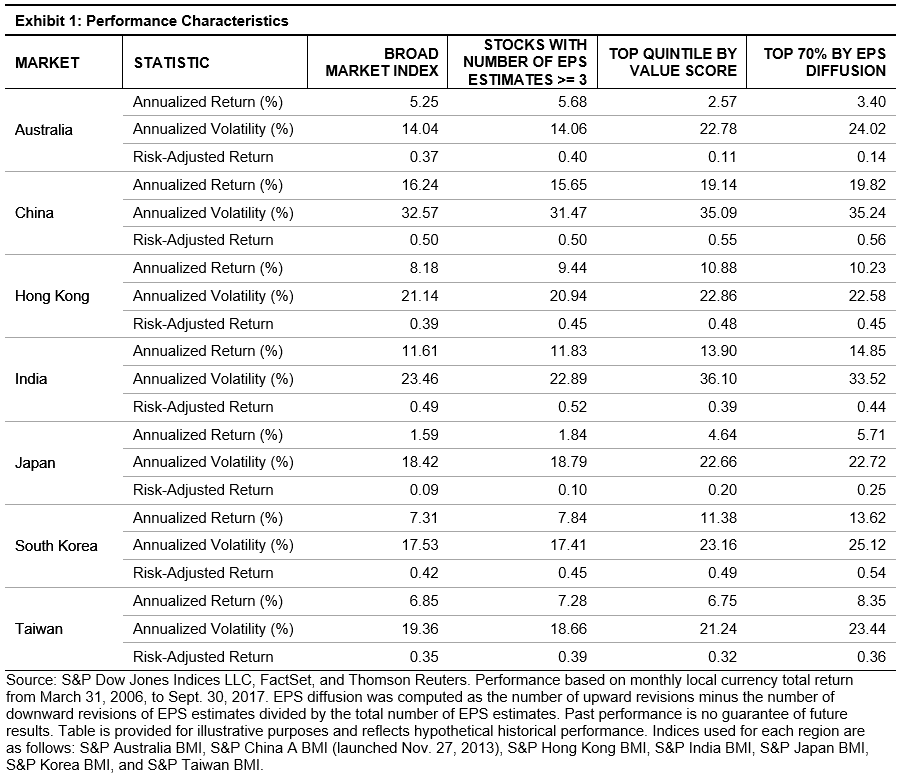

Adopting the S&P Enhanced Value Indices methodology,[1] we used earnings-to-price, sales-to-price, and book-value-to-price ratios to identify stocks that were relatively undervalued in comparison to the other stocks in the universe. Stocks with higher ratios were assigned higher value scores. We first selected a top quintile of stocks with the highest value scores from the universe.[2] From these stocks, we selected the top 70% of stocks with the highest earnings estimate diffusion, which is defined as the net percentage of upward and downward revisions in the earnings estimates.[3] We rebalanced the portfolios semiannually in March and September and weighted the portfolio members by their float-adjusted market cap.

With this sequential screening approach, the earnings diffusion strategy delivered return alpha over the simple value strategy in a majority of the Asian markets, with the most pronounced excess return in South Korea and Taiwan (see Exhibit 1). The annualized portfolio turnover was moderate, ranging from 80% to 100% over the back-tested period from March 31, 2006, to Sept. 30, 2017. Interestingly, despite the fact that the simple earnings revision strategy did not historically work in the broad Japanese market as noted in our research paper Do Earnings Revisions Matter in Asia, the earnings diffusion overlay delivered excess return on the value screened stocks in Japan. This implies that market participants in search of undervalued stocks in the Japanese market tended to care more about earnings revisions.

[1] For more details please see: http://spindices.com/documents/methodologies/methodology-sp-enhanced-value-indices.pdf.

[2] For each market, the universe comprised stocks with at least three analysts’ estimates. The indices used for each market were: S&P Australia BMI, S&P China A BMI, S&P Hong Kong BMI, S&P India BMI, S&P Japan BMI, S&P Korea BMI, and S&P Taiwan BMI.

[3] Earnings diffusion was calculated over the previous six-month period as of the data reference date. For more details please see: https://spindices.com/documents/research/research-do-earnings-revisions-matter-in-asia.pdf.

The posts on this blog are opinions, not advice. Please read our Disclaimers.